Tristel has now released their final results for the year ended 2018.

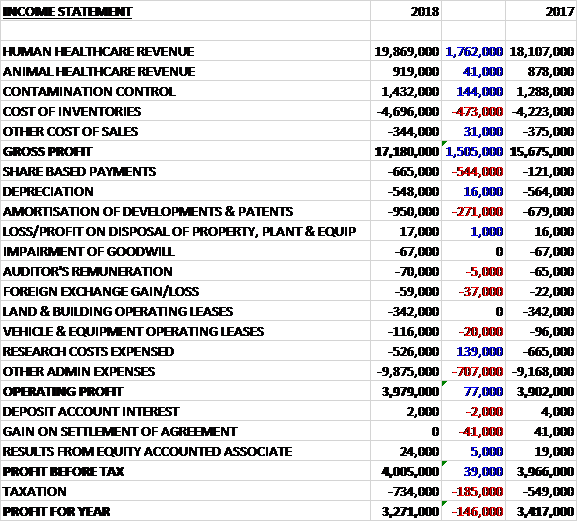

Revenues increased when compared to last year with a £1.8M growth in human healthcare revenue, a £144K increase in contamination control revenue and a £41K growth in animal healthcare revenue. Cost of inventories were up £473K but other cost of sales reduced slightly to give a gross profit £1.5M higher. Share based payments were up £544K, amortisation charges increased by £271K but research costs were down £139K before a £707K growth in other admin expenses meant that the operating profit was £77K higher. There was no gain on the settlement of an agreement, which brought in £41K last time and tax charges increased by £185K mainly relating by movements in deferred tax, which meant that the profit for the year was £3.3M, a decline of £146K year on year.

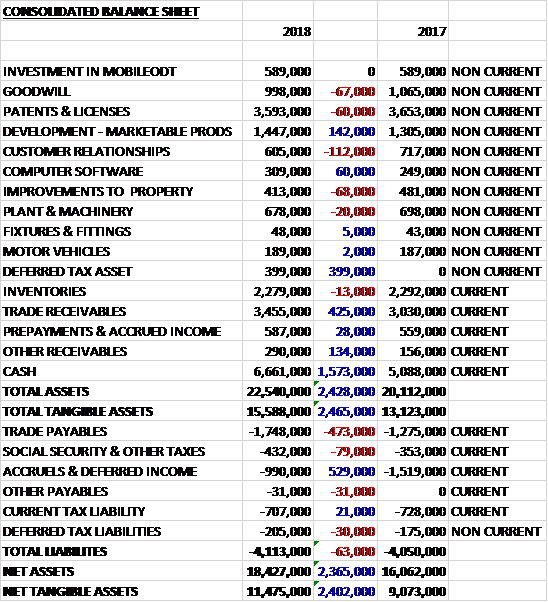

When compared to the end point of last year, total assets increased by £2.4M driven by a £1.6M growth in cash, a £425K increase in trade receivables, a £399K growth in deferred tax assets and a £142K increase in development costs. Total liabilities also increased slightly as a £529K decline in accruals and deferred income was offset by a £473K increase in trade payables and smaller increases in other liabilities. The end result was a net tangible asset level of £11.5M, a growth of £2.4M year on year.

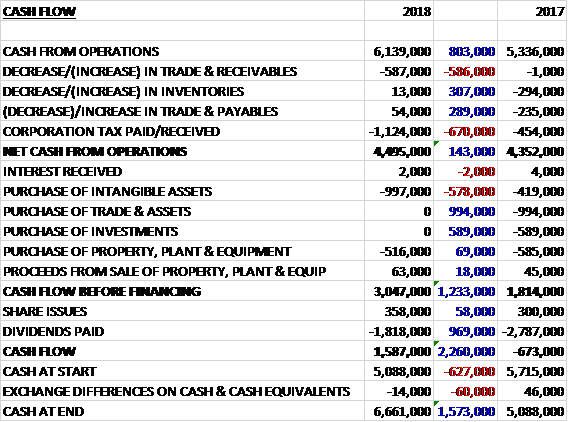

Before movements in working capital, cash profits increased by £803K to £6.1M. There was a cash outflow from working capital but this was broadly similar to last year. Tax payments increased by £670K to give a net cash from operations of £4.5M, a growth of £143K year on year. The group spent £997K on intangible assets and a net £453K on property, plant and equipment to give a free cash flow of £3M. Of this £1.8M was spent on dividends which gave a cash flow of £1.6M and a cash level of £6.7M at the year-end.

