TT Electronics have now released their interim results for the year ending 2018.

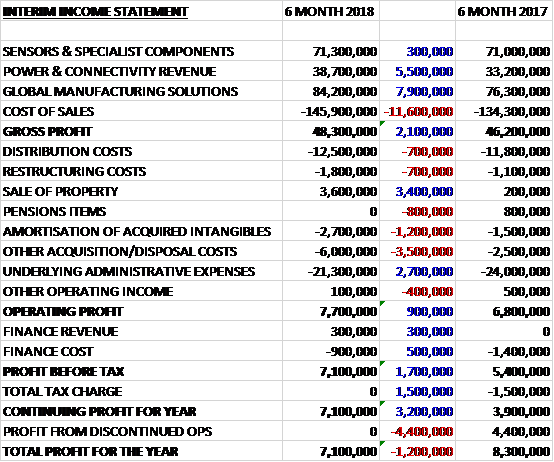

Revenues increased when compared to last year due to a £7.9M growth in global manufacturing solutions and a £5.5M increase in power and connectivity revenue with sensors and specialist components remaining broadly flat. Cost of sales also increased to give a gross profit £2.1M higher. Distribution costs increased by £700K, restructuring costs increased by £700K, there were no pension items, which brought in £800K last time, there was a £1.2M increase in the amortisation of acquired intangibles and a £3.5M growth in other acquisition and disposal costs, offset by a £3.4M increase in property sales and a £2.7M decline in other admin expenses. All this meant that the operating profit was £900K higher. Finance costs reduced somewhat and tax charges were down £1.5M. Offsetting this was the lack of £4.4M profit from discontinued ops and the profit for the period came in at £7.1M, a decline of £1.2M year on year.

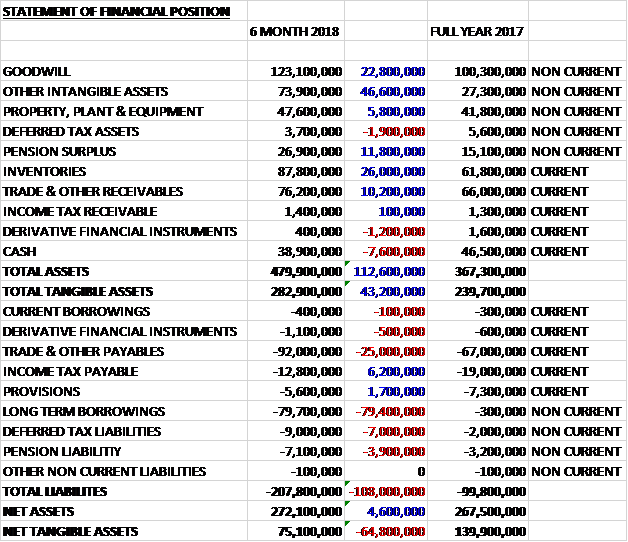

When compared to the end point of last year total assets increased by £112.6M driven by a £22.8M growth in goodwill, a £46.6M increase in other intangible assets, a £26M growth in inventories, an £11.8M increase in the pension surplus and a £10.2M growth in receivables, partially offset by a £7.6M decrease in cash. Total liabilities also increased due to a £79.5M increase in borrowings, a £25M growth in payables and a £7M increase in deferred tax liabilities. The end result was a net tangible asset level of £75.1M a decline of £64.8M over the past six months.

