Air Partner have changed their end of year date so this is an interim update but it includes the last 12 months of finances.

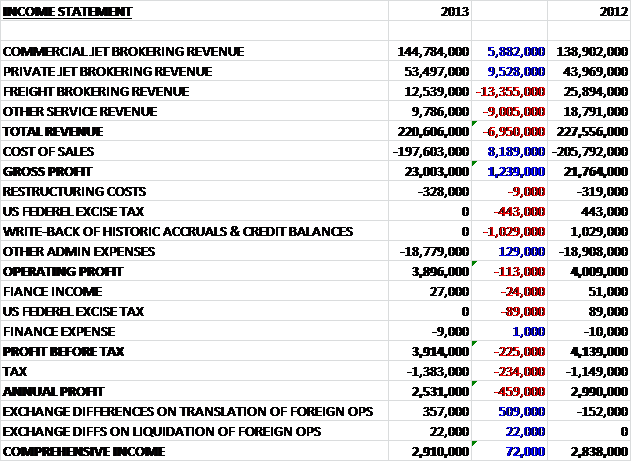

When compared to last year, revenues fell by just under £7M but there were differing fortunes for the four divisions. Private Jet brokerage performed the best, up £9.5M; commercial jet brokerage fared reasonably well too, being up by £5.9M. This was counteracted by a crash in both freight revenue and other services, both of which nearly halved during the year. Cost of sales decreased, however, which meant that gross profit improved by £1.2M year on year. Admin expenses remained unchanged but the group did not benefit from the one off income received last time due to the release of various accruals and provisions. Therefore operating profit was marginally lower, down £113K at £3.9M. Again, the group did not benefit from a one-off finance income and they had a larger tax bill which meant that overall, annual profit was down by nearly half a million at £2.5M.

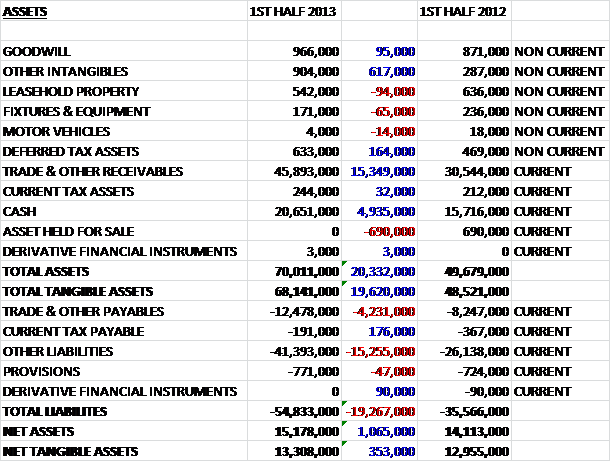

Total assets at the half year point of 2013 were just over £70M, up by more than £20M. This increase was driven by a £15.4M hike in receivables and nearly £5M more cash on the books. There was also an increase of £617K in other intangibles. Liabilities, however, also increased, driven by a £15.3M increase in “other liabilities” and a £4.2M jump in trade and other payables, with provisions up slightly to £771K, £473K of which are held in relation to the potential costs of third party claims following the closure of Air Partner Private Jets that are due to be settled by March 2016. The rest of the provisions relate to restructuring costs. This means that net tangible assets increased by just £350K to £13.3M.

Before movements in working capital, cash flow was £454K down on last year at just under £3.7M. Both payables and receivables increased considerably, put payables were up at a faster rate so cash from operations was actually £7.4M after working capital movements were taken into account. This was £4.8M worse than last year, though, because of a decrease in receivables in 2012. The group paid out £467K more in tax and did not receive the £664K they received from the administrators last year so net cash from operations more than halved to £5.7M. This year, cash spent on intangibles more than doubled to £640K but this was counteracted by an £815K gain from the sale of their plane. Dividend payment increased by £231K so the overall cash flow was £3.9M, which was £5.5M less than last year but still a decent return. Favourable exchange differences boosted this further by £1M.

From a 4% improvement in revenues, Commercial Jet Broking profits increased by 46% to £2.3M. The division has reacted to the reduction in government and conference business by concentrating on tour operating, automotive, sport and oil & gas (opening an office in Houston to service this market). Progress in the oil and gas sector has been good with client numbers up 50% on last year. Performance in the US was ahead of expectations, driven by investment in brokers, large corporate events, the White House and the repatriation of stranded passengers. Performance in the UK was also significantly ahead of that of last year.

Private Jets had a very good year with revenues up 22% and profits increasing by 47% to £1.5M. This was led by a strong performance the US, UK and France. Sales of the Jet Card continued to improve during the year and they were up 35%. Freight Broking fared less well as revenues fell by 52% and profits fell by £100K to just £200K, predominantly due to the conclusion of a large government contract and the continued weakness in the global air freight market. Support Service revenues nearly halved during the year reflecting the fact that the division is considered more of an internal support division than one that is expected to show a lot of profit. The profits were still £200K, however, driven by an increase in emergency planning.

Although revenues were down, a tighter control over costs meant that profitability improved, driven by both private and commercial jet brokering, with the freight business performing badly. The cash flow was decent enough, but due mainly to adverse working capital movements, was worse than last year. At the current share price the dividend yield is a decent 3.3%, after the interim dividend was increased by 10%. The current P/E is a reasonably expensive 23.4, although the underlying P/E is 21.3. The big cash pile is a good safety net but I am not sure that there is enough potential here to warrant the current share price.

On 6th November, it was announced that Tony Mack, a director, was retiring from his position. This is relevant because he is the son of the founder, and has been offered a life presidency position and that he has sold a substantial amount of shares for retirement purposes.

On 6th December the group released a statement covering the six month period to December. Commercial Jet and Private Jet divisions both continued to trade in line with expectations with growth in Commercial Jets driven by the UK and Europe and growth in Private Jets driven by the UK and the US. The Freight division performed significantly ahead of the comparative period last year with assistance to aid agencies driving the performance here. Despite this, the groups profit expectations for the period remain unchanged.

On the 20th December, the group announced that Gavin harles, the CFO will leave the company after four years to continue his career elsewhere. There may be nothing in it, but this does leave me slightly nervous.

On the 31st January the group released a brief statement stating that profit expectations for the full year remained unchanged.