QinetiQ has now released their interim results for the year ending 2019.

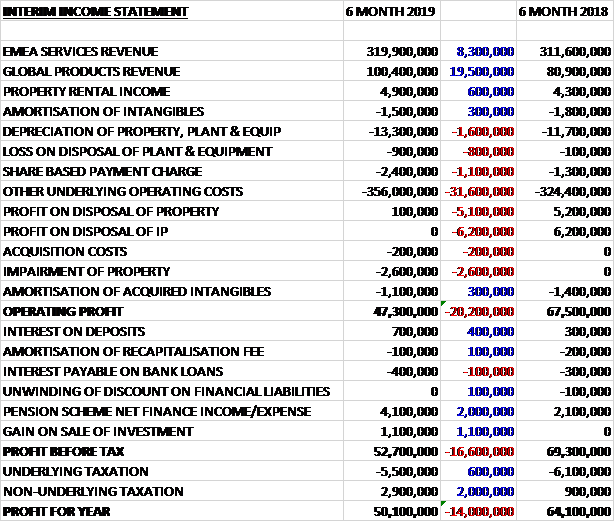

Revenues increased when compared to the first half of last year due to a £19.5M growth in global products revenue, an £8.3M increase in EMEA Services revenue and a £600K growth in property rental income. Depreciation was up £1.6M, share based payments increased by £1.1M and other underlying operating costs grew by £31.6M. We also see a £5.1M reduction in the profit on property disposals, a £6.2M fall in the profit of IP sales and a £2.6M property impairment which meant that the operating profit declined by £20.2M. Pension scheme income increased by £2M, there was a £1.1M gain on the sale of an investment and tax charges reduced by £2.6M due to a £2M increase in tax income related to share based payments, to give a profit for the period of £50.1M, a decline of £14M year on year.

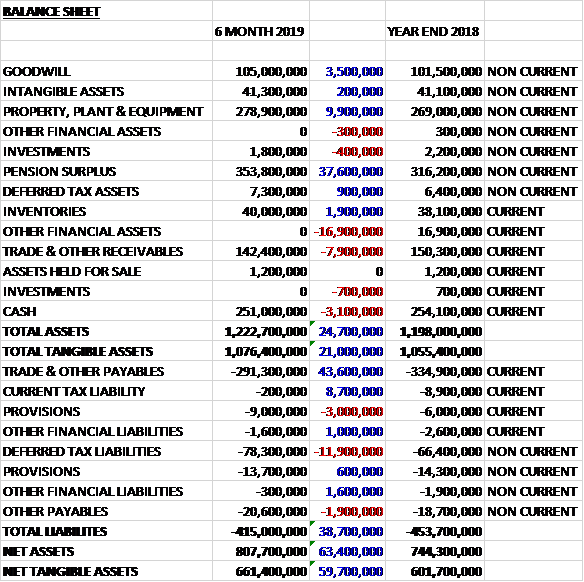

When compared to the end point of last year, total assets increased by £24.7M driven by a £37.6M increase in the pension surplus, a £9.9M growth in property, plant and equipment, a £3.5M increase in goodwill and a £1.9M growth in inventories, partially offset by a £16.9M reduction in other financial assets, a £7.9M fall in receivables and a £3.1M decrease in cash. Total liabilities declined during the period as an £11.9M increase in deferred tax liabilities and a £2.4M growth in provisions was more than offset by a £43.6M decline in payables and an £8.7M decrease in current tax liabilities. The end result was a net tangible asset level of £661.4M, a growth of £59.7M over the past six months.

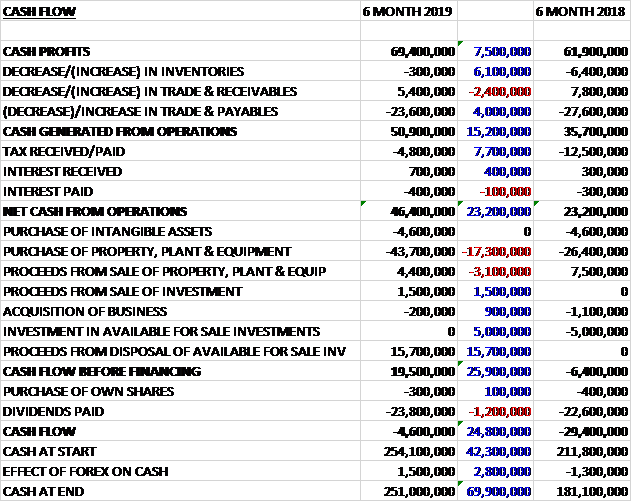

Before movements in working capital, cash profits increased by £7.5M to £69.4M. There was a cash outflow from working capital but this was less than last time and after tax payments declined by £7.7M the net cash from operations was £46.4M. The group spent £43.7M on property, plant and equipment along with £4.6M on intangible assets but they recouped £15.7M from the sale of an available for sale investment, £4.4M from the sale of fixed assets and £1.5M from the sale of an investment to give a free cash flow of £19.5M. This didn’t cover the £23.8M paid out in dividends so there was a cash outflow of £4.6M and a cash level of £251M at the period-end.

