Cranswick have now released their interim results for the year ending 2019.

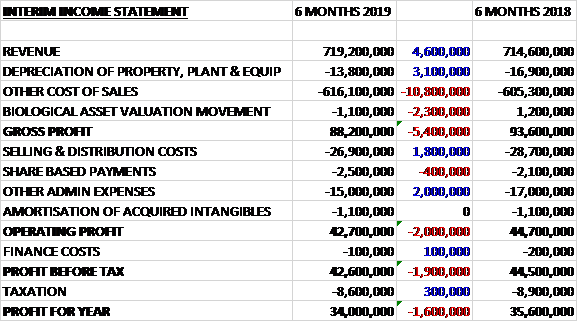

Revenue increased by £4.6M and depreciation was down £3.1M but other cost of sales increased by £10.8M and there was a £2.3M detrimental swing in the valuation of pigs which meant the gross profit declined by £5.4M. Selling and distribution costs declined by £1.8M and other admin expenses fell by £1.6M to give an operating profit £2M lower. Finance costs were down £100K and tax charges fell by £300K which meant that the profit for the period was £34M, a decline of £1.6M year on year.

When compared to the end point of last year, total assets increased by £27.8M driven by a £26.2M growth in property, plant and equipment, an £11.2M growth in inventories, a £1.8M increase in the value of pigs and a £2.2M increase in financial assets, partially offset by an £11.3M decline in cash. Total liabilities also increased during the period as a £2.5M decline in the current tax liability was more than offset by a £6.4M increase in financial liabilities. The end result was a net tangible asset level of £348.3M, a growth of £24.6M over the six month period.

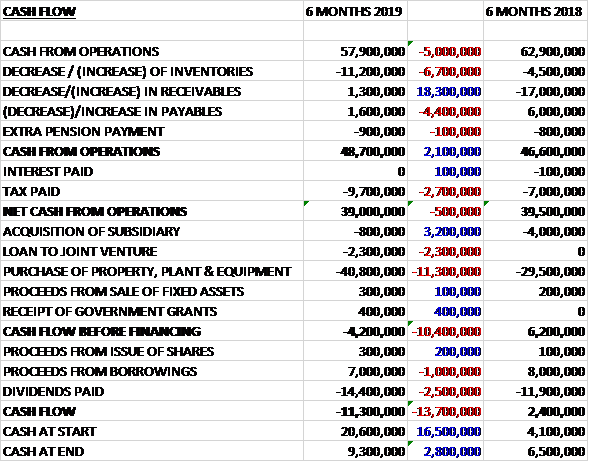

Before movements in working capital, cash profits declined by £5M. There was a cash outflow from working capital but this was less than last year. Tax payments increased by £2.7M, however, which meant that the net cash from operations was £39M, a decline of £500K year on year. The group spent £800K on acquisitions, loaned £2.3M to a joint venture and spent £40.8M on fixed assets to give a cash outflow of £4.2M before financing. They took out £7M of new borrowings but spent £14.4M on dividends to give a cash outflow of £11.3M and a cash level of £9.3M at the period-end.

Total fresh pork revenue fell by 5.5% reflecting lower wholesale and export demand with slightly fewer pigs processed. Retail sales increased by 4.7%, however, underpinned by strong volume growth as the World Cup and summer weather combined to deliver a strong BBQ season as well as good growth in added value convenience ranges. This growth was offset by lower sales of roasting joints and other more traditional products. Overall their retail sales growth was still comfortably ahead of the wider Fresh Port retail market performance.

The group invested £7M across the three pork primary processing facilities during the period, including spend on phase 1 of the extension to the Hull facility which is nearing completion and will further increase capacity and improve operational efficiencies.

Total export revenue reduced by 2.6% reflecting lower overall volumes. Export volumes to the key Far Eastern markets were 12.4% ahead of last year, however, driven by approval for direct export to China from the Ballymena site and for additional product lines from the Hull processing facility, secured in the second half of last year. Volume gains in these markets were offset by softer pricing.

The recent outbreak of African Swine Fever in China is disrupting local pork markets. The disease was also detected in the feral pig population in Belgium in September with the region having been quarantined. The group have implemented heightened biosecurity protocols. During the period they invested over £6M in their farming infrastructure to increase breeding and finishing capacity and a further £2M in a joint venture with one of their key commercial pig producers to increase capacity. The average UK pig price in the period was 8% lower but the price ended the period 1% higher than it started it, rising steadily through to the end of July before falling back.

Convenience revenue increased by 0.6% reflecting strong growth in continental products offset by lower cooked meats sales. Cooked meat sales were lower due to lower pricing and reduced promotional activity. The group continue to develop their Sous Vide and Slow Cook ranges and anticipate further penetration in this sector. A further £11M of capex was made across the three cooked meats facilities on cooking, cooling and slicing equipment to add capacity and improve efficiencies.

