Avingtrans has now released their final results for the year ended 2018.

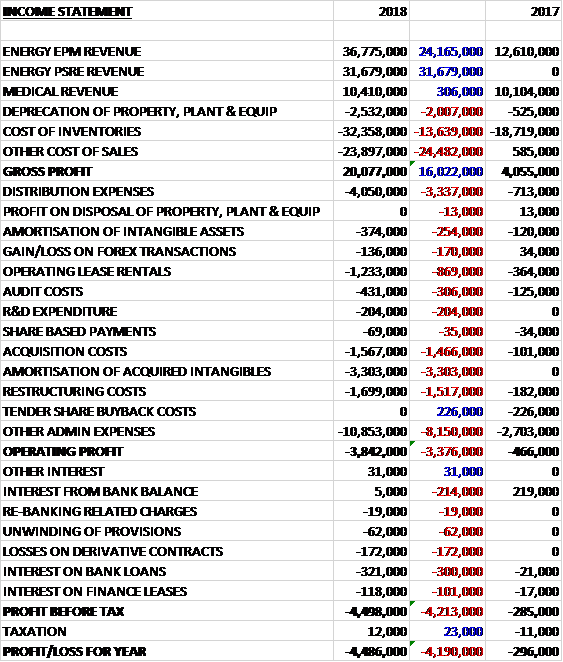

Revenues increased when compared to last year due to a maiden £31.7M of Energy PSRE revenue a £24.2M increase in Energy EPM revenue and a £306K growth in Medical revenue. Depreciation was up £2M, cost of inventories increased by £13.6M and other cost of sales grew by £24.5M to give a gross profit £16M higher. Distribution expenses increased by £3.3M, operating lease rentals were up £869K and other underlying admin expenses grew by £8.2M. We also see a £3.3M amortisation of acquired intangibles, a £1.5M growth in restructuring costs and a £1.5M increase in acquisition costs to give an operating loss £3.4M greater than last time. There was a £214K decrease in loan interest income couple with a £300K increase in loan interest charges along with some other increased finance costs which meant that the loss for the year was £4.5M, a £4.2M deterioration year on year.

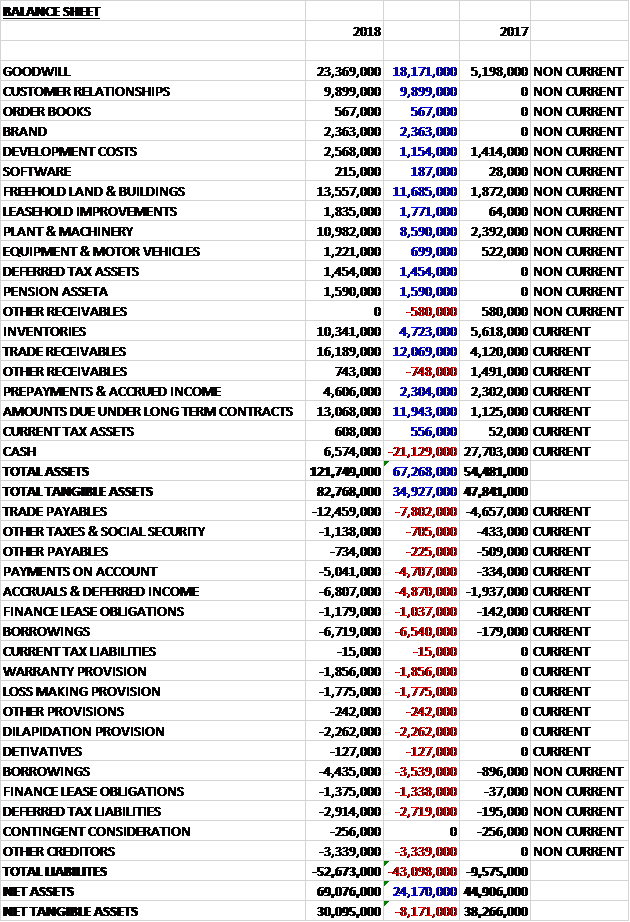

When Compared to the end point of last year, total assets increased by £67.3M driven by an £18.2M growth in goodwill, a £12.1M increase in trade receivables, an £11.9M increase in amounts due under long term contracts, an £11.7M increase in freehold land and buildings, and a £9.9M increase in customer relationships. Total liabilities also increased due to a £7.8M growth in trade payables, a £10.1M increase in borrowings, a £4.9M increase in accruals and deferred income and a £4.7M growth in payments on account. The end result was a net tangible asset level of £30.1M, a decline of £8.2M year on year.