After adjusting for non-recurring items, the group reported stable underlying operating profit in line with expectations. They have been able to offset margin pressure in EMEA Services through efficiency savings and revenue growth.

The operating profit in the EMEA Services division was £40.9M, a decline of £6.4M year on year due to a £6.5M benefit from non-recurring items last year. Excluding this, profits were broadly flat as the SSRO margin pressure was offset by efficiency improvements and revenue increases. There was a £42.2M increase in orders, primarily due to greater volumes of small value orders in maritime, land and weapons, and cyber, information and training following greater UK MOD commitments during the period.

Within the air and space business a key success has been winning the Engineering Delivery Partner framework contract with the MOD. This was signed in early October and covers the provision of all engineering services to DE&S, the MOD’s procurement body. The team consists of QinetiQ, Atkins and BMT and will lead the provision of engineering services with the aim of providing improved performance at reduced cost.

The group continue to add services to their Strategic Enterprise contract. During the period they added work for Chinook and Typhoon mission systems assurance. The deployment of their test aircrew training is progressing well. Their new fleet of aircraft are all being delivered to schedule and they are complementing their new fleet with a modernised syllabus. The Solar Electric Propulsion System will provide the engine power behind the BepiColombo mission to Mercury with the spacecraft due to start its transit in December 2018 with the group continuing to provide ground based testing to support the mission.

Within the maritime, land and weapons business the group’s investment in the MOD Aberporth air range will enable the first live weapon firing in the UK from the RAF’s new F35 Lightning II aircraft later this year which creates a potential opportunity for the group as the UK and other European nations assure new fleets of this aircraft. Improvements to the MOD Hebrides range will enable them to host Formidable Shield 2019 and deliver scenarios that combine traditional weapons with complex electronic warfare trials.

In addition to missile firings for a new Polish customer and further work from the German armed forces, the group have also hosted commanders from the UK Carrier Strike Group and the US Marine Corps as they prepare to deploy the new Queen Elizabeth class aircraft carriers. Shortly after the period-end they were awarded a £9M extension to the Naval Combat System Integrated Support Services contract to cover mission systems on the new UK QE class aircraft carriers.

In the cyber, information and training business the group were awarded a three year contract with options to extend for a further two years, worth up to £95M to support the UK MOD in delivering next generation battlefield tactical communications and information systems. They were also awarded a £7M contract to assure the Falkland Islands Ground Based Air Defence systems. As part of this they will build and maintain a synthetic environment for testing the Sky Sabre 3D radar surveillance systems used by GBAD and provide the support for live fire testing.

The business in Australia continues to perform well, delivering organic revenue and order growth supported by a number of contract extensions within the professional services business. The group are in a consortium, led by Nova Systems, that has been selected as one of only four major service providers through which the Australian government procured defence capabilities. They expect their involvement in this to drive further growth in the business. Building on their UK work on the new QE aircraft carrier, they were selected by Oman to deliver ship helicopter operating limit trials ahead of a Royal Navy and Omani Navy exercise. This is the first time they have delivered such trials for an international customer.

The operating profit in the Global Products division was £10.2M, flat year on year. Orders fell by £20.4M against a strong comparator which included a number of significant multi-year contracts, notably the €24.2M spacecraft docking mechanism order with the ESA. Revenues were up 24% driven by an £8.9M increase in QinetiQ North America due to robotic, survivability and maritime product programmes and £6.5M QTS Banshee target sales to India. At the start of the second half the division had 86% of its full year revenue under contract compared to 80% the year before. The reduction in margins was the result of timing and mix of product sales during this period, in particular lower license income couple with lower profitability in OptaSense. Full year margins are expected to be in line with previous years.

The North American business was awarded the Route Clearance and Interrogation System robotics programme of record. This contract with a potential value of up to $44M is for larger vehicles. They also secured a contract to convert large army vehicles into ones capable of remote operation. The broader robotics portfolio continues to perform well including continued demand to upgrade, repair and service the Talon product range. They have been selected as one of two suppliers for the Engineering and Manufacturing development phase of the Common Robotic System programme of record. The EMD will last around ten months, during which time the US DoD will test and evaluate robots from the two suppliers. The total budget for the programme is $429M in the form of an indefinite delivery and quantity contract over seven years.

They also secured a strategic milestone with an order for their Dolphin underwater acoustic networking product. This technology allows for full duplex underwater acoustic networking with many potential applications. Demand for light weight and cost effective survivability products such as Q-Nets and Last Armor was also strong.

In the OptaSense business the group were awarded the contract to protect a new pipeline for the Permian Basin in Western Texas. They will provide monitoring of the pipeline, including leak detection. They have continued to develop the technology, increasing the effective range of each sensor by around five times whilst also enhancing the sensitivity. This further supports their offering for long distance linear assets such as roads, railways and national borders. They have delivered Phase O of the 1,841km Trans Anatolian Natural Gas Pipeline project, the largest single system award for the business.

