Central Asia Metals has now released their final results for the year ended 2017.

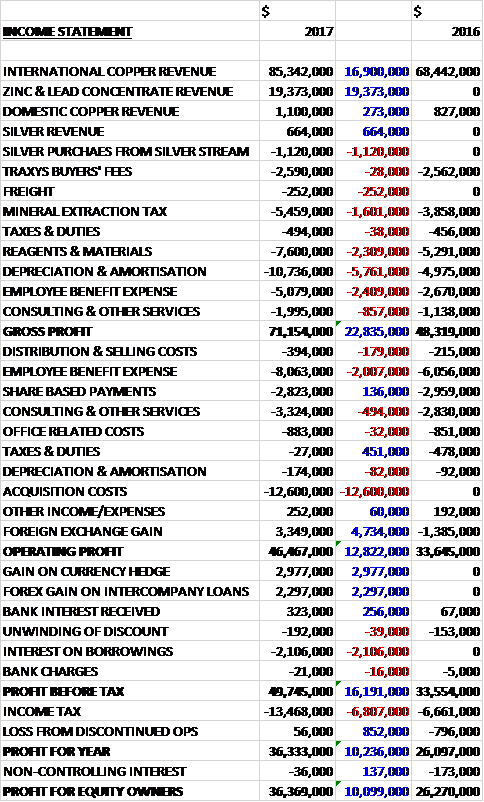

Revenues increased when compared to last year with a $16.9M growth in international copper revenue and a $273K increase in domestic copper revenue. There was also the first signs of zinc/lead revenue along with silver revenue which brought in $19.4M and $664K respectively. Mineral extraction tax was up $1.6M, reagents and materials increased by $2.3M, depreciation and amortisation grew by $5.7M, the employee benefit expense was up $2.4M and other cost of sales increased by $857K to give a gross profit £22.8M higher. We then see a further $22M increase in employee benefit expenses and $12.6M of acquisition costs, partially offset by a $4.7M positive movement in forex hedges to give an operating profit $12.8M ahead. There was a further $3M gain on the currency hedge, and a $2.3M forex gain on intercompany loans but interest costs on borrowings increased by $2.1M and tax charges were up $6.8M to give a profit for the year of $36.4M, a growth of $10.1M year on year.

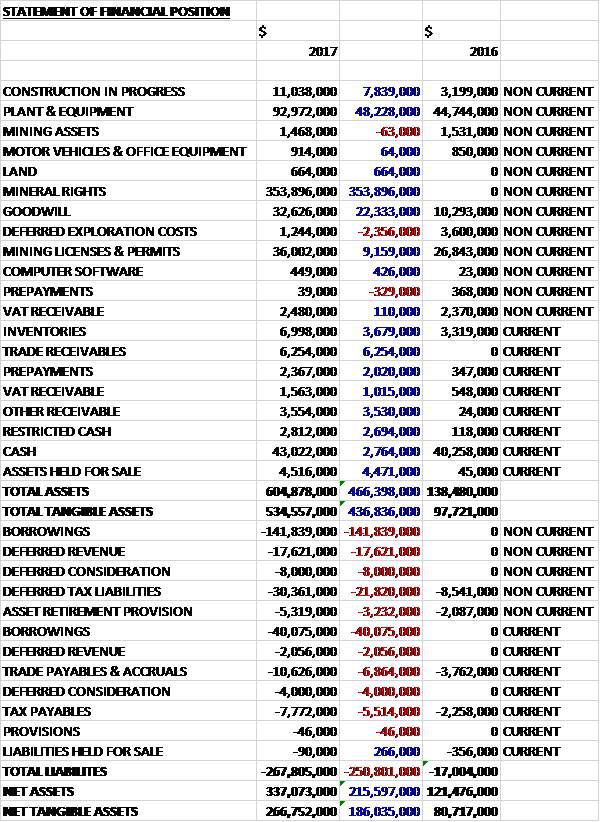

When compared to the end point of last year, total assets increased by $466.4M driven by a $354M growth in the value of mineral rights, a $22.3M increase in goodwill, a $48.2M increase in plant and equipment, and a $9.2M increase in the value of mining licenses and permits. Total liabilities also increased during the year sue to a $181.9M increase in borrowings, a $21.8M growth in deferred tax liabilities, a $17.6M increase in deferred revenue and a $12M growth in deferred consideration. The end result was a net tangible asset level of $266.8M, a growth of $186M year on year.

