Paypoint has now released their interim results for the year ending 2019.

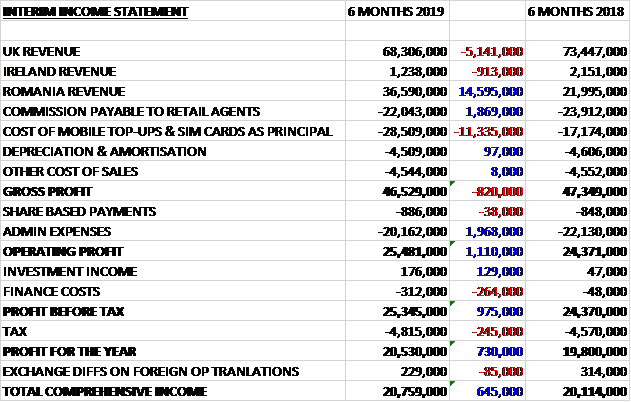

Revenues increased when compared to the first half of last year as a £5.1M decline in UK revenue and a £913K fall in Irish revenue was more than offset by a £14.6M growth in Romanian revenue. Commission payable to retail agents decreased by £1.9M but the cost of mobile top-ups and sim cards as principal increased by £11.3M which meant that the gross profit was down £1.1M. Admin expenses fell by £2M, however, to give an operating profit £1.1M above that of last time. Investment income was up £129K but finance costs increased by £264K and tax charges grew by £245K to give a profit for the period of £20.5M, a growth of £730K year on year.

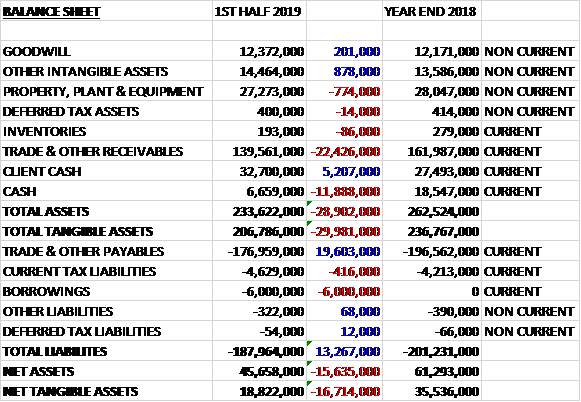

When compared to the end point of last year, total assets declined by £28.9M, driven by a £22.4M decline in receivables and an £11.9M decrease in cash, partially offset by a £5.2M increase in client cash. Total liabilities also declined as a £6M increase in borrowings was more than offset by a £19.6M fall in payables. The end result was a net tangible asset level of £18.8M, a decline of £16.7M over the past six months.

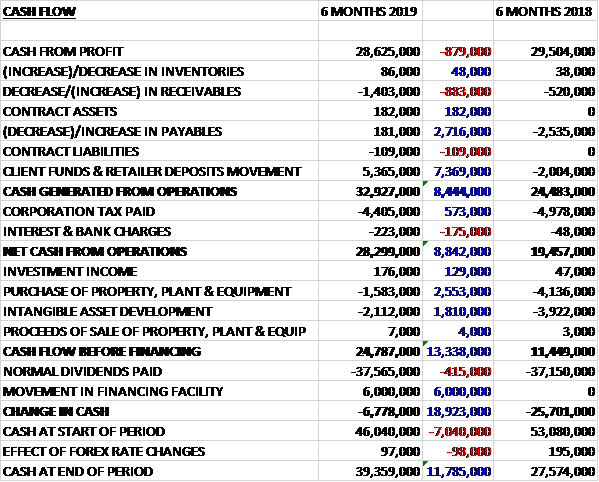

Before movements in working capital, cash profits declined by £879K. There was a cash inflow from working capital and tax payments fell by £4.4M to give a net cash from operations of £28.3M, a growth of £8.8M year on year. The group spent £2.1M on intangible asset development and £1.6M on property, plant and equipment (capex is expected to increase in the second half to around £8.8M) to give a free cash flow of £24.8M. This did not cover the £37.6M paid out in dividends so the group took out £6M of financing to give a cash outflow of £6.8M and a cash level of £39.4M at the period-end.

Overall net revenue was down 1.6% due to the £2.2M impact of the closure of the Department of Work and Pensions’ SPS and the £500K impact from the revised Yodel commercial terms. Underlying net revenue growth was 3.2% as a £400K increase in UK retail services and a £1.7M growth in Romania was partially offset by a £300K reduction in UK bill payments and top-ups.

The net revenue in the Bill and General division was £25.4M, a decline of £1.3M year on year. Net revenue in the UK fell by £2.3M, largely due to the closure of SPS worth £2.2M, whereas Romanian net revenue increased by £1M as a result of the Payzone acquisition and continued organic growth including adding ten new clients which increased market share in the country from 24% to 38%. The Multipay service continued to perform well and increased transactions by 56%.