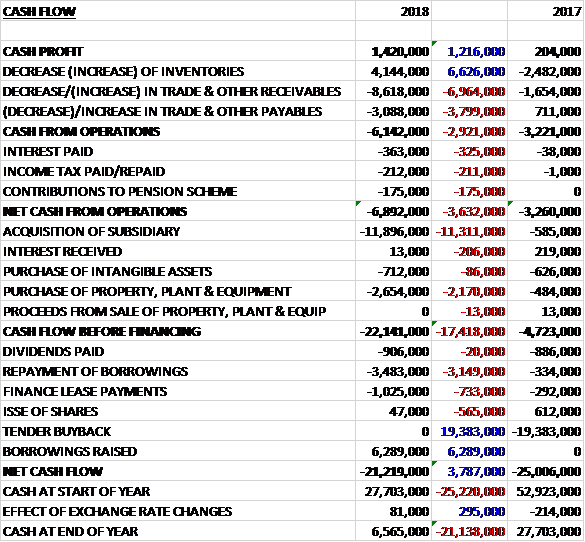

Before movements in working capital, cash profits increased by £1.2M to £1.4M. There was a cash outflow from working capital and a £325K increase in interest, a £211K increase in tax payments and a £175K growth in pension scheme contributions to give a net cash outflow from operations of £6.9M, a deterioration of £3.6M year on year. The group spent £11.9M on acquisitions, £2.7M on fixed assets and £712K on intangible assets to give a cash outflow of £22.1M before financing. They raised a net £2.8M of new borrowings, paid out £906K in dividends and paid £1M on finance leases which gave a cash outflow of £21.2M for the year and a cash level of £6.6M at the year-end.

The operating loss in the Energy EPM division was £1.5M which represents the first time the business has been part of the group. The division bolstered its capacity in India with a new motor rewind centre and has now opened a new facility in China. Both of these will help secure end user business in the region and act as operational hubs for the sale of original equipment, engineering and tendering.

In the UK the business has recently signed an authorised channel and service partner agreement with Baker Hughes, a GE company, which has significant installed base in the country but no effective local facility to service, overhaul and upgrade their equipment. This partnership is thought of as a template for other such opportunities elsewhere.

The business has gained its first order from a Gen IV nuclear developer in the US for a future molten salt technology and also funding from the US Department of Energy to develop molten salt pump technology for advanced concentrated solar applications. With its new range of pumps and seal-less circulating pumps for natural gas and a range of renewable tech, the business is slowly reducing its reliance on coal fired power stations.

The operating profit in the Energy PSRE division was £425K, flat year on year. The Hayward Tyler fluid handling business in Scotland was moved into this division to support the nuclear decommissioning and reprocessing market in the UK which remains a key focus for the group. The group also has a keen interest in both the UK nuclear submarine fleet and associated facilities as well as developing new nuclear tech such as small modular reactors. This division has a good installed base on the UK sub fleet, is the chosen manufacturing partner for the Astute steam turbines and experience to support longer term nuclear tech.

Away from nuclear, the divisional brands also have a strong presence in the oil and gas market. This market remains challenging but activity is increasing and with the global demand for LNG still expected to grow significantly, the group is confident about future opportunities.

The division has seen an increase in the ratio of end user to OEM sales. In particular Peter Brotherhood saw increased aftermarket sales across its installed base, including on one occasion an entire replacement steam turbine. End user service arrangements have been signed to gain better access to the reciprocating compressor installed base and a refresh of the channel partners and agents has been concluded to allow complete focus on this aspect of the business. It has a well developed end user value proposition and with improved agility and customer relevance, is confident of further growth.

The Crown business remains a small but solid performer in the division with new applications becoming apparent for its smart pole solutions. The first of these was a previously won contract for Fluor, for flame-detector masts which are being deployed in a large scale petrochemical plant improve overall site safety.

The operating loss in the Medical division was £109K, a deterioration of £537K when compared to last year despite modest revenue growth. As the new equipment business develops into growing niche markets, the addition of Scientific Magnetics and the MR Resources pan-European partnership will underpin significant investment in this division.

Strategic progress at Scientific Magnetics is promising but the expected resulting orders have been slower to materialise than originally thought and this business made a loss for the year. They have continued to invest for the longer term, however, and in early 2018 they launched a Europe-wide NMR service and support offering with their US partner, MR Resources. This development will only start to bear fruit in the current year but this new service offering means that all three divisions have access to a solid aftermarket revenue stream.