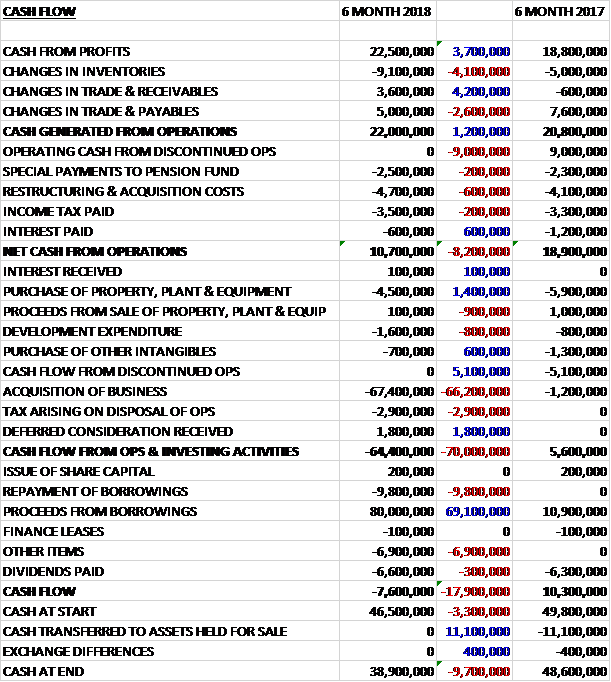

Before movements in working capital, cash profits increased by £3.7M to £22.5M. There was a slight cash outflow from working capital and a £9M reduction in the operating cash inflow from the disposal so the net cash from operations came in at £10.7M, a fall of £8.2M year on year. The group spent £4.5M on fixed assets, £1.6M on development expenditure and £700K on other intangible assets. They received £1.8M in deferred consideration but this was offset by a £2.9M tax payment relating to the disposal and a £67.4M payment for the acquisition. This meant that before financing there was a cash outflow of £64.4M. They took out a net £70.2M in new borrowings, paid out £6.6M in dividends and £6.9M on “other” items, whatever that refers to? The end result was a cash outflow of £7.6M in the first half and a cash level of £38.9M at the period-end.

The underlying operating profit at the Sensors and Specialist Components business was £9.9M, a growth of £1.3M year on year. The group have seen strong market demand continuing across the division and margins improved by 190 basis points due to increased volumes, operational efficiency and an improved product mix. In the UK facility they have continued to make capacity improvements which have enabled them to deliver a record output. In the US they have been increasing output to meet new demand for a high-reliability signal conditioning platform of products which precisely measure signals in electronic circuits. This platform of products is now in its ramp up phase and has contributed to growth in the period.

They continue to see growth in their automotive power inductors product line, driven by the technological advancements for electric and hybrid electric vehicles, and the team won a new European customers in the period. In the medical market the increasing demand for portable medical devices is resulting in increased demand for the group’s solutions. Customer wins have included two medical equipment manufacturers for applications in portable medical monitors.

They launched three new sensing and power management products from their new product and testing cell in Bedlington including a smaller sized power management component able to withstand high current surges in an electronic circuit. The power management component can be used in applications across aerospace, military, comms, medical and industrial markets where the proliferation of electronics requires more advanced and reliable circuitry components.

The underlying operating profit at the Power and Connectivity business was £2.5M, a decline of £900K when compared to the first half of last year although revenues increased by 17% due to the acquisitions. The fall relates largely to the absence of the high margin one-off sales relating to the last time buy activity in the US and £600K of additional one-off investment to meet customer schedules and build capacity to support anticipated future growth. The profit contribution from acquisitions was £1.1M.

The “more electric aircraft” continues to drive a pipeline of demand, Projects they have been working on include a development contract with a strategic partner for a fuel reduction initiative in aircraft, volume ramp-up of products linked to the A350 aircraft platform, and the extension of their capabilities into service support for engine test requirements. Growth in these areas is offsetting the expected reduction in revenue related to the 777 and A380 platforms.

To support current demand patterns and to provide capacity for future growth, they are transferring a number of product lines from the UK to Malaysia where they have established an aerospace capability. They have also established a new product introduction and prototype lab in the UK to service the pipeline of new business opportunities. During the period they won a supplier award from a global engine manufacturer for their work on hybrid microsystems.

Stadium’s Technology Products business forms the group’s new connectivity offering and has been incorporated into this division. Their connectivity offering allows systems to communicate with one another and transmit data wirelessly. Their solutions include connectivity, low power supplies and human machine interface products. The business is performing in line with expectations. They are increasing investment to support the development of these products and a range of new platform products.

The underlying operating profit at the Global Manufacturing Solutions business was £5.9M, an increase of £3.4M when compared to the first half of 2017 with organic revenue growth driven by demand in Asia and North American medical customers. The operating profit contribution from acquisitions was £300K. Margins increased by 360 basis points with the improvement particularly strong in China where the group have been adding more engineering services. The improvement in profitability was largely a result of operational leverage on revenue growth and efficiencies which have driven improvement in the European business. The improvement was also supported by a short term favourable purchase price variance and transactional forex gains of £500K which are not expected to recur.

The demand for technological advancements in the medical market, particularly in developing regions such as Asia, is driving demand for the group’s products. During the period they won a contract with a new medical customer for printed circuit board assembly for a new digital mammography device for breast screening. In the industrial market they won contracts with two new customers including a contract with a new Japanese customer to develop PCBAs for lumiscopes. In addition they have won a contract with a US based technology company for PCBAs for industrial radio remote controls.

They won a PCBA contract with an aerospace and defence customer that has been a longstanding customer in their Power and Connectivity division with the PCBAs used in navigation applications including in GPS systems.

They continue with their focus on operational improvement to drive margin improvement. During the period they closed the facility in Romania, moving product lines to the UK and China. Their European operations have been improving and during the period they won a new customer with a European marine company.

