TT Electronics is an electronics company with three different reporting groups. Components are specialist resistive components and microcircuits, connectors and interconnection systems; Sensors are electronic accelerator pedals, engine and wheel speed, temperature and pressure sensors and chassis height sensors; and Integrated Manufacturing Services is the provision of global electronics manufacturing capability with logistics and integrated solutions. The group is active in six different markets: transportation is the most important market, followed by industrial, defence & aerospace, medical, telecoms and power generation.

TT Electronics have now released their final results for the year ending 2012.

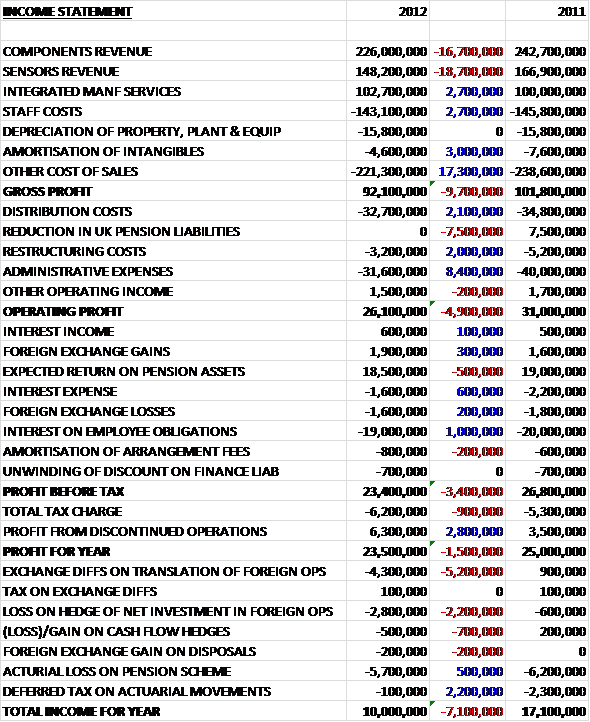

Overall revenue fell for the year with sensors revenue down the most (£18.7M) and components revenue falling £16.7M, somewhat mitigated by a £2.7M increase in Integrated Manufacturing Services revenue. Cost of sales also fell, however, and the gross profit was £92.1M, down by £9.7M. The comparative figure was further improved by a £2.1M fall in distribution costs and an £8.4M reduction in admin expenses, somewhat mitigated by the lack of a £7.5M reduction in pension liabilities that occurred last year. These, along with some smaller differences, such as a reduction in restructuring costs, which this year mostly related to the closure of the components operation in North Carolina, meant that profit from continued operations before tax was £3.4M lower. The group also received £6.3M of profit from discontinued operations (relating to the Secure Power division), which won’t occur next time to leave the profit for the year at £23.5M, down by £1.5M.

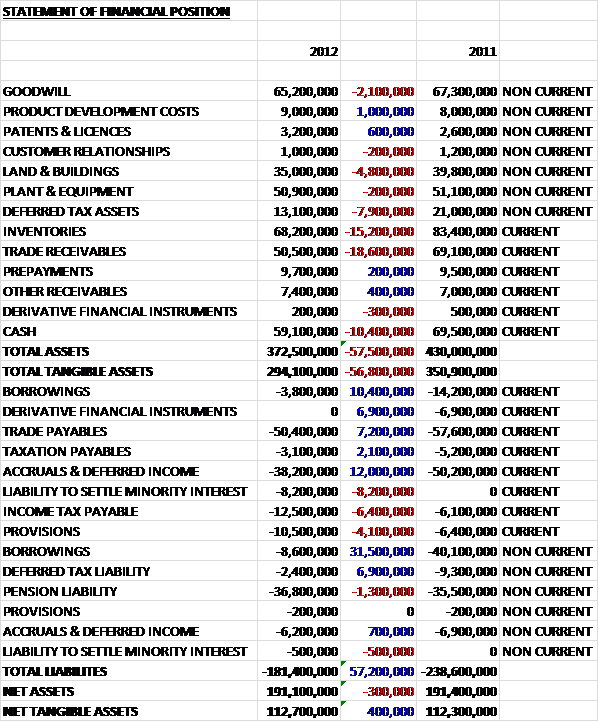

Total assets for the year were down by £57.5M at £372.5M. The largest falls were an 18.6M decline in Trade Receivables, a £15.2M reduction in inventories and a £10.4M fall in cash. There were also some smaller falls in deferred tax assets, land & buildings and goodwill. Thankfully, liabilities also fell considerably with a huge £41.9M decline in borrowings, a £12.7M reduction in accruals & deferred income and declines in deferred tax liabilities somewhat mitigated by an £8.2M liability to settle a minority interest, a net increase of £4.3M taxation payable and a £4.1M hike in provisions, due to an increase in legal provisions. Overall, then, net tangible assets were just about flat at £112.7M.