Continental products revenue grew strongly, with the new facility providing additional capacity for new olive business won in the period and increase sales of corned beef. Demand for summer eating ranges drove a 10% increase in the overall market for olives and continental meats, with the continental business outperforming the wider UK retail market. The new facility in Bury, which increases capacity by 70%, was commissioned in May with capex of £3M during the period to complete the £27M project. Although commissioning costs were higher than expected and expected efficiency improvements were no delivered immediately, the business is now making good progress towards achieving planned returns and revenue growth is ahead of expectations.

Gourmet products revenue increased by just 0.1% with moderate volume growth offset by lower prices. Strong sausage sales growth, which was well ahead of the market, was offset by lower sales of bacon and pastry products. Sausage sales growth reflected a strong promotional pipeline and the extended summer BBQ season. They secured additional business with their discount retail customers as they expand their premium ranges and they also secured a long term supply agreement with their largest food service customer.

Lower bacon volumes in the period reflected reduced levels of promotional activity from their retail customer as well as the delisting of another customer from April. As they move towards peak seasonal trading, promotional activity and sales volumes have increased with Christmas gammon sales expected to boost revenue. Pastry sales were lower reflecting a range review by the anchor customer but recent new listings with two of the business’ forecourt operators highlight the potential for this business to participate in the growing food to go market. A full Christmas order book and new product listings from the anchor customer from November will provide strong momentum for the pastry business through the second half of the year.

Poultry revenue increased by 19%. The ready to eat chicken category continues to grow ahead of the wider UK meat protein sector and fresh chicken continues to outperform with market volumes ahead by 6% and 3% respectively. Sales of premium cooked poultry grew strongly reflecting the full period benefit of business wins with two of the group’s principal retail customers in the prior year and the launch of new lateral sliced products with one of those customers during the period.

The fresh chicken business operated at full capacity during the period. It was affected during the warm summer by reduced bird growth and increased mortality. Also higher soft commodity prices increased feed costs and wholesale chicken prices were lower. The £60M investment in a new poultry processing facility in Suffolk is progressing to plan. Capex of £12M in the period included £11M on this project with the steelwork frame now under construction. The factory will be operational towards the end of next year and will be the most advanced and efficient facility in the UK. They have also committed to further substantial investment in their upstream agricultural operations to ensure they have a sustainable supply chain to serve the new facility.

There was a high level of capex in the period and future capex under contract at the period-end was a sizeable £35.4M compared to £11.2M at the same point of last year. The new £27M Continental Products facility in Bury was commissioned during the period. They have also invested heavily in their agricultural operations and construction of a £60M primary poultry processing facility in Suffolk due for completion towards the end of next year is now underway.

During the period the group exercised its call option to acquire the remaining 10% of Cranswick Gourmet Pastry Company for £800K reducing the contingent consideration balance to zero.

Going forward there will be challenges to be overcome, not least the uncertainty created by the ongoing Brexit discussions. There are a number of areas in which Brexit could affect the business including access to and the cost of labour, the potential for import tariffs on EU pork and continental food products and the valuation of Sterling against other currencies.

At the current share price the shares are trading on a PE ratio of 20.4 which falls to 18.7 on the full year consensus forecast. After a 5.3% increase in the interim dividend the shares are yielding 1.9% which increases to 2% for the full year. At the period-end the group had a net cash position of £2.2M compared to £20.6M at the year-end.

Overall then the group has struggled somewhat over the period. Profits declined due to increased cost of sales and the operating cash flow deteriorated with no free cash being generated. Both convenience and gourmet segments were flat during the period and while poultry saw revenues increase, fresh pork saw a decline due to lower wholesale and export demand. The group is currently undergoing heavy capex so doesn’t have much free cash, which is great but has its own risks and Brexit has the potential to throw a spanner in the works. This is still a quality company but I feel momentum has been lost somewhat and with a forward PE of 18.7 and yield of 2%, this doesn’t seem to be reflected in the share price and I am considering selling.

On the 7th February the group released a trading update covering Q3. As expected, revenue was 2% lower compared to last year. Strong growth in poultry and continental products was offset by lower sales from other pork related categories. The UK pig price continued to ease, ending the quarter 7% down on last year with this downward trend being reflected in selling prices. Performance over Christmas was robust.

Construction of the new poultry processing facility in Suffolk is continuing to plan with the exterior building works nearing completion and commissioning anticipated towards the end of the next financial year as previously indicated. They have agreed a long term supply contract with Morrison Supermarkets to supply fresh poultry from this new facility. They will shortly start supplying the same customer with a range of cooked poultry products from their added value poultry facility in Hull.

Net debt increased during the quarter, reflecting the seasonal increase in working capital and ongoing capex projects, but ended the period in line with the same stage last year.

Going forward, the board’s expectations for the performance this year is unchanged. For the following year, the operating margin is likely to decline, reflecting the potentially challenging commercial landscape, together with start-up and commissioning costs associated with the new Suffolk facility, only partly offset by management actions.

Notwithstanding these challenges, the new facility and existing added value poultry facilities and broadening customer base, provide a solid platform to further develop their poultry business and drive future growth in this expanding category.

On the 12th February it was announced that non-executive director Tim Smith had purchased 1,500 shares at a value of £39K.