In the Space Products business, the group won a two year contract with Effective Space Solutions to test and deliver docking mechanisms for two satellite servicing space drone spacecraft. The mechanism will provide a non-intrusive, safe and secure attachment between the spacecraft and existing satellites in ordbit.

In the EMEA Products business QinetiQ Target Systems continued to deliver good growth and agreed a framework contract with the US Target Management Office. In addition they completed the first deliveries of targets to the Indian Army and Navy. They have launched their secure satellite communication product Bracer and have seen positive early interest. The product allows for secure but cost effective global comms on a push to talk and group basis using the Iridium Low Earth Orbiting satellite network. They have also won a £2M order to develop Software Defined Multi-Function LIDAR for the UK MOD for incorporation into Airbus’ Zephyr programme. This product allows multiple functions such as communications, target acquisition and 3D mapping from a single small sensor.

Generally the UK trading environment remains mixed. The MOD is looking to achieve significant cost savings with further clarity expected in the MDP review which is currently underway. In the US expenditure is expected to remain robust and the Australian government intends to steadily increase defence spending up to 2021. Outside these regions, the group have identified Germany, France, Sweden, Canada and the Middle East as priority markets. The business in the Middle East is making encouraging progress, although it is still early days.

The group seem to be making good progress in their international business where revenues grew by £28.4M. In the US they won their first robotics programme of record for Route Clearance Interrogation System Type 1, worth up to $44M. They were also down-selected as one of two companies for the Engineering, Manufacturing and Development phase on the Common Robotics System, an opportunity worth up to $429M in total.

Capital commitments at the period-end include £29.5M that will be wholly funded by a third party customer under a long term contract arrangement.

The group expect the changes in the baseline profit rate to create a £6M headwind to profitability in 2019 but the headwind is expected to moderate in 2020 and beyond. Negotiations are progressing well for the remaining scope of the LTPA not covered under the December 2016 amendment. As part of these negotiations they will commit to delivering efficiencies and change to an output-based contract. They will be responsible for the investment to renew capabilities and modernise the LTPA, improving T&E capabilities for UK customers, as well as attracting international and industrial users. Their objective is to secure the pricing to 2028 with a similar level of investment and recovery mechanism to the 2016 amendment.

The modernisation of the air ranges agrees as part of the 2016 amendment is making progress and has included the installation of new safety critical systems on St Kilda and the delivery of new tracking radar for the Hebrides which remains on schedule.

After the period-end the group completed the acquisition of EIS for €70M. The business is a provider of airborne training services in Germany, delivering threat representation and operational readiness for military customers. Also in October the group acquired 85% of the shares of Inzpire with an arrangement to acquire the remaining 15% after two years, for a total consideration of £23.5M. The business is a provider of training services to the RAF and British Army and made an EBITDA of £2M last year.

The good first half means that the group are well placed to meet their expectations for the full year performance. The EMEA Services division delivered 3% organic revenue growth in the first half and has 91% of 2019 revenue under contract. The division is expected to deliver modest revenue growth this year, although the lower baseline profit rate for single source contracts represents a continued headwind for margins. The Global products division delivered a 25% organic revenue growth in the first half with 86% of full year revenue under contract. It is on track to meet expectations for further organic revenue growth this year and the full year operating margin is expected to be in line with last year.

The group expect full year capex to be at the upper end of previous guidance of £80M to £100M. They are now positioned for sustainable and profitable growth and continue to take steps to mitigate the effects of changes in the UK single source profit rate and expect this headwind to moderate in 2020, enabling growing revenues to deliver increased profitability. Overall expectations for 2019 as a whole are unchanged.

At the period-end the group had a net cash position of £249.1M, a decrease of £17.7M over the past six months. At the current share price the shares are trading on a PE ratio of 15.3 which increases to 16.8 on the full year consensus forecast. After the interim dividend remained the same the shares yielded 2.3% which increases to 2.4% on the full year forecast.

Overall then this has been a solid period for the group. Profits did decrease but this was due to non-recurring items and underlying profits were flat. Net assets increased and the operating cash flow improved, although not much free cash was generated and this did not cover the dividends. The group have done quite well in combating the SSRO margin reduction headwind and after this year, hopefully that will dissipate. The global products division grew but profits remained stagnant due to a reduction in margins. With a forward PE of 16.8 and yield of 2.4% these shares are probably priced about right.

On the 31st January the group released a trading update covering Q3. They continued to perform well and the board are maintaining their expectations for group performance in the current year. The EMEA services division continued to deliver encouraging organic order and revenue growth compared to the prior year. Revenue under contract and operating profit were in line with expectations. Discussions with the UK MOD on the remaining scope of the LTPA continue to make good progress. The group aims to secure pricing to 2028 and agree a similar level of investment and recovery mechanism to the December 2016 amendment.

The Global Products division delivered positive organic order and revenue growth compared to the prior year, with underlying operating profit improving during Q3. Revenue performance was particularly strong in North America.