Amino Technologies has now released their interim results for the year ended 2018.

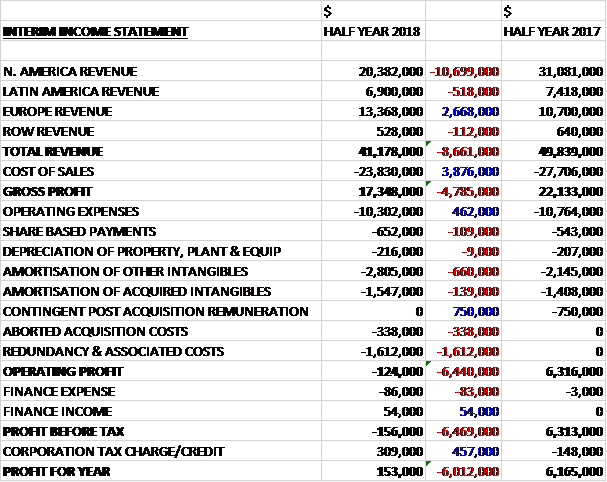

Revenues have declined when compared to the first half of last year as a $2.7M increase in European revenues have been more than offset by a $10.7M decline in North American revenue, a $518K decrease in Latin American revenue and a $112K fall in ROW revenues. Cost of sales also declined to give a gross profit $4.8M lower. Operating expenses declined by $462K and there was no contingent post acquisition remuneration which cost $750K last time, but amortisation increased by $800K, there was $338K of aborted acquisition costs and $1.6M of redundancy costs to give an operating loss $6.4M worse than last time. Finance expenses increased marginally but there was a $457K swing to a tax credit to give a profit for the period of $153K, a decline of $6M year on year.

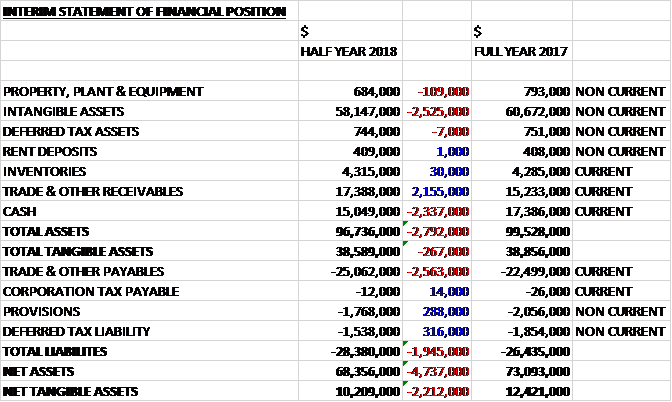

When compared to the end point of last year, total assets declined by $2.8N, driven by a $2.5M reduction in intangible assets and a $2.3M decrease in cash, partially offset by a $2.2M growth in receivables. Total liabilities increased during the period due to a $2.6M growth in payables. The end result was a net tangible asset level of $10.2M, a decline of $2.2M over the past six months.

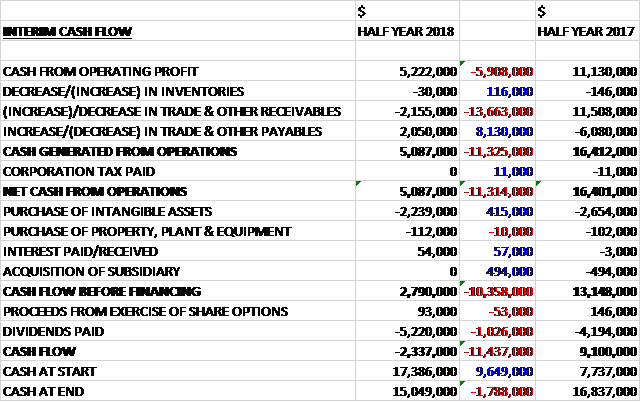

Before movements in working capital, cash profits declined by $5.9M to $5.2M. There was a modest cash outflow from working capital compared to a large inflow last year and with tax payments remaining broadly flat, the net cash from operations was $5.1M, a decline of $11.3M year on year. The group spent $2.2M on intangible assets and $112K on fixed assets to give a free cash flow of $2.8M. This didn’t cover the $5.2M paid out in dividends so there was a cash outflow of $2.3M in the first half and a cash level of $15M at the period-end.

