After a strategic review, the group is now split into Sensing and Control, the provision of sensors that convert physical variables into electronic signals, controls that process input from the sensor and instrument systems; Components, specialist resistive and magnetic components and microcircuits, connectors and interconnection systems; and Integrated Manufacturing Services, the provision of global electronics manufacturing capability with logistics and integrated systems.

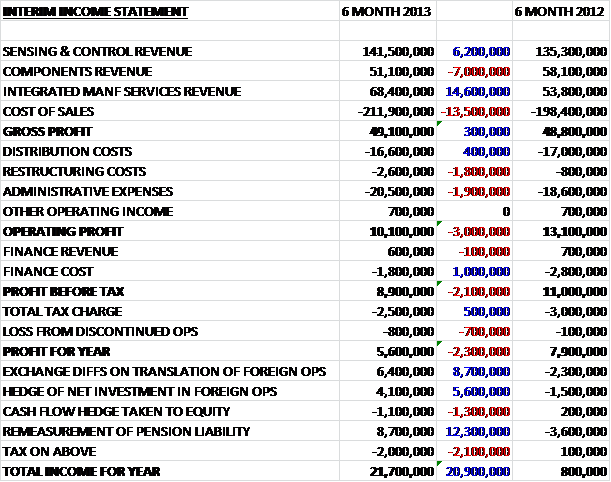

Overall revenues increased during the first six months of the year, after a slow first quarter was followed by a better second quarter. Discounting the favourable exchange rates and the contribution from the acquired ACW business, however, underlying organic revenue was down by just under 1%. There were differing fortunes for each sector, however. Integrated Manufacturing Services did best, up by £14.6M; Sensing and Control also head a steady half year, increasing revenues by £6.2M but the Components sector saw revenues fall by £7M, due to lower demand for industrial resistors and connectors for military markets. Cost of sales increased during the period to leave Gross Profit just £300K higher at £49.1M. Distribution costs improved slightly but admin costs increased by £1.9M and restructuring costs were up £1.8M to £2.6M. This meant that Operating profit was £3M lower at £10.1M before a lower finance costs and tax charge were somewhat mitigated by a £800K loss from the discontinued operation, due to a settlement from TT relating to the disposal of Ottomotores last year, to give a profit for the half year of £5.6M, down by £2.3M.

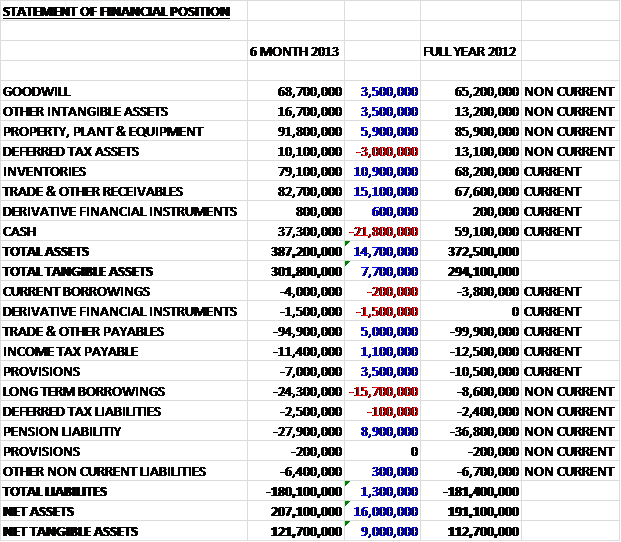

Overall total assets were up £14.7M. The largest increases were seen in trade receivables, up £15.1M; inventories, up £10.9M and property, plant & equipment, up £5.9M. These increases were counteracted by a £21.8M fall in cash levels. Liabilities were fairly stable when compared to the end point of 2012. A £8.9M fall in pension liabilities, a £5M reduction in trade payables and a £3.5M fall in provisions were almost entirely counteracted by a £15.9M increase in borrowings. Overall then, net assets increased by £16M to £207.1M and net tangible assets were up £9M to £121.7M.

