Sylvania Platinum have now released their final results for the year ended 2018.

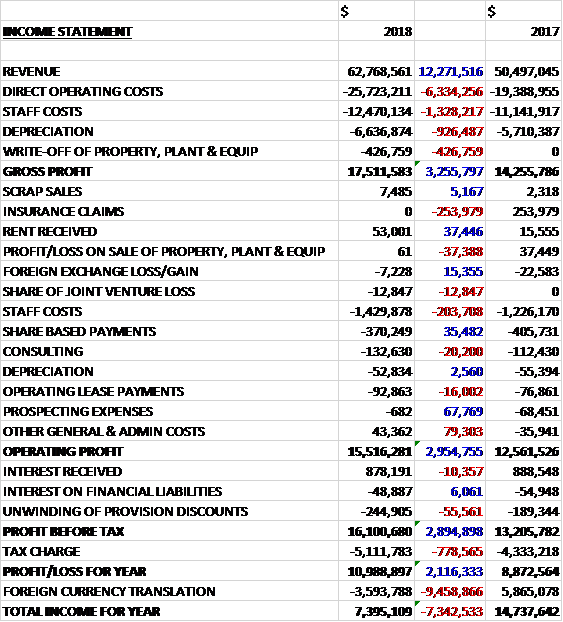

Revenues increased by $12.3M when compared to last year. Direct operating costs were up $6.3M, staff costs increased by $1.3M, depreciation increased by $926K and there was a $427K write-off of property, plant and equipment to five a gross profit $3.3M higher. There were a $68K reversal of prospecting expenses but there were no insurance claims, which brought in $254K last year, staff costs were up $204K and other general costs increased by $186K to give an operating profit $3M higher. Tax charges increased by $779K and there was a $56K increase in the unwinding of provision discounts which meant that the profit for the year was $11M, a growth of $2.1M year on year.

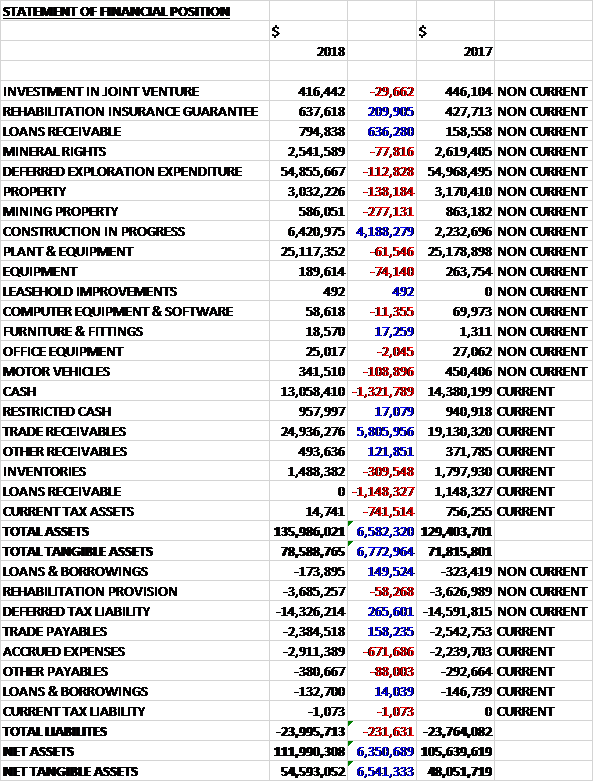

When compared to the end point of last year, total assets increased by $6.6M driven by a $5.8M growth in trade receivables, and a $4.2M increase in construction in progress, partially offset by a $1.3M reduction in cash. Total liabilities also increased during the period due to a $672K growth in accrued expenses. The end result was a net tangible asset level of $54.6M, a growth of $6.5M year on year.

