Character has now released their interim results for the year ending 2018.

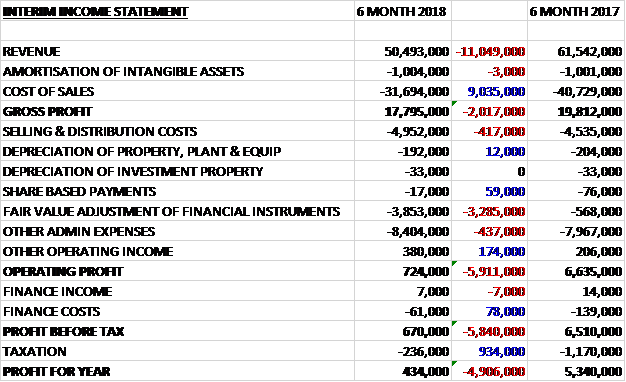

Revenues declined by £11M when compared to last year and with cost of sales down just £9M, the gross profit declined by £2M. There was a £417K growth in selling and distribution costs, a £3.3M increase in the losses from financial instruments and a £437K growth in other admin expenses which meant that the operating profit fell by £5.9M. There was a modest decrease in finance costs and a £934K decline in tax charges to give a profit for the period of £434K, a decline of £4.9M year on year.

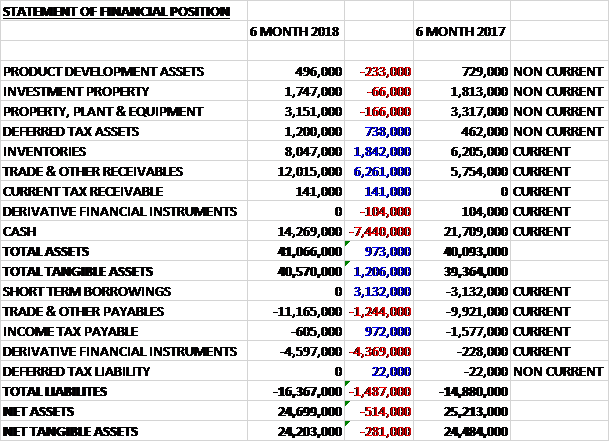

When compared to the end point of last year, total assets increased by £973K, driven by a £6.3M growth in receivables, a £1.8M increase in inventories and a £738K increase in deferred tax assets, partially offset by a £7.4M decrease in cash. Total liabilities also increased during the period as a £3.1M fall in short term borrowings and a £972K decline in income tax payable was more than offset by a £4.4M increase in derivative financial liabilities and a £1.2M increase in payables. The end result was a net tangible asset level of £24.2M, a decline of £281K over the past six months.

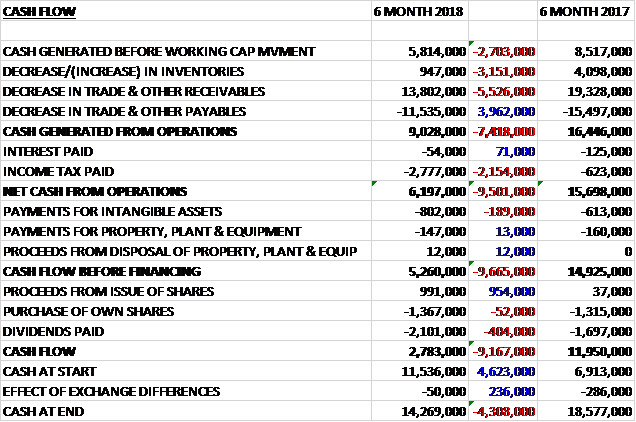

Before movements in working capital, cash profits declined by £2.7M to £5.8M. There was a cash inflow from working capital but this was less than last time and after tax payments increased by £2.2M, the net cash from operations was £6.2M, a decline of £9.5M year on year. The group then spent a net £376K purchasing shares and paid out £2.1M in dividends to give a cash flow for the half year of £2.8M and a cash level of £14.3M at the period-end.

In the first four months sales were in line with expectations, with UK sales being up and FOB sales being lower than last year. This period included the Christmas sales where the group focused on domestic sales efforts on absorbing the impact of the failure of Toys R Us in the UK. The environment for FOB sales was more challenging, and the group has been negatively impacted by several global factors, most notably the adverse forex movements and the global restructuring of Toys R Us which had a direct adverse impact on all major international markets. In January and February UK sales achieved record levels, ahead of budget.

At this year’s London Toy Fair they won two awards: The best electronic toy for the Laser X Dual Pack and the best action toy for the Original Stretch Armstrong. The leading in-house ranges of Peppa Pig, Stretch, Teletubbies and Scooby Doo, and the third party lines including Little Live Pets and Mashems, continued to trade well. They will be added to by the new line up of Pokemon toys which will be launched in the summer. Impulse buying is a growing trend and the group are looking to tap into this with their new “craze” lines such as Soft and Slo, make your own slime, cup cake cuties and Mine iT.

A significant proportion of the group’s purchases are made in US dollars. The business is therefore exposed to forex fluctuations and manages the risk through forward exchange contracts. At the end of each reporting period they make an adjustment in their statements to reflect the current valuation of these instruments. During the period this led to a charge of £3.9M. There is some volatility in this due to the timing of the exchange rates at the period-end but I would have thought in general, they would have benefited in some way given this is a hedge.

Going forward, the calendar year has started encouragingly with the established brands and new ranges selling through well at retail. The board remain of the view that the group will continue to make good progress in meeting the demands of its customers and growing the business. They are looking for a record second half year for their domestic business and a recovery in their FOB business next year.

The directors remain optimistic that the business will see a return to its previous growth pattern during the second half of the year and this will be fully reflected and significantly strengthen the trading results in 2019.

At the current share price the shares are trading on a PE ratio of 11 which increases to 12.9 on the full year consensus forecast. After a 22% increase in the interim dividend the shares are yielding 4.2% but this remains flat on the full year forecast. At the period-end the group had a net cash position of £14.3M compared to £11.5M at the year-end.

Overall then this has been a rather difficult period for the group. Profits declined, even when the forex losses were excluded, net assets fall and the operating cash flow was down, albeit still with some free cash being generated. The problems seem to be due to the collapse of Toys R US and the issues seem to have worked their way through as the last two months of the period saw a pick up in performance and the second half has started fairly well. A forward PE of 12.9 and yield of 4.2% looks OK and I am tempted to jump back in here now the issues seem to have been resolved.