Somero has now released their interim results for the year ending 2018.

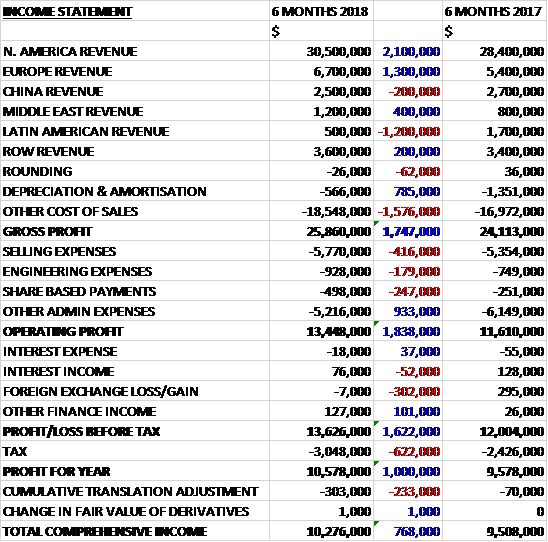

Revenues increased when compared to the first half of last year as a $1.2M decline in Latin American revenue and a $200K fall in Chinese revenue was more than offset by a $2.1M growth in North American revenue, a $1.3M increase in European revenue and a $400K growth in Middle East revenue. Depreciation and amortisation decreased by $785K but other cost of sales were up $1.6M to give a gross profit $1.7M higher. Selling expenses increased by $416K, engineering expenses were up $179K and share based payments grew by $247K but other admin expenses fell by £933K to give an operating profit $1.8M higher. There was a $302K detrimental swing in to a forex loss and the tax charge increased by $622K to give a profit for the half year of $10.6M, a growth of $1M year on year.

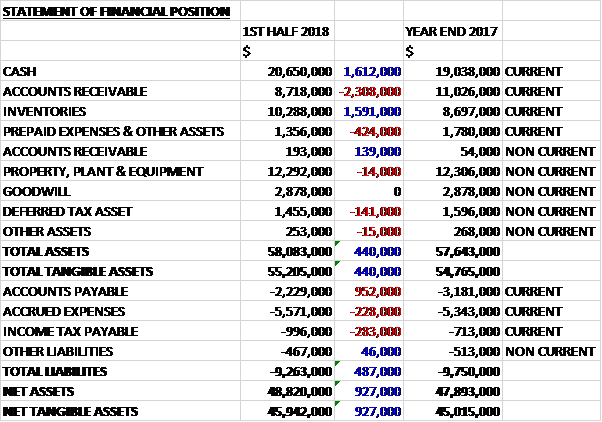

When compared to the end point of last year, total assets increased by $440K, driven by a $1.6M growth in cash and a $1.6M increase in inventories, partially offset by a $2.3M decline in accounts receivable and a $424K decrease in prepaid expenses. Total liabilities declined during the period as a $283K growth in tax payables and a $228K increase in accrued expenses was more than offset by a $952K decline in accounts payable. The end result was a net tangible asset level of $45.9M, a growth of $927K over the half year period.

Before movements in working capital, cash profits increased by $335K to $12.3M. There was a broadly neutral working capital situation compared to a cash outflow last time so the cash from operations was $12.3M, a growth of $2.9M year on year. The group spent just $553K on capex to give a free cash flow of $11.8M. Of this, $9.2M went on dividends, $541K on RSUs and $83K on stock options settled for cash to give a cash flow for the period of $1.9M and a cash level at the period end of $20.7M.

In North America, non-residential construction activity remained strong and the group’s customers reported project backlogs that extend well into 2019, underpinning their growth prospects. In the period there was a sales increase of 7% as sales of boomed screeds, ride-on screeds and other revenues all increased compared to the prior year. With robust market conditions and customer confidence the board expect solid second half trading in this key market.

The European market continued to perform well with sales up 24%. Broadly across the continent non-residential construction market conditions remained healthy and activity levels high, highlighted by the sale of equipment in 14 countries across Europe. The UK, Germany and France were the main contributors to growth.

In China first half sales were $200K lower in the period. Despite this the board are encouraged by the positive impact of marketing and demand generation activities they started and in addition, they hired a China National sales director.

The Middle East saw sales up $400K with ROW territories increasing by $200K. The Middle East reported sales in the UAE, Egypt and Turkey while in the ROW territories performance was led by meaningful contributions from Australia and India. In Latin America, while sales decreased by £1.2M they look for meaningful improvement as they have a solid pipeline of opportunities arising from anticipated second half customer projects and as overall activity in the territory remains healthy.

During the period the group’s revenue growth was in part driven by the launch of the S-22EZ, introduced in late 2017, that positively impacted their boomed screed sales which grew by 13%. In addition, sales of the SP-16 Concrete line pilling and placing system, a new product launched in early 2017, continued to grow reaching $700K in sales in the period. They are also pleased with the progress they have made on developing new products including the testing of prototype machines that target the high rise structural market segment as well as in identifying new product ideas to add to their long term pipeline.