Software and service revenues increased by 24% as a result of growth across Amino TV, Amino OS software and support for their Amino View devices. Device revenues declined as a result of the change in phasing of orders by one of their major customers in North America and they expect this trend to reverse in the second half of the year.

The group’s performance in the North American market was impacted by the phasing of orders received from a major customer, more of which will be recognised in the second half of the year than the first half. They continue to see sustained growth for their software-based service assurance platform which is becoming a key element in operators’ efforts to drive down operational costs through improved remote troubleshooting and device self-installation.

Latin America was broadly flat but the group have made good progress with follow on orders from key customers and secured a significant new contract with a major regional operator. European sales recovered after a period of decline with a long-standing customer restarting orders in the second half of last year. Following on from the DELTA launch of multiscreen services, Dutch regional provider Kabelnoord will also deploy the Amino TV platform to support a new service rollout in the second half of 2018. A contract win with T-2 in Slovenia to support their deployment of 4K UHD services was also announced during the period.

Operationally they have been mitigating ongoing pricing pressure on key device components such as silicon, memory and MLCCs. The focus on supply chain management continued to mitigate, where possible, price increases for customers and hence this pricing pressure does not alter the board’s confidence in meeting their previous expectations for the full year. They expect further pressure on component pricing and availability for the rest of the year, however.

At the start of the year, Dutch operator DELTA deployed the group’s Amino TV video delivery platform as part of a major project to transition their existing cable TV subscriber base to an all IP-based multiscreen service model. As well as delivering significant bandwidth savings, the operator also deployed their service assurance platform to provide a range of further cost efficiencies including customer self-installation.

Initial orders for operator ready Android TV devices have been secured in North America as demand is driven by their differentiated operator ready solution which adds their own software capabilities to the underlying Android platform. During the period they updated the platform to the latest Android O version and have also carried out a series of marketing workshops at industry events with Google partners in Europe, North America and Asia.

In March the group completed the final stage of rationalising their three R&D centres into two which resulted in $1.4M of annualised costs reductions. This also led to $1.6M of restructuring costs in the period. In addition, $300K of costs were incurred in potential acquisitions which were aborted following the completion of phase one of due diligence.

The group entered the year with a strong order backlog and have seen growing demand for their solutions with 40% more orders during the first half than in the corresponding period last year. As a result they entered July with 75% of their forecast revenue for the full year secured, in line with the same point of last year. The board is confident on delivering a full year performance in line with its previous expectations.

At the current share price the shares are trading on a PE ratio of 14.6 which falls to 12.4 on the full year consensus forecast. After a 10% increase in the interim dividend the shares are yielding 3.7% which is expected to fall to 3.6% on the full year forecast. At the period-end the group had a net cash position of $15M compared to $16.8M at the same point of last year.

Overall then this has been a bit of a difficult period for the group. Profits have declined, net assets decreased and the operating cash flow decreased. The group still managed to make some free cash, but this did not cover the dividend payments. The software and services division performed well but the device division saw profits fall due to the phasing of orders from a large North American client. This will apparently reverse in the second half. The group is also suffering some price pressure. The shares offer decent value with a forward PE of 12.4 and yield of 3.6% but there is a lot riding on the second half and I am somewhat cautious.

On the 8th October the group released a trading update covering the year ending 2018. They expect pre-tax profit to be around $11.5M reflecting an intensification of external macroeconomic headwinds. This has resulted in lower than expected orders and higher than expected component price increases in the second half of the year.

They have seen customer decisions on orders delayed in the second half because of instability in the economies of certain emerging markets, planned trade tariffs in the US which have created confusion among customers, and the diversity and depth of change in the industry. In addition they expect component prices to continue to increase in the near future.

The group remains profitable and cash generative but it is hard to see how long this state of affairs will continue for so I feel it is prudent to sell out here.

On the 6th December the group released a trading update covering the full year. They expect to report trading in line with market expectations.