Dechra Pharmaceuticals have now released their final results for the year ended 2018.

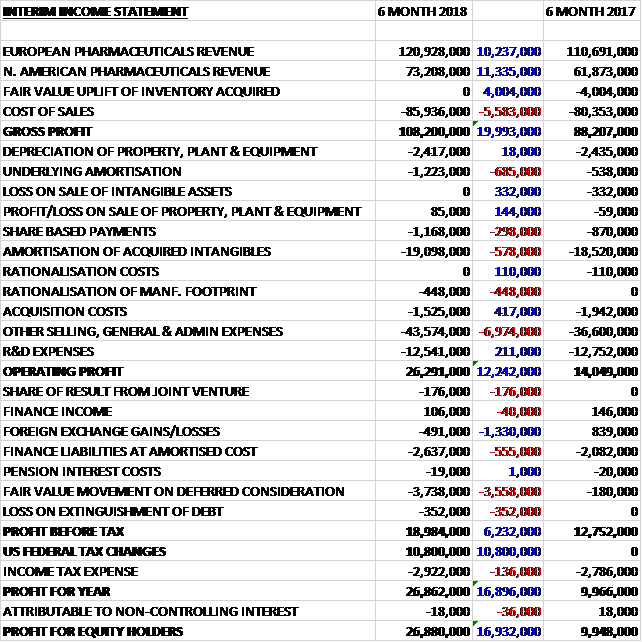

Revenues increased when compared to the last year due to a £31.8M growth in European revenue and a £16.1M increase in North American revenue. Cost of sales also increased to give a gross profit £30.7M higher. R&D amortisation charges fell by £3.4M but other pharmaceutical R&D charges increased by £3.3M to give a broadly stable picture. Underlying amortisation increased by £658K and other “underlying” admin expenses were up £10.2M. The amortisation of other acquired intangibles was £17.1M higher, acquisition expenses were up £1M and there was a £2.9M charge related to the rationalisation of a manufacturing organisation which was partially offset by an £809K reduction in other rationalisation costs. All of this gave an operating profit that was £886K higher. There was a £699K increase in forex gains and a £1.1M positive swing on the unwinding of discounts on contingent consideration. This was offset by a £1.8M increase in finance expenses from loans and a £400K loss on the extinguishment of debt. Tax charges swung £9.7M to the positive, which included the revaluation of deferred tax following changes in US corporate tax rates, which meant that the profit for the year was £36.1M, a growth of £10M year on year.