Overseas sales were ahead by 19% but UK sales only advanced by 2% due to the high market penetration in the UK. Gross margin remained static at 77%. They have seen an increase in the cost of componentry as a result of the scarcity of certain chemicals and an increase in the cost of cardboard and plastics. Offsetting this they acquired the Hong Kong distributor, gaining their gross profit.

The gross profit in the Human Healthcare division was £15.7M, a growth of £1.5M year on year. UK sales remained unchanged but direct sales to the EU were up 26% and to ROW countries increased by 11%. Sales to EU distributors were up 15% and sales to ROW distributors increased by 32%.

The gross profit in the Animal Healthcare division was £550K, a decline of £105K when compared to last year. Direct sales to UK customers declined by 16%. Direct sales to the EU fell by 40% (although this was just £2K). Direct sales to ROW customers were up 8%. Sales to UK distributors were up 9% but sales to EU distributors declined by 1%.

The gross profit in the Contamination Control division was £922K, an increase of £128K when compared to 2017. UK sales were up 11%. Direct sales to the EU increased by 89% and direct sales to ROW countries were up 444%, albeit from a low base. Conversely, sales to EU distributors were down 36% and there were no sales to ROW distributors (£1K last year).

The group have invested £981K in regulatory and product enhancement programmes with £500K of that relating to the US (the same as last year). Although no revenues have been earned in the US to date, progress has been made to build a commercial platform from which to enter the market. During the year they received their first regulatory approval from the EPA for their foam-based Duo product and will start manufacture and marketing on a limited scale during the year ending 2019.

Since the year-end they have made a second submission to the EPA to extend Duo’s product claims as an intermediate level disinfectant and they are well advanced in generating the data for their first submission for a 510 approval from the FDA. This is also for Duo and will position the product as a high level disinfectant. They have a partnership with Parker labs which means they have put in place manufacturing capability and a national distribution network. They have granted Parker marketing rights for Duo’s use in ultrasound where they are the market leader in the US for ultrasound conductive gels, the contract is royalty-based.

A further investment of £120K was made in MobileODT, the Israeli diagnostic tool business that the group has a 3% stake in. They have expanded their commercial collaboration with the business to include a version of their Duo product labelled for use with their mobile colposcope. After the year-end, the group have also become MODT’s distributor for EVA in the UK, Australia and New Zealand.

The group have advised their continental customers to increase their stockholdings over the coming months in preparation for possible disruption to the supply chain. Based on available advice they believe that they will be able to CE mark their disinfectants and sell them in Europe irrespective of the outcome of the Brexit negotiation. The only certainty is that they will experience turbulence this year and their normally predictable pattern of trade will be disrupted to some extent. Notwithstanding this near-term uncertainty the outlook for the group remains positive.

At the current share price the shares are trading on a PE ratio of 34.8, falling to 25 on next year’s forecast. After a 13.6% increase in the dividend, the shares are yielding 1.8% which increases to 2.1% on next year’s forecast. At the year-end the group had a net cash position of £6.7M.

On the 19th November the group announced the acquisition of European distributors Ecomed in Belgium, France and the Netherlands. The business is the group’s exclusive distributors and Benelux and France and is both cash generative and profitable. Of their €3.1M of sales, €2.5M were Tristel products and in the first half of this year they generated an EBITDA of €570K. The board expect the acquisition to contribute earnings of at least £250K this year and in subsequent years to be materially earnings enhancing. The office and logistics hub in Antwerp will be beneficial post-Brexit.

A consideration of €5M is to be paid upon completion, of which €3.4M is payable in cash and €1.6M from the issue of 573,860 new shares. Additional deferred consideration of up to €1.8M may be paid before July 2019 based on audited EBITDA in 2018 exceeding €840K and sales growth of 15% being achieved in 2019. France in particular is an underdeveloped market for the group with sales there only a fraction of those in Germany.

On the 11th December the group released a trading update. They expect pre-tax profit (excl. share based payments) for the first half to be no less than £2.2M compared to £2M last year. This figure takes account of the transaction costs arising from the Ecomed acquisition with the period only including one month’s full profit contribution from them. The integration of these new businesses is progressing well. Overall the group is performing in line with management expectations and the US regulatory approvals project is progressing as planned.

Overall then this has been a decent year for the group. Profits did decline but this was due to a higher deferred tax charge and pre-tax profits saw a modest rise despite rising costs. Net assets improved and the operating cash flow increased with a decent amount of free cash being generated. The US applications seem to be progressing well but there is real uncertainty on the horizon in the form of Brexit. The first half of the coming year has started well but the shares are highly priced with a forward PE of 25 and yield of 2.1%. Tricky one this but I still think the shares are on the expensive side.