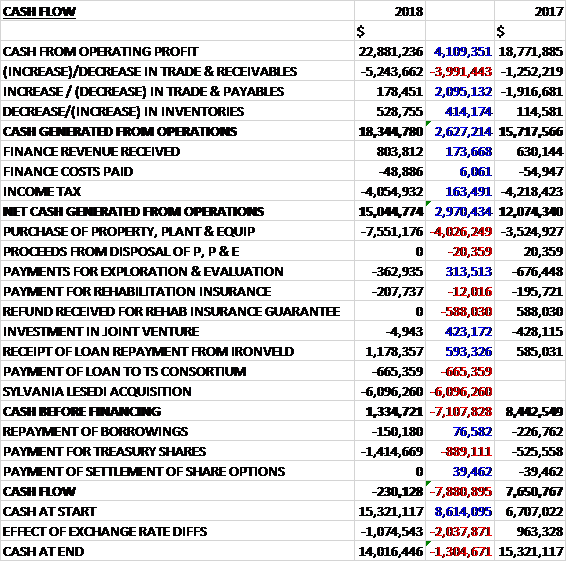

Before movements in working capital cash profits increased by $4.1M to $22.9M. There was a modest cash outflow from working capital but finance revenue increased by $174K and tax payments fell by $163K to give a net cash from operations of $15M, a growth of $3M year on year. The group spent $7.6M on property, plant and equipment, $363K on exploration, $208K on rehabilitation insurance, $665K in loan repayments to TS and $6.1M on the Lesedi acquisition. They did receive $1.2M in loan repayments from Ironveld, however, to give a free cash flow of $1.3M. Some $1.4M was spent on share buybacks to give a cash outflow of $230K for the year and a cash level of $14M at the year-end.

Overall despite a production wobble due to delays at Millsell where licensing of the newly constructed tailings facility was protracted, and at Tweefontein where power supply was erratic, the group have come in within their revised guidance, albeit at the lower end. Reliable power supply presents a serious cause for concern while the ongoing issues at their national power utility continues to hamstring opportunities in the mining sector.

The SDO delivered 71,026 ounces in the year which was a fifth year of record production. A 6% improvement in tons treated helped to mitigate the impact of an 11% lower feed grade and a 3% decrease in recovery efficiency associated with a delay in authorisation of the water use license at the Millsell operation. After the approval of the license in January 2018 the tailings dam at Millsell has been operating well and feed grades have returned to planned levels. The planned closure of the Steelpoort plant in June 2017 had a further impact on PGM production but this was mitigated by the acquisition of Lesedi.

The SDO cash costs increased by 20% in Rand terms while the dollar cost increased by 27% to $543 per ounce. The cost increases were largely due to one-off costs associated with ensuring the Lesedi operation’s profitability and the delayed commissioning of the tailings dam at Millsell. Overall group cash costs increased by 25% to $567 per ounce as Steelpoort, among the lowest costs plants, came to the end of its life. The acquired Lesedi plant has a much higher operating cost, although the group have identified a number of cost saving strategies and is making steady progress in that regard.

The average gross basket price for the year was $1,135 per ounce, a 21% increase on the prior year. Although the Platinum and Palladium prices fell sharply in H2, the group benefited from the higher Rhodium price.

Project Echo is proceeding well with the Millsell and Doornbosch MF2 modules commissioned during the year. While commissioning of Millsell did not proceed as planned, it is on track to deliver as promised. Tweefontein was deferred due to power problems which they may have to endure for longer than previously expected. As a result the roll out of Mooinooi is being fast tracked and they are looking at an opportunity to place MF2 at Lesedi.

They plan to move the redundant chrome separation plant from Steelpoort to Lesedi to allow for a higher chrome feed into the plant that will also enable chrome removal.

The group cannot develop their exploration assets with the current platinum price below $800 an ounce. The Department of Mineral resources has not communicated any progress in the appeal lodged in June against the decision to grant a mining right application to the company. The group’s environmental consultants are apparently following up regularly on this matter. No further work has been done on phase one of the Grasvally Bulk sample. They have received word that the mining right for the project has been granted.

In November the group acquired Phoenix Platinum for a consideration of $6.3M. In the eight months since acquisition the business contributed a profit of $329K to the group’s results. No goodwill was generated. Lesedi’s integration has been relatively smooth. With the plant producing the highest number of ounces ever achieved in December. The synergies are proving their worth.