Metalcraft’s UK business with Siemens for MRI components continues to be steady, but progress in China with other vacuum vessel customers such as Alltech was somewhat slower ramping up and was behind plan overall for the year. Composite Products had a solid year with deliveries to Rapiscan improving steadily and showing promise for next year. Other smaller accounts also supported revenues at this unit and a return to profit.

In the upstream oil and gas market exploration is now increasing 6% year on year which although still only half what it was at the beginning of the decade, marks a massive change over recent years. Operating expenditure is now being released to secure current operations, resulting in capex beginning to be slowly released for major new projects. The group is witnessing the front end of this activity through increased bidding and is optimistic regarding future projects. The ongoing investments in technologies such as the subsea boosting tech are now poised to move through the development phase to full deployment as the market reopens.

In the midstream market, although the market predictions for LNG and FRSU vessels remains bullish, in reality the supply chains remains stagnant. The group maintains a close eye on developments and supports projects at the appropriate level from early engineering studies. Timing remains challenging, but the group is confident of securing some projects.

Within the medical markets, the group are investigating a number of niche MRI applications such as veterinary imaging and their associated routes to market with the intention of pinpointing the most promising of these for future investment. Within NMR, their previous attempts to align with the market leader Bruker were unfruitful so they are now looking to align with new market entrant Q One Instruments of China and also with MR Resources of the US. Whilst early days for this initiative they are already winning support contracts for end users and the prospect list for Q One Instruments is promising.

The customer on time in full deliveries score declined from 99.7% last year to 84.2% this year due to lower performance in Hayward Tyler which was struggling with deliveries as a result of cash flow issues and a resulting creditor overhang. These statistics have been gradually improving since the acquisition.

In September 2017 the group acquired Hayward Tyler for a total consideration of £42M, generating goodwill of £18.2M. Since acquisition the business has made a loss of £3.5M. The business’ higher cost debt of £11.5M was repaid at acquisition and a further £10.7M absorbed with HTG costs of £3.7M also being incurred and paid. During the period £3M was removed from the creditor overhang with further right sizing restructuring costs of £1.7M and acquisition costs of £1.6M being paid alongside a further working capital investment of £4.4M

In February the group acquired Ormandy for a cash consideration of £135K, generating goodwill of £50K. Since the acquisition date the business has generated a loss of £16K. The business is now part of the PSRE division and manufactures off-site plant, heat exchangers and other heating, ventilation and air con products. Following the acquisition, the business has been trading out a few remaining loss making contracts and rebuilding its business to be in a profitable position but this has required a cash investment for working capital and initial underutilisation which has since improved.

Going forward the energy divisions has a strong emphasis on both the nuclear and off shore oil and gas markets, both of which are showing signs of regeneration. The medical division continues to focus on high integrity components and systems for medical, industrial and scientific equipment manufacturers. The board are not unduly concerned by Brexit since their direct EU exposure is rather limited and they have taken some initial evasive action in their supply chains. Similarly US government tariff change risks have been largely mitigated by an agile supply chain response but they will continue to monitor this situation closely.

The group is loss making which makes PE ratios a rather moot point but on next year’s forecast the shares are trading on a PE ratio of 20.3. At the year-end the group had a net debt position of £7.1M compared to a net cash position of £26.4M at the end of last year. At the current share price the shares are yielding 1.7% which increases to 1.8% on next year’s forecast.

On the 23rd October the group announced the acquisition of Tecmag of Texas for a total consideration of $243K. The business designs, manufactures, installs and tests instrumentation including full consoles, system upgrades and solid state probes, mainly for MRI and NMR systems. Last year the business had a pre-tax profit of $16K.

Overall then this has been a year of transition for the group, dominated by the acquisition of Hayward Tyler. The loss widened, net tangible assets declined and operating cash outflow worsened but the latter was due to working capital movements and cash profits improved. The only division to make a profit was the Energy PSRE division but profits were flat. This business is reliant on the oil and gas market. The medical division saw losses worsened as orders were slower to come by and the Energy EPM division made a loss on its first contribution. Obviously teething problems would be expected with such a transformational acquisition so I am sure things will improve but the forward PE of 20.3 and yield of 1.8% looks a bit expensive to me.

On the 14th January the group released a trading update covering the first half of the year where they stated that trading had been in line with expectations. The former HT businesses are continuing to improve and are now fully integrated. Peter Brotherhood’s large government contract is proceeding to plan and their progress has resulted in further enquiries from the customer. Metalcraft’s 3M3 box contract is now in production with an expectation that they will achieve full current production capacity by the year-end.

Recent acquisitions are also integrating well. The performance of Ormandy is steadily improving and the outlook for the business is strong. Integration is also underway at Tecmag.