Air Partner has now released their final results for the year ended 2018.

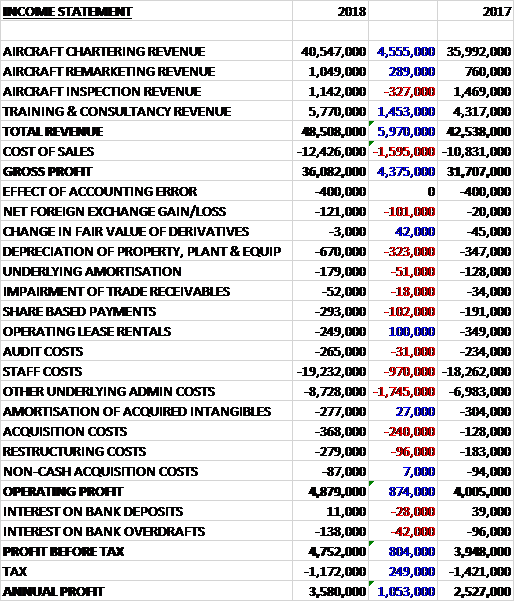

Revenues increased when compared to last year as a £327K decline in aircraft inspection revenue was more than offset by a £4.6M growth in aircraft chartering revenue, a £1.5M increase in consultancy revenue and a £289K growth in aircraft remarketing revenue. Cost of sales also increased to give a gross profit £4.4M higher. Depreciation was up £323K, staff costs increased by £970K and other underling admin costs grew by £1.7M. We also see a £240K increase in acquisition costs to give an operating profit £874K higher. There was a modest increase in finance costs but this was offset by a £249K reduction in tax charges which meant that the profit for the year was £3.6M, a growth of £1.1M year on year.

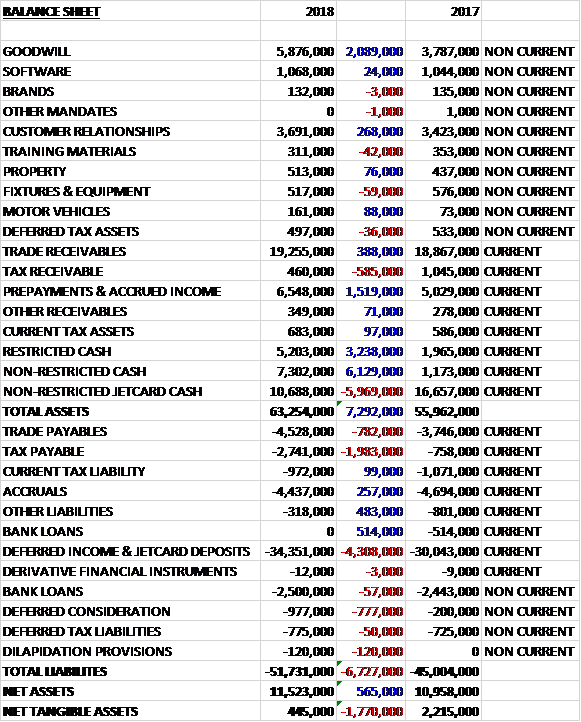

When compared to the end point of last year, total assets increased by £7.3M driven by a £6.1M growth in non-restricted cash, a £3.2M increase in restricted cash, a £2.1M growth in goodwill and a £1.5M increase in prepayments and accrued income, partially offset by a £6M decline in jetcard cash. Total liabilities also increased during the year due to a £4.3M growth in deferred income and Jetcard deposits and a £2M increase in current tax payables. The end result was a net tangible asset level of just £445K, a decline of £1.8M year on year.

