Redrow have now released their final results for the year ended 2018.

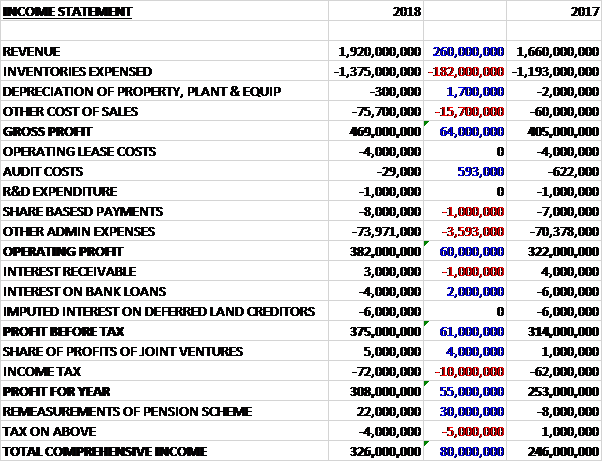

Revenues increased by £260M and after inventory expenses grew by £182M and other cost of sales were up £14M the gross profit was £64M higher. Share based payments increased by £1M and other admin expenses were up £3.6M to give an operating profit £60M higher. Interest costs fell by a net £1M, the profits from joint ventures increased by £4M but tax charges were up £10M which meant that the profit for the year was £308M, a growth of £55M year on year.

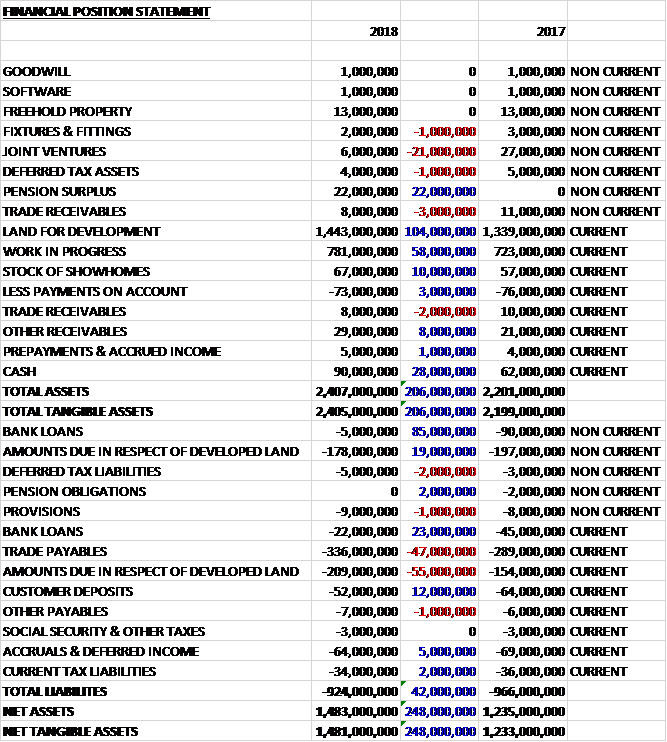

When compared to the end point of last year, total assets increased by £206M driven by a £104M growth in land for development, a £58M increase in work in progress, a £28M growth in cash, a £22M increase in the pension surplus and a £10M growth in the stock of show homes, partially offset by a £21M decline in the value of joint ventures. Total liabilities declined during the year as a £36M growth in the amounts due in respect of developed land and a £47M increase in trade payables were more than offset by a £107M decline in bank loans and a £12M decrease in customer deposits. The end result was a net tangible asset level of £1.481BN, a growth of £248M year on year.