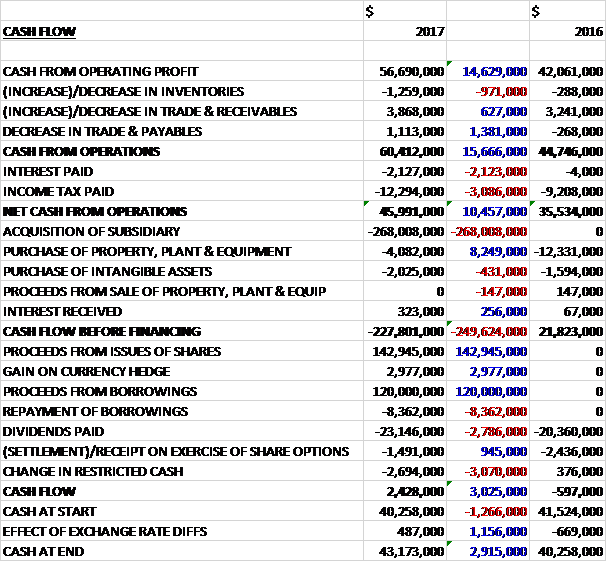

Before movements in working capital, cash profits increased by $14.6M to $56.7M. There was a cash inflow from working capital but interest payments increased by $2.1M and tax payments were up $3.1M to give a net cash from operations of $46M, a growth of $10.5M year on year. The group spent $4.1M on tangible assets and $2M on intangibles but the big spend was the $268M spent on the acquisition which meant that before financing there was a cash outflow of $227.8M. The group also paid out $23.1M in dividends but brought in $142.9M from the share issue and $120M from new loans. The end result was a cash flow of $2.4M and a cash level of $43.2M at the year-end.

These results reflect a much improved copper market, with the LME price increasing by 30% throughout the year with copper prices increasing from $4,994 per tonne last year to $6,107 per tonne. The sector is also now starting to experience cost inflation

The adjusted EBITDA for Kounrad was $63.6M, a growth of $12.2M year on year. During the year the group sold 14,001 tonnes of copper through off take agreements and 180 tonnes to local customers compared to 13,751 tonnes and 187 tonnes last year respectively.

The group produced 14,103 tonnes of copper during the year. In April they began leaching copper form the Western Dumps after their stage 2 expansion that was delivered 30% below budget as a result of the weaker local currency and engineering efficiencies. During the year 40% of the copper production was from the Western Dumps with the contribution increasing as the year progressed. Production from the Western Dumps has been in line with expectations with some 65% coming from there in Q4.

The cash cost of production increased modestly from 43c per pound to 52c per pound reflecting the increased electricity consumption and additional labour costs of working on the Western Dumps, but they remain one of the lowest cost copper producers in the world.

The maiden adjusted EBITDA for Sasa for the first two months of ownership was $14.5M. During the year the group sold its zinc and lead concentrate to two European smelters. They sold 2,906 tonnes of zinc concentrate and 4,559 tonnes of lead concentrate. In January 2018 the group entered into a zinc and lead concentrate off take agreement with Traxys which has been fixed through to the end of 2022. This is for all of the Sasa concentrate production.

In September 2016, Lynx Group entered into a Silver Purchase agreement with Lynx Metals by netting of its existing loan payable with Lynx Metals. The prepayments for the purchase of silver are recognised as deferred revenue and are related to production of silver during the life of the mine. Deferred revenue is recognised on the income statement as the silver is delivered

The EBITDA loss from Shuak was $130K. During the year the team undertook over 22,000 metres of drilling in the license area. The findings have been encouraging with additional oxide potential identified at the Kyzyl-Sor prospect and some interesting deeper intersections of Sulphide mineralisation. They will soon embark on another exploration season in 2018 which should enable them to better understand the potential in terms of continuity and likely scale.

After announcing the positive results from the Copper Bay definitive feasibility study in January the group undertook some additional engineering studies with the intention of improving the economics of the project. Some capex savings were identified and there is the potential to optimise the project further in the future. In the context of the new Sasa mine, however, the board decided that it was no longer a material asset so they have started a sales process.