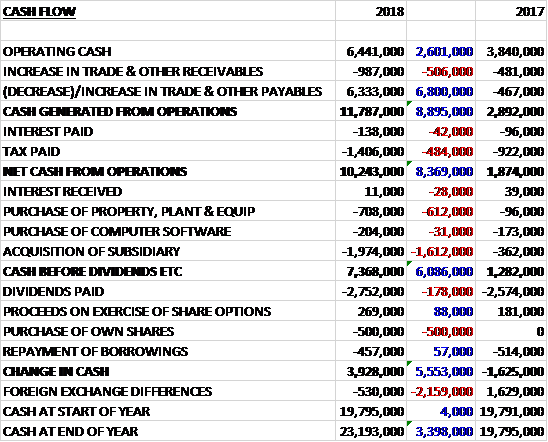

Before movements in working capital, cash profits increased by £2.6M to £6.4M. There was a big cash inflow from working capital and despite tax payments increasing by £484K, the net cash from operations was £10.2M, a growth of £8.4M year on year. The group spent £708K on fixed assets, a £204K on computer software and £2m on acquisitions to give a free cash flow of £7.4M. Of this, £2.8M was paid out in dividends, £457K on loan repayments and £500K on share purchases to give a cash flow of £3.9M and a cash level of £23.2M at the year-end.

The underlying operating profit in the Commercial Jets division was £3.8M, a growth of £461K year on year. Strength has been seen across territories and sectors and from new and existing customers. In the US they posted record results despite a strong comparative last year. The traditionally softer second half of the year did not materialise as they were able to respond to customers needs in the face of the hurricanes which hit the US, and to a non-hurricane related evacuation for a customer in the leisure sector. There has also been an increase in the corporate sector.

In Europe they have benefited from prior investment in people in the sports sector and they are well placed to perform well with the world cup taking place in Russia. They saw good results from their tour operator programmes and continued strength in automotive, where they have helped with the launch of a cross over vehicle for a major German manufacturer and are seeing growing opportunities despite an increasingly competitive environment. In the UK and Europe they continue to see steady, year round demand to meet government requirements.

Air Partner Remarketing has had an encouraging year in which it has secured a number of exclusive mandates and demonstrated the benefit of inclusion in the wider group with the recent sale of a 2009 vintage Beechcraft King Air 200 for Air Hamburg, the result of an introduction from the Private Jets business. During the year they also sold two B737 aircraft and a GE engine for Kenya airways, two 747s on behalf of China Airlines, and won exclusive contracts with a large Australian bank and with Saudia, the latter to market 15 Boeing 777 aircraft.

The underlying operating profit in the Private Jets division was £1.1M, a decline of £1.4M when compared to last year. This largely reflects lower sales in the UK, as the group moved key personnel to the US, and the subsequent impact of investment they have made in upskilling the sales team. They are beginning to see the benefit in the New Year. In the US, where they expanded their office in NY last year, the investment has enabled them to service an increase in demand and they have seen a record rise in overall client numbers of 80%. Business from existing customers is performing well with Jetcard renewals up 16% including two €1M renewals and utilisation up 8%.

The underlying operating profit in the Freight business was £1.8M, an increase of £1.5M when compared to 2017. This performance has been driven by a mix of charters carried out across the Caribbean to support the aid efforts of hurricanes Irma and Maria, the impact of new hires over the period, and ongoing contracts in the Middle East.

The underlying operating profit in the Consultancy and Training business was £561K, a decrease of £90K year on year. Baines Simmons had an encouraging year with good long term contract wins and some of the pipeline projects crystallising in the second half. Contract wins have been good across civil and military organisations and the forward pipeline remains strong. In the first half the business secured contracts with national carriers, the RAF of Oman and the European Defence Agency. In January they won the Safety Training for Error Prevention tender with the MOD for a four to six year contract. A number of commercial contracts were also won throughout the year.

The fatigue risk management team has had a good second half. Over the year they have carried out work for national carriers and airlines across the world along with a train provider in the UK. In a move into rotary, a national air rescue client became the first rotary operator in Europe to be given a fatigue risk management approval by the regulator. The pipeline of opportunities for the business is good and they expect to increase efficiency further next year.

