Although listed on AIM and headquartered in Jersey, Naibu Global International is a Chinese company and operate exclusively in that country. They design, manufacture and supply Naibu branded sport shoes and design and supply Naibu branded clothing and accessories. The target market is students and young people between 12 and 35. There are currently two factories with eight production lines and there are 3,040 stores across 21 Chinese provinces. The business is split into two segments: The design manufacture and sale of footwear comprises athletic and leisure footwear under the Naibu brand and the design and sale of apparel and accessories which are marketed under the Naibu brand but manufactured by an outsourced manufacturer. When I have converted from RMB to GBP it is very rough and only so I could more easily understand the size of the company.

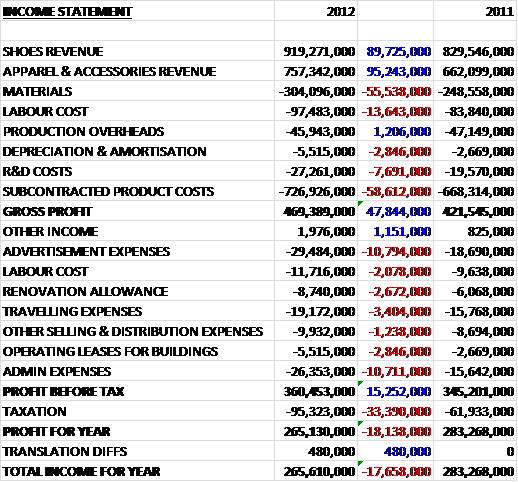

When compared to last year revenues are up strongly for both shoes and apparel as the group increased the number of branded stores by 170 to 3,040 and the group managed to increase unit sales price but materials and labour costs also increased along with R&D costs and subcontractor production costs (only the shoes are made by Naibu themselves). This meant that Gross profit was up by RM47.8M to RM469.4M. Admin costs are also up a fair amount to give a profit before tax RM15.3M higher at RM360.5M. The big difference to last year is a RM33.4M hike in tax costs relating to the tax that the Chinese government levies on dividends and as a consequence of this profit for the year was down RM18.1M to RM265.1M, which in terms that I can understand translates roughly to a £1.8M fall to £26.5M.

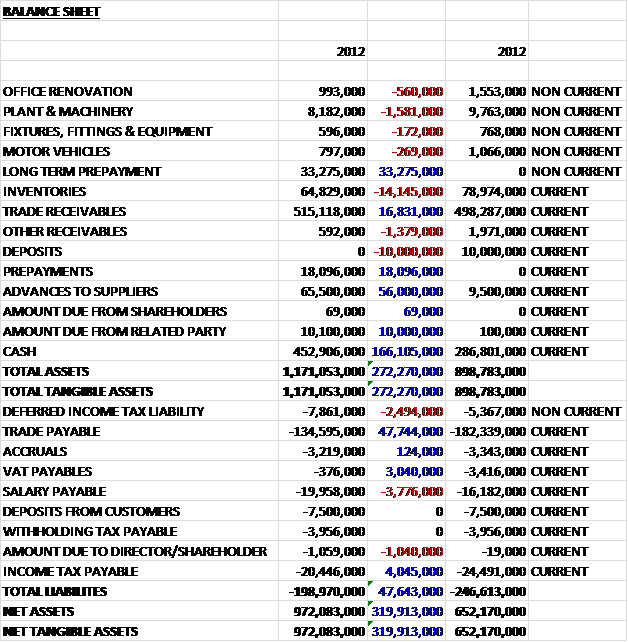

Overall, assets increased by about £27.3M during the year, driven by a £5.6M advance to suppliers which is apparently the deposit paid to suppliers to establish a “cooperation relationship” – interesting; a £5.1M increase in prepayments (relating to prepayments of store renovation for distributors) and a hefty £16.6M hike in cash levels which was slightly mitigated by a £1.4M fall in inventories. Deposits relate to deposits paid for the acquisition of a factory and staff hostel from related parties. This amount was transferred to amount due from related parties this year. Surprisingly, liabilities fell during the period by £4.8M driven almost entirely by a £4.8M fall in trade payables. There were no intangible assets so overall net tangible assets increased by an impressive £32M to £97.2M.