The company began a share buyback programme during the year. Due to their initial domicile in Australia, 40% of shareholders owned 3% of the register with little opportunity to trade. It was impractical to maintain a register of shareholders outside the UK trading platform and the programme aimed to assist this group of shareholders to obtain fair value at minimal cost. Around 57% of non-UK shareholders were bought out. At the close of the period, the cost of the programme amounted to $369K with 2,281,570 shares bought. This rose to $388K and 2,397,481 on conclusion of the programme.

The past year has ended with the platinum price the same as it was after the 2008 financial crisis and they don’t expect this to improve while supply continues to exceed fundamental demand. The board remain concerned about the platinum price but their revenues have increased due to higher rhodium and palladium prices.

The board expect a further increase in production when they realise the full year benefits of Lesedi, the parts of project Echo that are due to be completed alongside ongoing efficiency improvements in the plants and they have set a production guidance of between 76,000 and 78,000 ounces in 2019. They expect a 6% to 10% increase in output due to the further roll out of project Echo.

At this point they do not see a recovery in the price of platinum going forward but they anticipate a modest improvement in net profit.

At the current share price the shares are trading on a PE ratio of 5.9 but this increases to 6.9 on next year’s consensus forecast. After re-writing the dividend policy, a maiden dividend has been announced which represents a yield of 2%. This is expected to remain the same next year.

Overall then this has been a fairly decent year for the group. Profits increased, net assets grew and the operating cash flow improved with a small amount of free cash being generated. The production levels have been maintained despite the closure of Steelpoort, issues with the licensing of the new tailings facility and power supply problems at Tweefontein, the latter of which seems to be an ongoing issue. The acquisition of Lesedi offset all these issues but it should be noted that Lasedi is currently much higher cost than Steelpoort was, although this is being addressed.

The improvement in profit is also due to an increase in the basked price. This is entirely due to the higher price of Rhodium as Platinum did not have a good year. Project Echo seems to be progressing OK but while the platinum price remains low these shares are a little risky. That being said it is a well-run company with a forward PE of 6.9 and maiden dividend of 2% so I am tempted to hold on here.

On the 31st October the group released a trading update covering Q1. The group produced 19,137 ounces which was the second highest quarterly production, although down slightly on Q4, impacted by some operational instability and teething issues at Doornbosch and Mooinooi which have since been resolved. Group EBITDA was $7.1M with operating costs down 2% in rand terms and 12% in dollar terms.

PGM feed grades remained static but the PGM plant feed tons and recovery efficiencies were both 3% lower. The lower feed tons was primarily due to the downtime and feed instability associated with the commission of a new process coil at Doornbosch as well as come operational challenges at Mooinooi during September. Recovery efficiencies were impacted by a lower percentage of fresh current arisings feed to some operations as well as oil contaminated feed material received at Mooinooi that negatively affected the PGM flotation process.

The cash costs for the period in rand terms increased 2% which was attributable to lower ounce production. In USD terms the cash costs decreased by 8%, however, to $508 per ounce due to forex movements. Capex reduced 20% in line with the Project Echo construction plan.

Operational challenges experienced at Millsell after the commissioning of the MF2 module earlier this year resulted in some design changes and upgrades to flotation mechanisms which will enable improved PGM recoveries in Q2. Process circuit modifications, using enhanced fine screening technology, at Doornbosch, Millsell and Tweefontein will be completed in Q2 and optimisation of these new circuits will be done after commissioning in order to further improve feed grades.

The MF2 module for Mooinooi, which is being fast tracked to counter the delay in the execution of the Tweefontein module is progressing well. The Lesedi chrome plant project, comprising of the dismantling and relocation of the redundant Steelpoort chrome circuit, has started and is expected to be completed in H2 of this year. This will enable chrome removal ahead of Lesedi’s PGM plant, aligned to the standard SDO operating model, and will contribute to higher feed grades.