SafeSkys, acquired in September, has performed well over Q4. The integration of the team was completed in November. The business has a good customer base with stable contracts of an average of four to six years. A key RAF contract was secured at the year-end to operate in the Scottish region. The air traffic control side of the business is performing in line with expectations.

In September the group acquired Safe Skys ltd, a supplier of turnkey ATC services and wildlife management services. The total consideration was £3M, of which £2.2M was paid in cash with the remainder deferred consideration. The business contributed £70K of profit in the first five months of ownership and the acquisition generated £2M of goodwill.

The business provides airport wildlife management and services, air traffic control and air traffic engineering to over 85 international airports. The business is also an Air Navigation Service Provider. One of the group’s ATS contracts is with Llanbedr, which was resurrected in 2014 as a centre of excellence for unmanned aerial systems. The acquired business was engaged early in the project to re-establish the provision of air traffic services which involved designing and re-equipping the control tower with state of the art equipment, the production of procedures and operations manuals as well as the design and implementation of the safety management system.

In April, following the recruitment of new and enhanced skills into the finance department, the group identified an issue, predominantly relating to the accounting for receivables and deferred income, originating in 2011. They then appointed independent advisors to carry out a review which is now concluded. No cash or assets were lost and no customer was impacted. Integrating the review into the full year audit took significant time and forced the suspension of trading in the shares. CFO Neil Morris resigned and an interim CFO has been appointed. The group will incur costs of £1.3M in 2019 as a result of the review and an aborted acquisition.

In late 2017 the group entered discussions to acquire a managed services business. At the beginning of January, having agreed transaction terms they entered into an exclusivity period expiring at the end of April. The acquisition wold have met the group’s financial return criteria and immediately increased the weighting of their consultancy profitability by 30%. When the above accounting issues were identified, they let the exclusivity lapse but they remain in dialogue with the board members of the business.

Going forward, at the start of the year the board are seeing a particularly strong performance in Freight and the US. Commercial jets is flat while private jets UK has started the year slowly. At the beginning of the year, for global charter at least, it is too early to predict the full year outcome. The more pipeline oriented businesses have encouraging order books which will develop even further during the year ahead.

After a 5.8% increase in the full year dividend, the group is yielding 4.7% which increases to 4.8% on next year’s consensus forecast. At the current share price the shares are trading on a PE ratio of 17.8 which falls to 16 on next year’s forecast.

Overall then this has been a rather mixed year for the group. Operationally it has been rather decent with increased profits and an improvement in the operating cash flow with a good amount of free cash being generated, although the latter was mostly due to working capital movements. Commercial Jets had a good year with a boost from the hurricanes and the world cup along with growth in the corporate and automotive markets. Freight has also fared well with a boost from the hurricanes. Private Jets has struggled somewhat, however, seemingly as resource was moved from the UK. Consulting also saw a reduced profit but no reason is given for this.

Obviously overshadowing this is the accounting debacle which means they have been over stating profits and assets. This does seem to be resolving, however, but it is still an unprofessional embarrassment. Going forward, the year has started OK but private jets still seem to be struggling in the UK. With a forward PE of 16 the shares are not exactly cheap but the yield of 4.8% is very decent. Tricky one this, on balance I might wait and see how the year pans out.

On the 24th August the group released a trading update covering the first half of the year when underlying pre-tax profit was in line with board expectations and with the same period last year. The US business had a record year last year and that strong performance continued across all business lines in the region with a new office being opened in Los Angeles.

In the UK, after a flat start, commercial jets performed well over Q2 with increased activity around the World Cup in Russia and a good result from tour operations. They continue to see the benefit of investments made in their freight business with another strong performance throughout the period. In the US and Europe, private jets has seen good growth in both jet card numbers and bookings throughout the first half. Whilst the UK has been more subdued, they have seen an increase in the number of jet cards in issue.

The consulting and training division is trading in line with expectations, winning some excellent long term contracts in the period. They have an encouraging pipeline for the remainder of the year and the division remains well placed for further growth.

Overall the board are encouraged by the start to the year and remain confident in the group’s prospects for the full year.