Bioquell has now released their interim results for the year ending 2018.

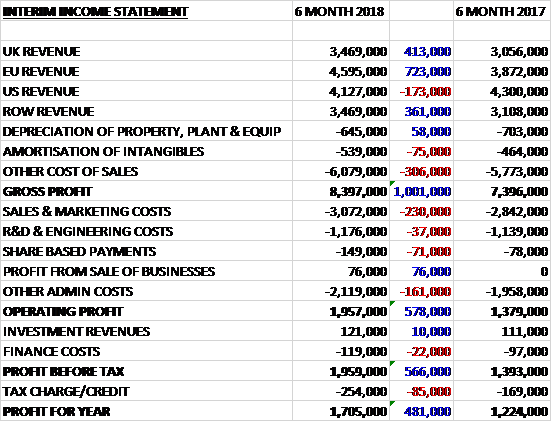

Revenue has increased when compared to the first half of last year as a £173K reduction in US revenue was more than offset by a £723K growth in EU revenue, a £413K increase in UK revenue and a £361K growth in ROW revenue. Cost of sales increased to give a gross profit £1M higher. Sales and marketing costs were up £230K and share based payments were up £71K, offset by a £76K profit from the sale of a business. Other admin costs increased by £161K to give an operating profit £578K higher. Finance costs were up modestly and tax charges grew by £85K to give a profit for the period of £1.7M, a growth of £481K year on year.

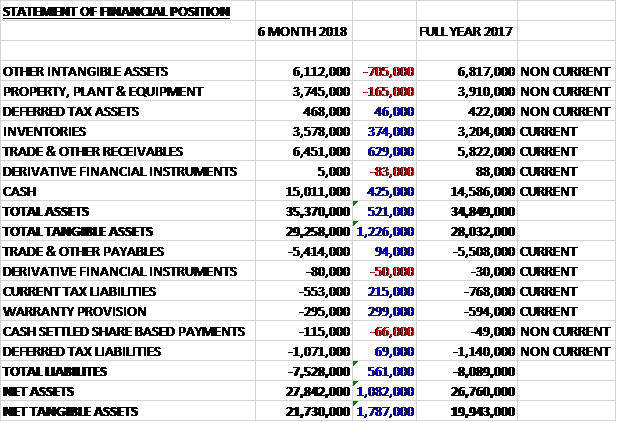

When compared to the end point of last year, total assets increased by £521K driven by a £629K growth in receivables, a £425K increase in cash and a £374K growth of inventories, partially offset by a £705K fall in other intangible assets and a £165K decrease in property, plant and equipment. Total liabilities declined during the period due to a £299K decrease in the warranty provision and a £215K fall in current tax liabilities. The end result was a net tangible asset level of £21.7M, a growth of £1.8M over the past six months.

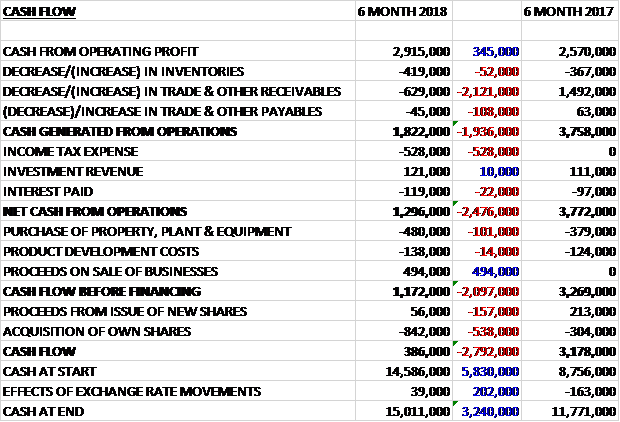

Before movements in working capital, cash profits increased by £345K to £2.9M. There was a cash outflow from working capital with a large increase in receivables and after tax payments increased by £528K the net cash from operations was £1.3M, a decline of £2.5M year on year. The group spent £480K on fixed assets and £138K on development costs but the recouped £494K from the sale of a business to give a free cash flow of £1.2M. Of this, £842K was used to buy their own shares for cancellation to give a cash flow of £386K and a cash level of £15M at the period-end.

The profit in the Bio division was £2.4M, a growth of £422K year on year with a 15% like for like increase in revenue. This growth was driven by a strong performance in sales of the Qube modular isolator, which were up 90%. This was partially offset by a small decline in revenues from bio decontamination solutions due to lower equipment sales than last year which included a large one-off order worth £1.1M.

The profit in the defence division was £92K, an improvement of £113K when compared to the first half of last year. The group anticipate a further £700K of revenue in the second half as a result of pre-existing commitments to complete current contracts which were not transferred as part of the sale.

During the period the group completed the disposal of its Air Flow business and sold its subsidiary MDH Defence for a total consideration of £494K which led to a profit on the sale of £76K. There is a contingent consideration of £600K. Following these disposals, the group is now focussed on two product lines – bio decontamination solutions and modular isolators which it sells to the pharmaceutical, life science and healthcare markets.

Going forward, given the continued improvements, particularly with respect to profitability the board believes that the group will exceed current market expectations for profit for the full year with a broadly similar financial performance in the second half as the first half.

At the period-end the group had a net cash position of £15M compared to £11.8M at the same point of last year. There are no dividends on offer here.

Overall then this has been a good half year for the group. Profits are up, net assets increased and although the operating cash flow declined, this was due to working capital movements and the group still made a decent amount of free cash. The good performance seems to be entirely due to increased sales of the Qube unit. It is unclear as to whether this is a ramp up in demand or just the lumpy orders working their way through the system. On balance, if the price looks decent I’d be tempted to buy in here. Unfortunately the shares look too expensive to me.