The gross basket price decreased by 2% to $1,149 per ounce which, along with the lower production figures, saw net revenue reduce by 14% to $17.2M, although this was in line with board expectations.

Platinum has remained in the $800 range but Palladium has continued its steady increase, up 15%. Rhodium increased 10% and appears to be continuing this upward trend. In light of the current South African political environment the exchange rate remains just as volatile for most of the quarter and continues to be monitored.

On the 31st January the group released an update for Q2. The SDO delivered 14,907 ounces, a 22% decrease over Q1. The feed grade decreased 5% and PGM plant feed tonnes decreased by 15% which together with the 3% decrease in recovery efficiency resulted in the reduction in ounces produced.

The lower PGM plant feed tonnes was primarily due to significant downtime experienced during November and December at Lesedi due to water shortages in the area. This resulted in the plant only being able to treat 45,800 tonnes compared to a planned 86,700. Significant downtime and feed instability at Doornbosch’s dump re-mining where the current dump is reaching its end of life also contributed to the decrease.

Lower production at both Tweefontein and Millsell host mines during the quarter following safety stoppages and PGM reed grades and recovery efficiencies across operations were lower due to the lower percentage of fresh current arisings feed received from the host mines during their annual mining break.

The total operating costs for the period decreased 6% in ZAR terms but due to lower production, the unit cost increased by 22%. In USD terms costs increased by 19% to $606 per ounce. A three year wage agreement was concluded with the union for the Western Operations which is in line with the SDO cost forecasts going forward.

Extreme summer heat conditions presented a challenge at many operations in terms of water availability but Lesedi in particular was badly affected due to the absence of current arisings or tails slurry from the host mine. Mitigating actions to address the water shortage include both optimising of process parameters to reduce water consumption, as well as evaluating and implementing alternative water supply measures. The Lesedi team have drilled several new boreholes and engaged with host mines and neighbouring operations in order to secure adequate water for continuous operation and will continue these initiatives. Since January, after some rain and supply improvements, water availability improved significantly but the issue has not been fully resolved and will remain a key focus area.

At the Doornbosch operation at the current dump, which is at the end of its life, the lower mining benches and coarser dump material associated with the final clearing of the dump floor impacted negatively on hydro mining feed stability and caused downtime when pipe lines choked and the team had to perform certain system upgrades during recent months to address this. Since mid-January the upgraded system has been commissioned and is performing significantly better which should improve performance during the next quarter, especially when the new dump re-mining is planned to start in Q4.

The commissioning of the enhanced processed circuit modifications that use enhanced fine screening technology for more efficient upgrading of PGMs at Doornbosch, Millsell and Tweefontein was completed towards the end of Q2 and the optimisation of these new circuits should assist in improving feed grades and production in the coming quarters. The project Echo MF2 module for Mooinooi is progressing well and scheduled to be commissioned in Q4.

The Lesedi chrome plant project, comprising of the dismantling and relocation of the redundant Steelpoort chrome circuit, has started and is expected to be completed in the second half. This will enable chrome removal ahead of Lasedi’s PGM plant, aligned with the standard operating model, and will contribute to higher feed grades and production.

The gross basked price for the quarter was $1,204 per ounce, a 5% increase on Q1. Palladium and Rhodium continued their upward trend, continuing into January but Platinum remained under pressure. The decline in revenue was due to the decrease in production. Total operating costs decreased by 6% in ZAR terms but cash costs per ounce were up 22% as a result of the lower ounces. In dollar terms, cash costs increased from $531 to $635 per ounce. The all in sustaining cots also increased as a result of the increase in capex and lower production, growing from $593 per ounce to $821 per ounce.

The cash balance at the period-end was $20.2M, a $2.5M increase. The operating cash flow was $5.4M with a $2.9M net increase in working capital movements.

At Grasvally the mining right granted in Q4 has been executed and is being registered in the Mining Titles Office and rehabilitation of the historical mining area has now commenced. Sales agreements are in place and the historical dump material will soon be sold as low grade chrome ore. The group has appointed a consulting company to prepare financial models as a back up to a possible sale process of the resource.