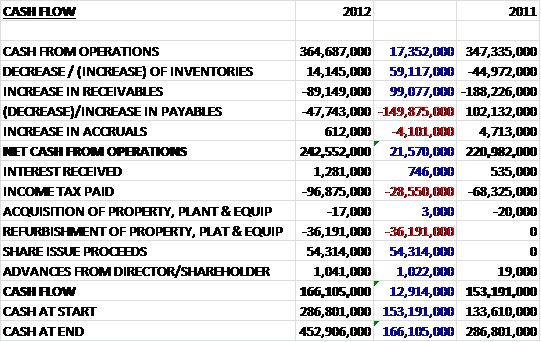

At £36.5M, cash profits were up on last year. An increase in receivables (average debtor days increased from 103 to 121 days which seems like a lot but I guess could be the norm for China) and a decrease in payables, slightly mitigated by a strong control on inventories, took the net cash from operations down to £24.3M but this was still £2.2M up on last year. The largest expenditure was tax which increased by £2.9M to £9.7M and the refurbishment of property which was £3.6M that did not occur last year. The group gained a cash inflow of £5.4M from share issues which gave a cash flow of £16.6M for the year, £1.3M up on last year. This is a strong cash generation and would still have been fairly substantial without the new share issue, although it would have been lower than last year.

When looking at this company as investment, one of the most relevant factors is that it operates in China which is still under communist control. There is a warning in the annual report that although the political landscape is currently stable, in the future there may be changes introduced affecting the way companies do business and in particular their ownership structure – something to bear in mind. Another peculiarity of doing business in China is that regulations require to transfer 10% of its profit after tax to the statutory reserve until the reserve balance reaches 50% of the respective registered capital. This reserve is therefore not available to be distributed to shareholders.

Although profits before tax were up, margins were eroded somewhat this year due to increased R&D and advertising together with the costs related to the IPO. The group is also investing in production capacity. Currently they have 8 ageing production lines in two factories in Fujian province. The lease on one of the plants is due to expire at the end of the year and the group are negotiating in order to acquire a plant in Quangang where 8 new production lines will be created. There is not expected to be any effect on production while the change-over takes place but the timings seem quite tight. They are also in negotiations to purchase a factory in Sichuan province to provide 12 more production lines. This is taking longer than expected due to the political changes in the country but should be completed by the end of 2014 and will give the group a much larger capacity and a foothold in Central and Western China.

Although shoes account for a larger portion of revenues, the profits are similar for both segments and are indeed growing at a quicker rate for apparel and accessories. The group have two customers that contributed over 10% of group revenues which represents a bit of a risk but it does seem as though the group could cope with the loss of one of these clients. One thing to note is that nearly half (46.75%) of the shares are owned by the founder Huoyan Lin with the only other director to own any shares being Giles Elliott who has picked up a measly 8,065. During the year Kenny Law resigned as the CFO to return to Singapore. Ms. Zhen Li was announced as his successor.

So, profit for the year was up about £1.5M before tax but due to the tax paid on dividend payments the net profit for the year was down by £1.8M. Net assets showed a very healthy increase, mainly due to a big hike in cash levels and a reduction in trade payables. Not including the cash flow from new shares, the cash inflow for the year fell by £4.1M due to increased tax and refurbishments to their property but it was still fairly healthy at £11.2M. At the year end, the group announced its maiden dividend of 4p per share. At the current share price, this represents a tasty yield of 5.3% and marks the start of further dividend announcements in future, along with the proposed introduction of an interim dividend. At current share price the P/E ratio is a measly 1.5 reducing to 1.4 next year. There is also not debt at the company and I think that they are worth a buy despite the potential pitfalls of investing in China. Before I make my decision, however, I will take a look at another similar company, Camkids.