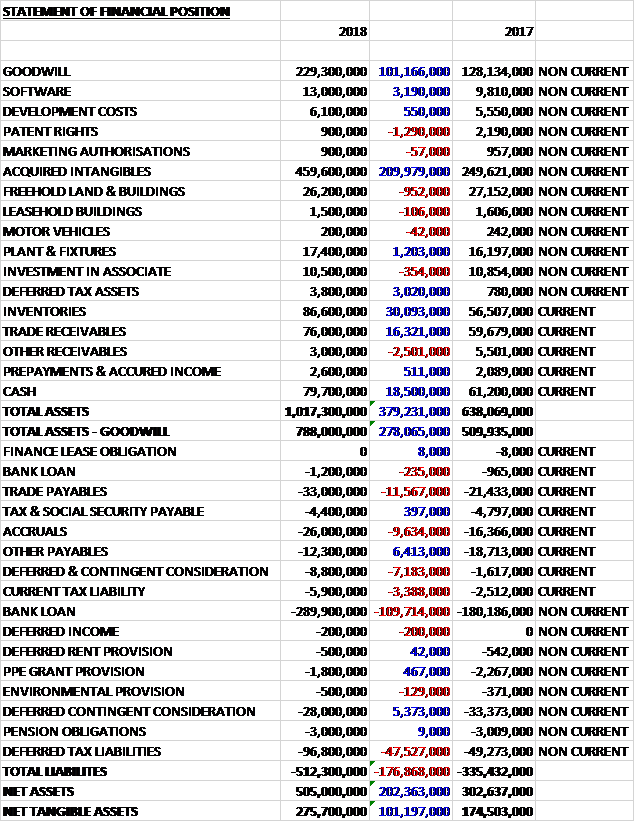

When compared to the end point of last year, total assets increased by £379M driven by a £210K increase in acquired intangibles, a £101.1M growth in goodwill, a £30.1M increase in inventories, an £18.5M increase in cash and a £16.3M growth in trade receivables. Total liabilities also increased as a £6.4M decline in other payables was more than offset by a £110M increase in the bank loan, a £47.5M growth in deferred tax liabilities (entirely due to the increase in intangible assets), an £11.6M increase in trade payables and a £9.6M growth in accruals. The end result was a net asset level (excluding goodwill) of £275.7M, an increase of £101.2M year on year.

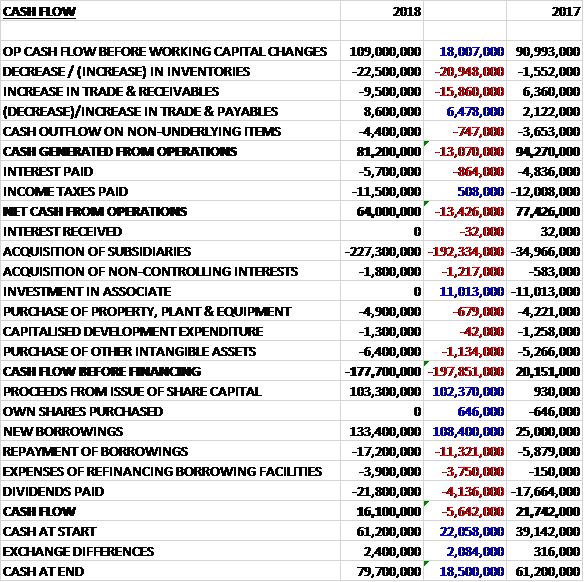

Before movements in working capital cash profits increased by £18M to £109M. There was a cash outflow from working capital and after an £864K increase in interest payments was mostly offset by a £508K fall in tax payments the net cash from operations declined by £13.4M year on year to £64M. OF this, £4.9M went on fixed assets, £1.3M on development expenditure, £6.4M on other intangible assets and £229.1M on acquisitions. This meant that before financing there was a cash outflow of £177.7M. The group also spent £21.8M on dividends. To pay for all of this, they took out a net £112.3M of new loans and received £103.3M from the issue of new shares which meant that there was a cash inflow of £16.1M for the year and a cash level of £79.7M at the year-end.

The operating profit in the European Pharmaceuticals business was £77M, a growth of £16.3M year on year with £9.5M of this increase coming from acquisitions. Segment revenues increased by 11.4% with like for like revenues up 3.7%. This performance was in line with management expectations with the majority of countries performing ahead of the market. With the consolidation of vet practices they are starting to adapt the support model with an increase in key account managers and resource for the technical support team. Whilst consolidators put pressure on margins, they deliver volume.

Companion animal products continues to perform well, especially endocrinology and anaesthesia and analgesia. Food producing animal products delivered growth of 0.4% with an ongoing pressure on antibiotic reduction. The board believe the FAP antibiotic range is now aligned for best prescribing practice and the overall portfolio is in a strong position to deliver future growth, enhanced by the range of in-house developed poultry vaccines. Equine products have performed well and sales of Osphos have continues to grow as clinical merits are more widely appreciated. The performance from nutrition was pleasing as they have addressed historic supply and palatability issues by delivering growth of 4.4%. They have now launched their refreshed cat diets with new modern packaging design to keep the product fresh once opened. They are currently embarking on a similar programme for their dog diets.