The group are changing their approach to business development to reflect the increasingly design-led focus of the business which requires them to develop more strategic relationships with their customers. They are providing their sales force with new tools and developing their skills through training to improve their success in selling engineered product solutions and higher-value components capabilities.

In April the group acquired Stadium PLC for £45.8M in cash and the assumption of net debt of £13.9M. The business contributed an operating profit of £1.2M in the two and a half month period since acquisition. Stadium is a provider of connectivity solutions across industrial, transportation, medical and aerospace and defence markets. The integration is progressing well with expect cost synergies to date being realised. Costs addressed include the removal of duplicate PLC costs and some initial procurement savings have been identified. The net cost synergy expectations remain unchanged but the evaluation of Stadium’s product capabilities combined with the group’s market presence and scale points to future potential revenue upside.

Previously Stadium split its revenues between Technology products and electronics assemblies. The technology products businesses are being integrated into the newly named Power and Connectivity division whilst electronic assemblies is being integrated into the global manufacturing solutions division.

In June the group acquired Precision Inc for an initial consideration of £17.6M in cash and up to an additional £3M of contingent consideration. In the month since acquisition the business contributed £100K in operating profit. The Stadium acquisition generated goodwill of £14.3M with the Precision acquisition generating £6.8M. Precision is a designer and manufacturer of precision electromagnetic product solutions for critical applications, primarily in medical markets. The business is being integrated into the Power and Connectivity division.

In October last year the group disposed of the Transportation Sensing and Control division to AVX Corp for £125.6M in cash. The gain on disposal was £26.3M and the business generated a profit of £4.4M in the first half of last year.

Going forward, the first half performance and order momentum give the board confidence of progress for the full year ahead of their prior expectations.

At the current share price the shares are trading on a PE ratio of 24.9 which falls to 16.4 on the full year forecast. After an 11% increase in the interim dividend the shares are yielding 2.5% which increases to 2.7% on the full year forecast. At the period-end the group had a net debt position of £41.2M compared to a net cash position £47M at the start of the year.

On the 9th August the group announced that non-executive director Neil Carson purchased 40,000 shares at a value of £103K.

Overall then it is quite hard to get at the underlying performance of this company as there is a lot of noise but it seems to have been a decent period. Profits declined but this was due to no contribution from the disposed business and continuing profits increased. The sale of a property broadly offset the increase in acquisition costs. Net tangible assets fell due to the acquisitions and the operating cash flow reduced, although again the continuing operating cash flow improved. There was no free cash due to the acquisitions but even excluding them, the free cash did not cover the dividends.

The Sensors and specialist components division performed well with strong underlying growth. The Global Manufacturing Solutions division also saw an improved performance due to increased demand from medical customers in Asia and North America, improved efficiencies and one-off forex gains. The Power and Connectivity division saw a worse performance, however, due to the non-repeat of a large US order this year and investments made to cover potential future growth – increased costs basically. With a forward PE of 16.4 and yield of 2.7% these shares aren’t a massive bargain but the expected outperformance is a positive and I continue to hold for now.

On the 13th November the group released a trading update to the end of October. Trading has continued to be positive. For the year to date organic revenue is up 5% with all three divisions growing over the last four months and good revenue, profit and order momentum across all three divisions is expected. They have continued to see positive order intake across all divisions and the order book continues to be strongly ahead of last year, supporting their confidence in the improved growth continuing for the remainder of the year and into the early part of next.

The integration of Stadium is progressing well and the acquisitions are performing in line with expectations. In response to opportunities in connected devices highlighted from the integration of Stadium, in October they opened an Advanced Technology Centre in China.

In November they signed an agreement to establish a joint venture with their long-term supply partner Uniroyal for sensing and power management devices. Uniroyal is the world’s second largest manufacturer in this growing technology. The partnership with combine the group’s design engineering and global distribution channels with Uniroyal’s penetration of the Asian market and higher volume manufacturing capabilities to target the automotive, industrial automation and other high volume market segments. Revenues from the joint venture are expected to start in H2 2019. They expect in invest $4.5M in 2019 and to significantly exceed their 12% roe capital hurdle in 2020.

Following a first half with good revenue growth and significant margin improvement, momentum has strengthened in H2. They are on track with their plans for the year as a whole and confident of meeting the enhanced expectations they set out at the interims. All this sounds very good, I might have taken profits too early? I am tempted to buy back in.

On the 7th December the group announced that non-executive director Jack Boyer purchased 11,792 shares at a value of £25K.

On the 4th January the group announced that non-executive director Michael Baunton purchased 5,000 shares at a value of £10K.

On the 28th January the group released a trading update to the end of December which was positive and in line with plans. The year finished with a good performance across the business, in line with guidance, with good revenue growth and a strong order book.