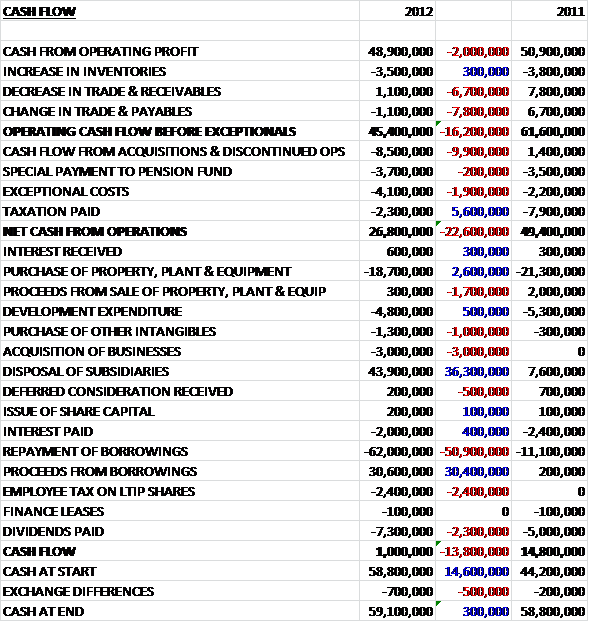

At £48.9M cash profits were £2M down from last year before slightly adverse working capital movements, particularly an increase in inventories, gave an operating cash flow of £45.4, which was £16.2M worse than last year because of particularly favourable movements in payables and receivables. Acquisitions and discontinued operations gave rise to an £8.5M outflow of cash compared to a £1.4M income in 2011. A further £3.7M payment to the pension fund, £4.1M in exceptional costs and a tax payment meant that net cash from operations was £26.8M, £22.6M below that of last year. This cash was spent on capital expenditure and dividends and the £43.9M of cash received from the disposal of subsidiaries was mainly used to pay down borrowings. The overall cash flow at the end of the year was a modest income of £1M, down from £14.8M in 2011. A little disappointing really, considering the disposal.

During the year, the group disposed of the whole Secure Power division. Dale Power Solutions was sold for £10.6M and Ottomores was sold for £29M. Due to the assets that were disposed of along with the businesses, the group made a net profit of £6.8M on the disposals. The group also made an acquisition, buying ACW Technology for £3M in cash and £100K of deferred consideration. On the surface, this seems like a good deal because the value of inventories and net receivables came to £3.1M on their own and there was also £300K of fixed assets acquired. The acquired company provides manufacturing services to clients in the defence, aerospace and industrial markets.

The group seem to be moving a lot of their manufacturing plants to lower cost regions. During the year, they expanded the Mexicali facility in Mexico, a new facility was established in Romania and a new engineering facility was opened in India.

An example of the work the components division has been doing this year is the design and manufacture of blood sensing oximetry technology that delivers accurate non-invasive data, this work has been conducted with CAS Medical Systems. The Sensors division has designed and developed a second generation combined pressure and temperature sensor, which has already won a major order from BMW. In China the IMS division has won new business with Aviage systems to provide avionics solutions for the next generation C919 Chinese built commercial airliner.

After the balance sheet date, the group purchased the 49% of Padmini TT Electronics that they did not already own for £8.2M plus £500K of deferred consideration.

Net cash was fairly flat year on year, increasing by £300K to £59.1M, which is certainly a big pile of cash. The final dividend was increased by 0.3p per share and at the current share price the dividend yield is 2.5% which is decent rather than spectacular, the yield is fairly well covered, however. At the time of writing the P/E is currently 13.6, which is not that taxing but due to a predicted fall in EPS next year, the P/R next year is 15.9, which is starting to look a bit worse value-wise. It is disappointing to see that revenues across the two largest businesses were down, but due to a fall in costs, profits were no lower when one-off items were discounted. It has been a busy year, there was a large disposal, with the cash being used to reduce debts that has resulted in a large cash pile (some of which was then spent on Padmini); the group is clearly taking measures to reduce costs and as a result the lower revenues do not seem to be affecting profits, but I would like to see more evidence of growth I think before I invest here.