The net revenue in the top-ups and e-money division was £10.7M, a growth of £400K when compared to the first half of last year. UK net revenues declined by £200K as a result of the expected ongoing decline in UK mobile top up volumes, offset partially by good growth of 10% in UK e-money transactions. Romanian revenues were up £600K driven by a growth in transactions following the acquisition.

Net revenue in retail services overall was flat. In the UK, ATM revenues declined by £100K despite an increase in the number of transactions. Services fees increased by £1.4M driven by the rollout of the PayPoint One terminal, partially offset by lower SIM activation revenue. Card payments rebate revenue was flat but parcels net revenue reduced by £1.4M, partially reflecting the £500K impact of the revised terms with Yodel along with a 16% decline in parcel volumes through Yodel. Net revenue in Romania increased by £100K.

Going forward, a good performance in the first half underpins the board’s confidence that there will be progression in pre-tax profit in the full year. The New carrier partnership with Ebay is now live in 2,500 sites ahead of the festive season and the group remain focused on delivering at least two additional carriers in 2019. E-money and MultiPay volumes grew strongly and a further six clients were secured including Monzo.

At the current share price the shares are trading on a PE ratio of 12.7 which falls to 12.6 on the full year forecast. After an increase in the dividend the shares are yielding 10.4%. I can’t find a forecast for the dividends so if we assume the normal dividends are kept the same the forward yield is 5.8%.

Overall then this has been a bit of a subdued period for the group. Profits did increase, but this was due to a one-off VAT refund. Net assets deteriorated and although the operating cash flow improved, this was due to working capital movements and cash profits declined. A decent amount of free cash was generated but dividends weren’t covered entirely. The reduction in net revenue seems to be due to the SPS closure and revised Yodel terms. Excluding these items, there was growth, mainly due to the acquisition in Romania.

I think there is potential for the parcels business to take off at some point but this company does not seem to be growing at the moment. The forward PE of 12.6 and yield of 5.8% is not that taxing, however.

On The 24th January the group released a trading update for the quarter ending December 2018. Underlying net revenue increased by 1.4% to £30.9M. Including the impact of £1.3M from the closure of the Simple Payment Service and the renegotiated Yodel parcel fees, net revenue declined by 2.8%.

UK retail services net revenue increased by £400K to £9.7M driven by good growth in service fee revenue which increased by 31% to £2.6M. There was an increase of 1,455 PayPoint One terminal sites over the quarter. Given the strong momentum over the quarter, the year-end target of 12,400 sites has been increased to 12,700. The sales effort in the quarter continued to focus on extending penetration of the Base version of the EPoS solution charged at £10 a week to replace the legacy T2 devices and as a result, the average weekly service fee per site reduced from £15.01 to £14.89.

Card payment transactions grew by 23% to 28.8 million, driving a £200K increase in net revenue. ATM performance was strong despite the difficult market conditions with transactions increasing by 3.1% to 10.6 million. ATM net revenue declined by £200K primarily due to the reduced Link interchange fee which became effective in July.

Strong momentum continued in the Parcels business. The group delivered a first Christmas with new partner Ebay, with over 2,500 sites processing Ebay parcels and volumes are expected to grow as awareness of the service increases. A third party has now been added to the Collect+ network and is expected to go live before the end of the year. As anticipated, Yodel volumes continued to decline albeit at a lower rate, resulting in overall parcel volumes reducing by 3.2% to 6.8 million in the quarter.

Bill payment underlying net revenue was flat at £13.2M despite a 1.5% decline in transactions. The group has continued to execute its strategy to diversify its client portfolio to smaller higher margin customers. In the quarter, they added five new clients. Multi Pay drove a strong performance in energy transactions as businesses increasingly adopts their omni-channel platform, where transactions increased by 44% to 8 million.

Overall top-up and e-money transactions declined by 15% to 11.1 million. As expected this was driven by the continued declined in the prepaid mobile sector. E-money transactions, however, continued to grow strongly with transactions increasing by 13%. Top-up and e-money net revenue declined by nearly 3% with the reduction in volumes offset by increased average top-up values and the growth of e-money transactions which have a higher net revenue per transaction.

In Romania, net revenue increased by £200K to £3.7M. The migration of the Payzone network is making good progress, increasing operational efficiency and profitability. Romanian sites reduced from 18,984 to 18,317 in line with rationalisation plans to remove unprofitable sites. Transaction volumes declined by 2% primarily due to telecom operators switching customers to post-paid bills and new EU legislation reducing roaming charges.

At the period-end the group had a net cash position of £52.1M including £42.3M of client cash and retailer deposits. Seems like much of the same to me and the board’s expectations for the full year remain in line with the previous outlook.