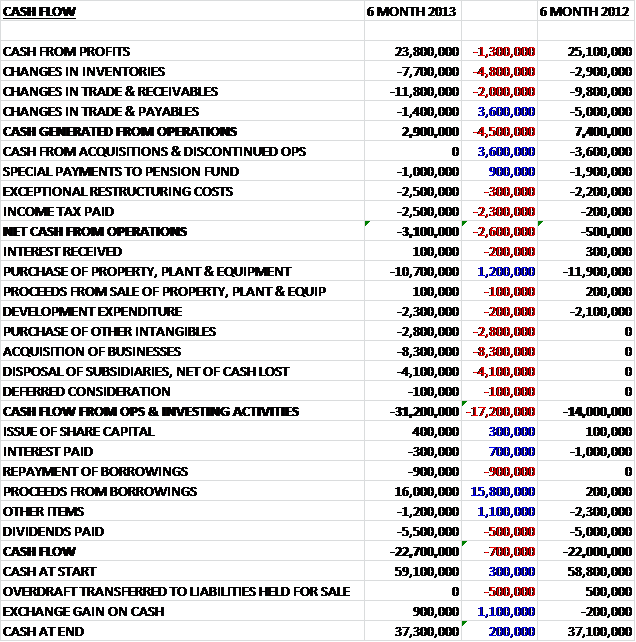

Cash from profits for the first half of the year suffered a £1.3M fall when compared to the same period of last year. There was a huge adverse shift in working capitals with particularly large increases in receivables and inventories due to seasonal factors, the ramp up of manufacturing in Romania, the effect of the ACW acquisition, the closure of the IMS Malaysia plant and lower trading in components and IMS. This left the cash generated from operations at only £2.9M, down by £4.5M. The group then paid a £1M cash charge to the pension fund, although this was less than last year, and had £2.5M of restructuring costs which meant there was a net cash outflow from operations of £3.1M, £500K worse than in the first half of 2012.

The group then spent £10.7M on tangible assets, mainly as a result of investment in the Mexican and Romanian facilities, and £2.8M on intangible assets, along with £8.3M to fund the acquisition. They also managed to lose a net cash amount of £4.1M on disposals! Therefore we see a £31.2M cash outflow before investing activities. The cash flow was give some help with a £16M receipt from new loans but even after this, the cash flow was a negative £22.7M. The group really need to work on their working capital controls to improve the cash generating performance.

As can be seen from the statements, there were a number of exceptional items during the period including the closure and relocation of the ACW Technology facilities from Southampton to Tonypandy in Wales at the cost of £1.1M; the relocation and start-up costs of production facilities in Romania, at a cost of £400K; the relocation of production facilities in Malaysia, at the cost of £500K; restructuring costs relating to the new organisation structure (£400K); final costs relating to the closure of the Boone, NC plant (£200K); the release of a surplus fair value inventory provision created at the date of acquisition of ACW Tech; and the amortisation of the fair value adjustment made to inventory at the date of acquisition relating to ACW Tech (both £400K). This is a lot of restructuring, hopefully it will all bear fruit. The group also announced the “Operational Improvement Plan” which is expected to cost £30M over the next two years and give annual savings of £8M by the end of 2015.

During the half year the group completed the acquisition of the 49% minority interest in Padmini, the Indian Sensing and Control business for £8.3M in cash with a further £500K deferred subject to performance conditions. The earlier acquisition of ACW Technology is apparently now successfully integrated. It can be seen that there is a clear problem with the pension deficit and an agreement has been made with the trustee of the scheme for additional payments of £3.9M in 2013, £4.1M in 2014, £4.3M in 2015 and £4.5M in 2016. This is a substantial amount of money and may act as a bit of a drag on results for years to come but will hopefully go some way to reducing the deficit.