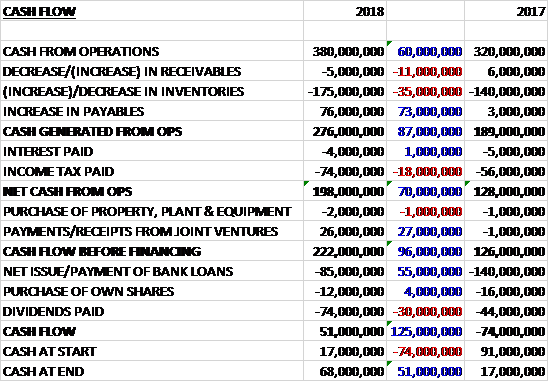

Before movements in working capital, cash profits increased by £60M to £380M. There was a cash outflow from working capital but this was lower than last time and after tax payments increased by £18M the net cash from operations was £198M, a growth of £70M year on year. The group spent £2M on capex but received £26M in payments from joint ventures to give a free cash flow of £222M. Of this, £85M was used to pay back bank loans, £74M on dividends and £12M on share buy-backs. The end result was a cash flow of £51M and a cash level of £68M at the year-end.

Group turnover rose by 16% as a result of the increase in legal completions to 5,913 along with a 7% rise in the average selling price to £332K. The increased selling price was mainly due to the faster growth of the Southern business. With firm control to operating costs, operating expenses as a percentage of turnover reduced from 5% to 4.5%.

Despite the uncertainty surrounding Brexit, demand for new homes continued to be robust and overall house price inflation has moderated to 2%. With the exception of Central London where they only have a handful of properties to sell, they continue to see encouraging levels of demand for their homes. The group entered the year coming year with an order book of £1.14BN, an increase of £110M. Help to Buy continues to support home buyers and the housing industry and in the last year, 1,794 of private reservations were secured through the scheme (a similar amount to last year).

During the year the group added 7,455 plots to their current land holdings. Of these, 2,727 were converted from their strategic land. As a result, net of completions and re-plans, their current land holdings increased by 1,530 plots to 27,630. Their strategic land holdings also increased by a net 4,300 plots to 30,700. Growing the number of outlets in line with the increased land holdings remains a challenge as the journey from outline planning permission to implementable planning permission remains bureaucratic. The gross development value of their total land holdings now stands at £20M.

The new East Midlands division made its first full year trading contribution and the Southern divisions continue to grow strongly as they target increased market share. Colindale Gardens in North London also made a significant contribution, delivering its first completions. They have announced the launch of a new division in Thames Valley and reorganised their London operations into East and West to focus on growth in this area. They have also restructured Harrow Estates to help manage and support their forward land activities.

The land market remained attractive throughout the year, they acquired 7,455 plots and increased to 27,630 plots in total, representing 4.8 years of supply. Pull through from Forward Land accounted for 2,727 of the plot acquired. The average size of sites acquired was around 180 plots and the larger sites were generally acquired on more favourable terms. The owned plot cost increased by £1,000 per plot to £71K, reducing slightly to 19% of the average selling price of legal completions.

The £24M improvement in the pension scheme is mainly due to the increase in corporate bond yields along with a decrease in the market’s long term expectations for inflation.

Going forward, demand for the group’s homes remains strong. Despite Brexit and the exceptional summer weather, sales revenue in the first nine weeks of the year is in line with last year. They expect to grow their land holdings and increase the number of average outlets by 5% to 130.

At the current share price the shares are trading on a PE ratio of 6.7 which falls to 6.4 on next year’s consensus forecast. After a 65% increase in the full year dividend the shares are yielding 5.1% which increases to 5.4% on next year’s forecast. At the year-end, the group had a net cash position of £63M compared to a net debt position of £73M at the end of last year.

On the 7th November the group released a trading update. For the first 18 weeks of the year they have traded in line with expectations. They continue to see good demand in their regional businesses with most sites sold well in advance. The London sales market has remained subdued, however, affected by high stamp duty and Brexit uncertainty.

The value of net private reservations was in line with last year at £588M. The average selling price was up 4.6% to £388K but the sales rate per outlet reduced slightly entirely due to the London market. The total order book increased by 11% to £1.2BN. The operational cash flow was strong with net cash currently standing at £132M compared to a net debt position of £25M last year.

Overall then this has been a good year for the group. Profits increased, net assets grew and the operating cash flow improved with plenty of free cash being generated. Both the number of completions and average selling price improved, the land market remained good and outside London demand remained strong. The issues in London are a concern and of course Brexit looms large but with a forward PE of 6.4 and yield of 5.4% these risks seem to be at least partly factored in and I think the shares are looking decent value.