The operating profit in the North American Pharmaceuticals business was £48.3M, an increase of £5.1M when compared to last year. Revenues increased by 18.2% at constant currency. The US was the main driver of this growth but Canada also performed well. With the exception of the Carprofen chews and caplets, where sales and margin were affected by distributors marketing their own brands, growth was delivered across the entire range. Strong performers were Amoxi-Clac, following the launch of the smallest tablet size which completes the range; Vetivex IV critical care fluids, and Zycortal suspension which benefited from increased market share and additional demand in Q4 due to a competitor product being out of stock.

Sales leverage is being realised from the enlarged sales team which has benefited from a significant amount of investment over recent years. To mitigate the activity of distributors selling their own competitive products they have realigned their terms. Incorporation of vet practices in the US continues which means that the group has increased their focus on corporate account management.

Over the two years of ownership of Brovel, the Mexican subsidiary, the group have made significant changes. They have recruited completed new management. Following the registration of several Dechra products they are now able to transform the business into the Dechra brand, delisting a number of the original, low value, Brovel farm animal range. They expect Mexico to make a more meaningful contribution to their North American segment performance in 2019.

The group has identified some changes in the market. A recent significant move is the leading US vet company is taking a small presence in the UK and a significant presence in mainland Europe. Also, vet distributors who operate in Western Europe and North America are changing and beginning to increase focus on the sales and marketing of their own products. There is also ongoing consolidation of distributors, especially in the US.

Significant new product registrations were achieved in Europe including Solacyl, a water soluble powder and anti-inflammatory for turkeys; Diatrim, an antibiotic for the treatment of a wide range of infections such as cattle mastitis; Avishield IBH120, their second EU registered poultry vaccine; Avishield ND B1, their third poultry vaccine; and Tiasol, a solution to treat various infections such as swine dysentery and colitis in pigs and treatment of respiratory disease in poultry. Additionally more than 60 registrations were achieved for existing products in new EU territories.

Internationally there have been over twenty product registrations across Australia, Kazakhstan, Malaysia, New Zealand, Russia, South Korea and Thailand. In North America they have extended the range of Vetivex critical care fluids and have launched the full range of Amoxi-Clav tablets. They have also developed in house Redonyl Ultra, a soft chew dermatological supplement with an active supplement sourced through a licensing agreement with Premune AB. In Mexico Osphos, Vetoryl, Canaural and Fothyron have all been approved.

In addition to their pipeline they have in-licensing deals with Redonly Ultra, a dermatological supplement from Premune AB which has been launched in the EU; Vetradent, a water additive to combat biofilms from Kane Biotech, extending their dental range, has been launched in the US; and BioEquin, the first equine vaccing from Bioveta for herpes, has been launched in Germany. They have an agreement in place to access additional equine vaccines from the Bioveta pipeline for the major EU markets.

At the start of the year the group established DVP International in order to generate a material presence in markets outside Western Europe and North America. Good progress has been made in establishing the business with an objective of targeting the registration of their existing portfolio into target markets. The Australian business has performed well with sales growth in line with the market. They have made significant improvements to their manufacturing facility to improve efficiency and they have sufficient capacity to deliver future growth.

There were a number of non-underlying items as usual. There was an £18.7M amortisation of acquired intangibles. The fair value uplift of inventory acquired through business combinations of £5.1M is to record the inventory acquired at fair value and its subsequent release into the income statement. Expenses of £3.1M related to acquisition activities includes legal and professional fees during the acquisitions of AST and Le Vet (£2.8M) and others (£300K). There was also a £2.9M cost related to the rationalisation of a manufacturing organisation.

In February the group completed the buy-out of the remaining minority interest (4.87%) in Genera for £1.8M. Also in February they acquired the share capital of AST Farma and Le Vet, developers of generic and niche pharmaceutical products predominantly for companion animals for £229M in cash and £82.7M in shares. Both businesses are based in the Netherlands and the acquisition generated goodwill of £102.3M. Together they contributed £7.4M of operating profit in the four and a half months of ownership and would have contributed £17.3M had they been a part of the group all year.