Operating profit for the Sensing and Control business was £8.9M, up by £800K. This performance was driven by progress in industrial and transportation markets, including a better performance for the Austrian operation. Demand in their markets is being driven by tighter emission targets and the need for better performance and the group apparently has a good pipeline of products to take advantage of this. Two new contracts have been won in China for delivery next year, which reflects growth in this market. Going forward, the group is expecting margins to improve due to the move of several operating lines from Austria to Romania.

Operating profit for the Components business was £1M, down by £2M. The connectors business was affected by lower levels of defence spending, which is expected to continue going forward. The resistors business was affected by customers re-balancing inventory levels, which is expected to improve in the second half of the year. The group has invested capital in a new facility at Corpus Christi in the US for the development of thin film resistor products in an effort to refresh the product portfolio.

Operating profit for Integrated Manufacturing Services was flat at £2.8M as the segment suffered lower margins due to the ACW acquisition and the exit of operations in Malaysia. The business entered the second half of the year with a strong order book, however, and is expected to improve margins during the period. The ACW acquisition has come with a number of new clients and the group is increasing its manufacturing footprint by establishing a new facility in Romania alongside the existing Sensing and Control operations.

Overall then, this was a slightly disappointing performance. Underlying organic revenue fell, mainly due to the reduction in military spending in the components division, but net assets were up, due mostly to increased working capital. This increase in working capital, partly due to the ramp up of production in Romania and the ACW acquisition gave rise to a dire cash flow performance as there was an operating outflow of £3.1M (hopefully this can be reversed somewhat in the second half). There are also a lot of exceptional items, and this is only going to increase in the near term as the group has outlined a cost reduction plan this will cost £30M over the next couple of years, which will have an effect on free cash flow going forward, I would have thought. An interim dividend of 1.6p was declared (an increase of nearly 7%) which gives an annual yield of 2.3% at the current share price. The group has a net cash position of £9M, a vast improvement on the net debt position of £7.3M this time last year, due to the disposal of the Secure Power business. Orders apparently indicate that the second half of the year should give a better performance than the first half. So, some signs that this may be a decent investment in the long term but I see a few too many headwinds in the near term to dip in just yet.

On 12 November the group issued a statement covering the first ten months of the year. It was announced that underlying sales were up 2.6%, reflecting the improving trading conditions. It was also stated that the order book had been growing steadily. During the period, the group secured a contract with a major Korean OEM, supplying pedal and power management electronic controls. New contracts were also won supplying control modules, system critical sensors and electonic pedals to three major customers. As part of the “operational improvement plan” the group has announced the transfer of production of sensors and resistors from California to Mexico and the closure of the sales office in Japan, instead relying on distributors in that country. The connectors and harnessing factory based in Smithfield, USA is being closed with some lines being transferred to Perry, USA and some to Abercynon in the UK. So far the savings in transfering lines from Germany to Romania have been lower than expected due to delays in obtaining approvals and supply chain issues, which have now been largely resolved. Due to these problems, the group’s performance for the year is likely to be at the lower end of expectations. It is good to see the increase in business but it is a shame about the supply chain issues. I remain uninvested here.

On the 10th January the group released a pre-close trading statement covering the last two months of the year. Trading was in line with expectaions and underlying organic sales for the whole year were ahead by approximately 5% on 2012. The order book continued to improve and the group is heading into 2014 with a healthy order book. Improved working capital controls helped give a decent cash generation and the group had a decent £26M net cash position at the year end. This cash will be used for internal investment and the odd acquisition. At the same time it was announced that the group was planning to relocate manufacturing operations from Werne to lower cost areas. Due to the ongoing operational plan, there will be a doubling up of inventories and some operational efficiencies which will obviously affect cash flow and hold back margins in the coming year. This is a better update but I still feel the desire to wait on the sidelines until the operational review plan is properly underway.

On the 14th January, the group announced that Geraint Anderson was stepping down as CEO after six years. He will be replaced by Richard Tyson in July. Richard joins from Cobham as president of their Aerospace and Security division. The outgoing CEO is leaving to focus on other projects and came as a bit of a surprise.