Swallowfield have now released their final results for the year ended 2018.

Revenues declined somewhat year on year as a £6.6M growth in UK revenue was offset by a £6.1M decline in EU revenue and an £800K fall in ROW revenue. Cost of sales also declined somewhat with a £77K fall in R&D costs to give a gross profit £218K lower. Amortisation increased by £343K but there was a £113K positive swing to a forex gain and other commercial and admin costs declined by £1.7M. There were no acquisition costs, which accounted for £343K last year but there was a Sterling share club write-off, which cost £279K to give an operating profit £1.4M higher. There was an increase in dividend income from the 19% shareholding in Shanghai Colour Cosmetics Technology but tax charges grew by £348K to give a profit for the year of £3.5M, a growth of £988K year on year.

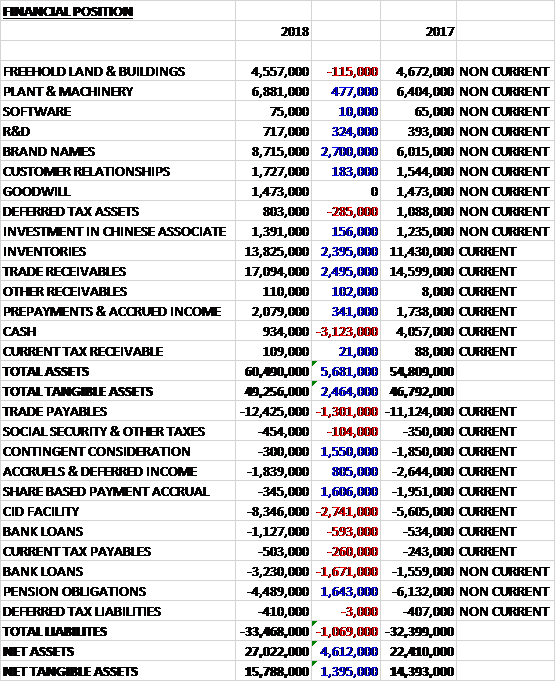

When compared to the end point of last year, total assets increased by £5.7M driven by a £2.7M increase in brand names, a £2.5M growth in trade receivables and a £2.4M increase in inventories, partially offset by a £3.1M fall in cash. Total liabilities also increased during the year as a £1.6M decline in contingent consideration, a £1.6M fall in share based payment accruals and a £1.6M decrease in pension obligations was more than offset by a £2.7M increase in the CID facility, a £2.3M growth in bank loans and a £1.3M increase in trade payables. The end result was a net tangible asset level of £15.8M, a growth of £1.4M year on year.

Before movements in working capital cash profits declined by £1.7M to £4.9M. There was a cash outflow from working capital reflecting the timing of the three big contracts in the manufacturing business, but tax charges fell by £380K to give a net cash outflow from operations of £281K, a £4.1M detrimental movement year on year. The group spent £1.6M on fixed assets, £3.9M on intangible assets and £1.9M on acquisitions which meant there was a cash outflow of £7.4M before financing. They took out £5M of new borrowings and paid out £963K in dividends which meant that there was a cash outflow of £3.1M and a cash level of £934K at the year-end.

The profit for the brands business was £4.8M, a growth of £1.9M year on year. All major brands are showing year on year growth and the Fish acquisition has been integrated into the portfolio during H2.

The group are focusing on developing sales in new international markets. Bi-lingual pack formats have been developed for specific brands. The launch of Dirty Works into France and Belgium has been followed by new distribution in the Middle East. The range of bath solutions, Dr Salts, has launched successfully in South Africa and the Real Shaving Company has launched in New Zealand.

The profit for the manufacturing business was £2.6M, a decline of £2.2M compared to last year. Despite a satisfactory H1 performance the business was adversely affected by material cost inflation and this, combined with delays in the production of three major new contracts, resulted in the lower profit. Actions have been taken to mitigate the inflationary headwinds and the new contracts will contribute to business results in 2019.

The group have won significant volumes within the aerosol category with two brand owners. They have also developed a new lip care line for a major global brand. All three of these contracts went into full production as they entered the new financial year.

The group have completed a major refurbishment of their R&D lab in Wellington. They have also invested in both new robotics to drive line efficiency and improved packing automation for hot pour products at their Tabor site in the Czech Republic. At the UK sites they have made specific investment to improve capacity and flexibility to support new customer requirements.

In February the group acquired the Fish brand, a range of male haircare and styling products.

During the year there was an exceptional cost of £279K which is the costs of writing off the investment in Sterling Shave Club and having certain posts duplicated to ensure a smooth transition in key management roles.

After five years in the role, CEO Chris How has decided to retire. The group have appointed Tim Perman as CEO who joins from PZ Cussons where he was group category and brand director and global beauty director.

The board expect the strong momentum from the owned brands business to continue, supported by a stream of new products and continued support from retail customers. The manufacturing business is expected to remain challenging due to prevailing market conditions and ongoing cost inflation. Significant actions are being taken to mitigate these challenges and they expect the profitability of this segment of the business to improve in H2 2019. In line with the rest of the industry, however, the group continues to be challenged by low consumer confidence, global inflationary pressures and the uncertainty of Brexit.

At the current share price the shares are trading on a PE ratio of 12.8 which falls to 9.7 on next year’s consensus forecast. At the year-end the group had a net debt position of £11.8M compared to £3.6M at the end of last year. After a 19% increase in the dividend the shares are yielding 2.4% which increases to 2.7% on next year’s forecast.

Overall then this has been a bit of a mixed year for the group. Profits increased due to lower admin costs and net assets improved. The operating cash flow deteriorated though, even before the large outflow of cash through working capital, and there was a cash outflow at the net operating level. The brands business seems to be doing well but the manufacturing business has struggled with higher costs and the timing of large contracts. The latter issue will reverse in the coming year.

This is a tricky one. I would like to see some real growth and cash generation but it does sound as though the coming year will be an improvement. With a forward PE of 9.7 and yield of 2.7% I’m tempted to get back in here. Maybe I need an intervention!

On the 15th November the group released a trading update covering the first four months of the year which were in line with expectations. They continued to see strong momentum in their brands business which is benefiting from another year of sales growth in Christmas gifting ranges.

The manufacturing business remains challenging with a general softening in demand due to the current retail environment and low consumer confidence. Price increases and cost base optimisation are being implemented and expected to have a positive impact in H2 and volumes generated by three previously announced contract wins are also making a positive contribution.

While the board are conscious of the continuing macro uncertainty overall they expect to maintain their progress and are well positioned to deliver against their expectations for the full year.