In December the group acquired RxVet, a vet pharmaceuticals company based in New Zealand, for a total of £300K in cash. No goodwill was generated and the business contributed £11K in operating profit. Had they been part of the group for the whole year, the business would have contributed £100K.

There is some deferred and contingent consideration associated with the acquisitions. There is £22.8M for Tri-Solfen which is expected to be payable over a number of years and relates to development milestones and sales performance. During the year the development milestones have been re-measured and are now expected to happen later than initially anticipated. There is a consideration of £1.1M payable for StrixNB and DispersinB under the same terms as above.

There is a consideration of £6.6M for a new licensing agreement for an Ifate sodium injectable solution which relates to development milestones and a consideration of £2.8M for Phycox relates to sales performance. Finally there was £1.7M of other contingent consideration payable.

It is refreshing to see a clear outline of the risks that Brexit could cause the business. The primary focus is on addressing Brexit risk in the supply chain. This includes transferring UK registered market authorisations for products that are sold in the EU to an EU entity and duplication of product release testing for products that are transferred between the UK and EU.

The group has implemented a hard Brexit mitigation plan which will provide an EU based lab testing facility and staff for batch testing if this is required and the transfer of product registrations to an EU domiciled legal entity within the group. This will entail an upfront investment of £200K in capital and £1M in one-off expenses. If EU batch testing and increased customs duties is required this will result in additional operating costs of around £800K. In addition they continue to monitor the potential impact of US sanctions on their existing business with Iran where they currently sell £1.3M of products that are on the UN exempt sanctions list.

Going forward the new financial year has started well and in line with management expectations.

At the current share price the shares are trading on a PE ratio of 65.6 which falls to 26.8 on next year’s consensus forecast. After a 19% increase in the dividend the shares are yielding 1.1% which increases to 1.2% on next year’s forecast.

On the 8th October the group announced the acquisition of Caledonian Holdings for a cash consideration of £4.4M. The business supplies equine vet practices in New Zealand and Australia. Their range of equine drugs will enhance the existing portfolio and will enable the group to grow market penetration in Asia.

On the 19th October the group released a trading update covering Q1 which was in line with management expectations with year on year above market growth in both Europe and North America. The board is confident of achieving their expectations for the current year and in the continued out-performance of the markets in which it operates.

Also on the 19th October the group announced the acquisition of Laboratorios Vencofarma do Brasil for a total consideration of £37.8M. The business has a large portfolio of vaccines and other food producing animal products which it sells predominantly within Brazil. It also has a small range of companion animal products. The group will invest significantly over the next three years to develop the business and its presence in South America.

Overall then this has been a decent year for the group. Profits were up due to the US deferred tax credit, otherwise they were broadly flat, not helped by the large increase in amortisation following the acquisitions. Net assets increased but net operating cash flow declined due to working capital movements. Europe seems to be performing OK, driven by companion animal products and North America also seems to be doing fairly well as strength in the US and Canada offset slower conditions in Mexico, although the work done on improving Bovel should help there.

The group is looking to expand internationally which is a good thing but it is mostly through acquisitions. I would prefer a more measured approach personally but I suppose this is personal preference. The trend of distributors marketing their own products is a concern and I’m sure this is something we will likely hear more of. This is a good company and I have owned shares in them for nearly ten years. They are now very expensive, however, with a forward PE of 26.8 and yield of 1.2% so I sadly think it might be finally time to take profits.

On the 19th December the group announced that director Tony Griffin sold 5,000 shares at a value of £106K. He now owns 70,606 shares in the company.

On the 14th January the group released a trading update covering the first half of the year which was in line with management expectations. Reported group net revenue increased by 18% with the same increase in the European net revenues, including the acquisitions RX Vet, AST Farma, Caledonian Holdings and Venco. Like for like European net revenues increased by 4%. The North American segment reported net revenue growth of 18% which was driven by the expansion of the US direct sales force which is continuing to generate significant sales growth and was further helped by the temporary absence from the market of a competitor product to Zycortal.