In November the group acquired Lynx Resources which owns the SASA mine located in Macedonia. The mine comprises an operating underground zinc and lead mine and a processing facility that produces both zinc and lead concentrate. The group paid a total of $401.1M with $340M in cash, $49M in new shares and $12M in deferred consideration and the acquisition generated goodwill of $22M.

In June, director Kenges Rakishev sold his 86% interest in KKB bank, which the group uses for its normal day to day banking. In September he sold half of his shareholding in Central Asia Metals and in February 2018 he sold his remaining shareholding. I hope that this is not something to be worried about as having such an influential local businessman as a key shareholder was a big plus for the group in my opinion.

As of the year-end a total of $2.7M of VAT receivable was still owed to the group by the Kazakhstan authorities. A portion of this amount totalling $233K was refunded in January.

Going forward, many industry commentators are expecting a challenging year for copper supply that could result in another positive year for the copper price. In the zinc market, supply side challenges remain whilst demand is expected to increase to over 15 million tonnes by 2019. The board expect steady production from both Sasa and Kounrad. They have set their 2018 cooper production target at between 13,000 and 14,000 tonnes. They expect to produce between 21,000 and 23,000 tonnes of zinc and between 28,000 and 30,000 tonnes of lead.

At Kounrad, the proportion of copper production from the Western Dumps will increase to around 65% in 2018, and by 2020 almost all of the production will be from those areas which will mean an increase in electricity consumption. At Sasa the operational focus will be on completing construction of the new tailings storage facilities that will ensure sufficient storage for operations until at least 2026. Both mines are expected to be highly cash generative and should enable the group to return to shareholders a target range of between 30% and 50% of free cash flow.

At the current share price the shares are trading on a PE ratio of 13.6 which falls to 7.8 on next year’s consensus forecast. After the final dividend was kept the same, the shares are yielding 5.8% which falls to 5.6% on next year’s forecast. At the year-end the group had a net debt position of $138.9M compared to a net cash position of $40.3M at the end of the prior year.

On the 12th April the group released a Q1 operations update with both operations on track to achieve 2018 production targets. At Kounrad the group produced 3,070 tonnes of copper, a reduction of 287 tonnes year on year. The winter period was the coldest experienced in five years and 75% of production came from the Western Dumps. Copper sales during the period were 2,527 tonnes.

At Sasa the group produced 5,518 tonnes of zinc, an increase of 229 tonnes; and 7,020 tonnes of lead, a decline of 266 tonnes. During the period, mined and processed ore was 192,372 tonnes and 196,364 tonnes respectively. The average head grades for the period were 3.32% zinc and 3.83% lead.

Following completion of the Shuak 2017 exploration programme, the group has now received all assay results for the drilling undertaken. The new areas of oxide mineralisation that have been identified at the Kyzyl-Sor prospect have an estimated average thickness of 46 metres at an estimated average copper grade of 0.32% based on CHT drilling.

Overall then this has been another year of progress for the group with profits, net assets and operating cash flow all increasing. This mainly seems to be down to the 30% increase in copper price with production increasing only slightly and cash costs increasing due to higher electricity consumption at the Western Dumps.

The group has used this increase in commodity prices to acquire the Sasa mine which adds two more metals to their repertoire. Q1 has started OK but there was lower copper production due to the cold winter. Overall though, despite their being rather more risk here now due to the borrowings that have been taken out, I feel the forward PE of 7.8 and yield of 5.6% represents decent value and I remain a holder.

On the 10th July the group released a trading update covering the first half of the year. Q2 copper output of 3,677 tonnes brings output for the first half of the year to 6,747 tonnes, a decline of 280 tonnes year on year, attributed to a particularly cold Q1.

At Sasa, 11,020 tonnes of zinc was produced, an increase of 281 tonnes mainly due to increased grades. The mine produced 14,386 tonnes of lead, a decline of 493 tonnes due to lower grades and slightly lower recovery. Q2 zinc recoveries were lower than previous periods due to a mechanical failure of the original zinc regrind mill and commissioning of the new SMD mill. During the period they sold 180,233 ounces of silver which had been pre-sold.

Exploration started at Shauk in May and since then, 11,550 metres of core drilling has been undertaken. A survey will be undertaken in the second half as well as a diamond drilling programme to start in Q3. As of the end of the half, the group had $40.5M of cash in the bank.