The group are continuing to evaluate plans for expending their Fort Myers and Houghton facilities to accommodate future growth. Previously they reported that they expected the project cost associated with expanding their Fort Myers HQ would amount to $1.3M and this continues to be the case. In addition with their core business growth and the introduction of new products in the coming years they expect the need to expand their Houghton facility. Before committing capex to expand either, however, they will complete a full assessment of the impact of planned growth from their core business and new products. This assessment is expected to be completed by the end of H1 2019.

The positive momentum experienced in North America has carried over into the second half reflecting robust non-residential construction markets and a high level of confidence by their customer base. Positive market conditions and healthy customer project backlogs give the board confidence in delivering a solid performance in the region in the second half.

The momentum of trading activity in Europe is also expected to carry over to H2 and the board expect the market will continue to be driven by demand for replacement equipment and technology upgrades as well as interest in new products. In China they are aiming to gain traction in the second half with the sales and marketing initiatives launched at the beginning of the year starting to deliver returns, in addition to positive contributions to market performance over the medium term from the recently added local leadership.

In the Middle East they expect to see a continuation of the first half performance for the rest of the year while in Latin America they expect H2 will improve due to the meaningful opportunities and solid level of activity across a variety of countries. In their ROW territories they also anticipate that the solid first half performance will continue through the remainder of the year and are particularly pleased with the traction being gained in the Indian market.

Overall they see strong activity across their entire geographic footprint and strong interest across their product categories in H2. The board remains confident in delivering another year of profitable growth in line with current market expectations.

At the current share price the shares are trading on a PE ratio of 15.8 which falls to 12.8 on the full year consensus forecast. After a doubling of the dividend the shares are yielding 3.6% which increases to 5% on the full year forecast. At the period-end the group had a net cash position of $20.7M compared to $18.3M at the end of last year.

On the 12th September the group announced that Chairman Lawrence Horsch sold 46,000 shares at a value of £190K. He now owns just 46,000 shares in the company.

Overall then this has been another period of decent progress for the group. Profits were up, net assets increased and the operating cash flow improved with a decent amount of free cash being generated. The North American, European, Middle East and Indian markets are all performing well and whilst South America slipped this time, the group expect this to improve in the second half. China also saw a decline and with China being China it is hard to see if this will improve or not. In any case the forward PE of 12.8 and yield of 5% looks OK for this company. The main risk, of course, being a global downturn which seems a little closer than it was.

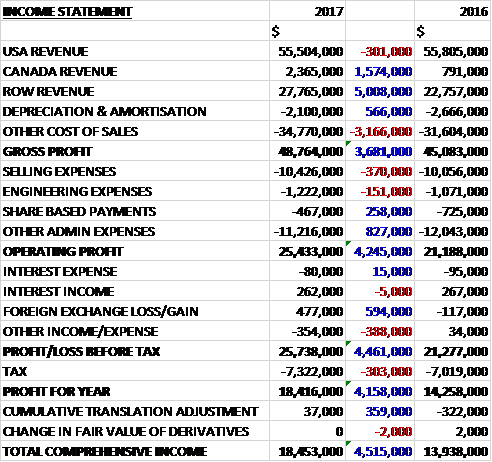

On the 16th January the group released a trading update covering the year as a whole. They delivered strong, profitable growth and healthy cash generation in the second half of the year and the board now expects 2018 revenues and EBITDA will be moderately ahead of market expectations driven by volume increases and effective management of operating costs. In addition, they expect net cash to be more significantly ahead.

Three of the group’s six regions grew, led by a strong performance in North America and ROW territories along with a positive contribution from the Middle East. Europe and China were slightly down on 2017 while in Latin America trading fell below 2017 levels, albeit with H2 improving on H1.

In North America the strong H2 trading reflects the strong pipeline of construction projects that remain for the US customer base. The growth in ROW territories was led by a significant contribution from Australia along with positive contributions from Scandinavia and India. In the Middle East, activity levels were solid throughout the year leading to the increase compared to 2017. In Europe, while trading ended slightly below 2017 levels, the group saw healthy demand for new products and technology upgrades, in addition to opportunities to refresh the installed base of equipment.

In China the group is pleased with its efforts to refine its strategy to target the quality market segment, although these efforts have yet to gain full traction. In Latin America, trading improved in the second half of the year and the group is encouraged by the addition of future product opportunities in this market. On a product basis, growth in H2 was balanced with sales in all product categories increasing, led by a particularly strong performance in the ride-on screed category.

Going forward, the board is confident in the group’s ability to deliver another year of profitable growth in 2019. The underlying market conditions in their North American and European markets remain buoyant and the board sees meaningful growth opportunities in China and their other territories alongside growth opportunities from new products.

On the 16th January the group announced the acquisition of Line Dragon, a US-based provider of concrete placing and hose dragging equipment to the concrete industry. Line Dragon complements the group’s SP-16 Concrete Line Placing and Pulling system with the combined offering introducing innovative features to customers and expanding their customer relationships in this market segment.

Last year, the business generated revenues of $2M and is expected to have a slight positive impact on 2019 earnings. The group paid $2M in cash with ongoing performance payments based on a percentage of future sales, which are not expected to be material to the group.