Tower Resources has now released their interim results for the year end 2013.

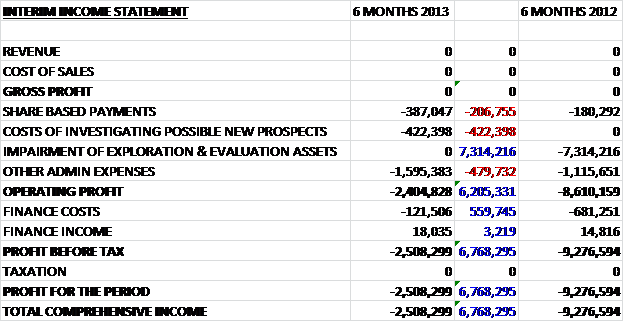

Again, the group received no income and only incurred admin expenses because all the exploration expense is capitalised. Share based payments more than doubled in the half year to just under $400K and the group also incurred a $422K cost for investigating new prospects, presumably relating to the Madagascar acquisition. Other admin expenses also increased, up $480K to $1.6M but the largest difference on the first half of last year was the lack of a total impairment for the Ugandan exploration assets. Therefore operating loss was much lower, down by $6.2M to $2.4M. Finance costs were also much reduced, down $560K so the loss for the year was $2.5M, down by $6.8M on the same period of last year.

At the half year point, total assets were fairly static when compared to the end of last year as the restricted cash and non-restricted cash were used to increase the exploration and evaluation assets. Liabilities, however, increased by $2.5M due to an increase in payables because of money owed to Respsol, the Namibian site operator (this cash was subsequently paid after the end date of the balance sheet), which meant that net assets fell by $2.1M when compared to the end of last year to finish the half year at just under $13M.

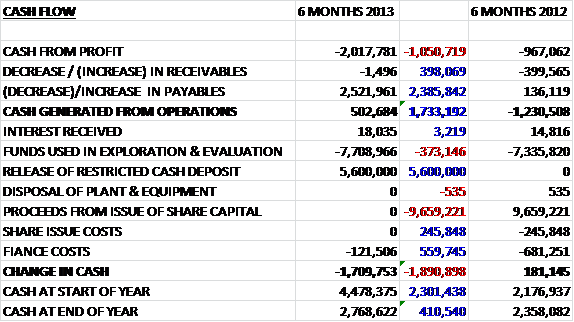

The cash lost before movements in working capital was $2M, $1.1M worse than during the same period of last year. A large increase in payables, however, meant that the net cash from operations was actually in positive territory, a $500K inflow compared to a $1.2M outflow last time. The group also benefited from the release of the cash held in the escrow account which was promptly used in exploration and evaluation, which was $373K higher than last year. The group did not receive any financing for the issue of shares, which brought in $9.7M last year but the finance costs were down slightly, due to lower costs relating to the SEDA. Overall for the half year there was a $1.7K outflow of cash which was fairly modest, mainly due to the release of the withheld cash.

Things are ticking along OK. These accounts don’t really give much to go on, just more of a back-up and confirmation of where the cash is going. Despite the recent disappointments with other companies’ drills in Namibia, I am still happy with my modest holding here to keep the dream alive!

On 12th August, the group released a statement that the open offer had raised £1.04M. Every little helps, but it some way below the maximum that could have been received and shows that only a quarter of the open offer shares were taken up.

On 2nd September the group issued a statement regarding the acquisition of Wilton Petroleum. The operator of the Madagascan block, Ophir no longer intend to drill the commitment well. Tower have not yet indicated what course of action they now wish to take but this is a bit of a set-back in their desire to diversify away from Namibia.

On 25th September the group released a statement covering the settlement agreement between Tower, Wilton and Ophir regarding the Madagascan block. It was agreed that due to the cancellation of the drilling of the block, Ophir would compensate Wilton to the tune of $6M. Tower will then complete the acquisition of Wilton which would basically have the effect of increasing the net cash by $4.25M, after the cash consideration is taken into account – as the shareholders of Wilton will receive some equity in Tower, it is basically a back door way of making a share placing. Tower will then continue discussions relating to the future licencing of the block. It was also mentioned that the group intend to bid on a licence on a block in Cameroon.

On 1st October the group confirmed the completion of the Wilton acquisition for a total value of $4.3M. As mentioned previously, this was basically a different way of raising finance and was the same as a share placing of 4.6% of Tower’s capital at a 35% premium to the share price. So, it is a shame to see yet more dilution of the shares in issue, it seems a good, opportunistic, deal.

On 5th November, the group issued a statement covering the issue of equity to PDF. In payment for their services, the group has issued PDF with 1.8M shares in the company, they now own 0.46% of Tower’s equity.

On 29th November, the group announced that the drillship being used for the Namibian licence had been delayed by a month as it had not yet left the shipyard in South Korea. It is now scheduled to arrive at the drill site on 23rd March.

On the 24th January, the group released an operational update. It was confirmed that they are actively looking for a farm-out partner for 10% of their interest in the Namibian site. Another mile stone is that the drill ship has finally left South Korea and is on its way. It was also announced that more shares had been issued. They raised £820K via a modest draw down on its EEF with Darwin and more shares were issued as an increase in demand for the shares pushed the price over 5p – an interesting concept. Finally, it was stated that they had a cash balance of $18M having already paid $3M towards the drilling costs.

On 5th March the group released a statement announcing that the drill ship had arrived in Namibia. It will undergo final testing before drilling is scheduled to start on the 11th April. Still no news on any farm out deal. I am a bit concerned that no one else seems interested in the site and that Tower may have problems with cash flow during the drilling process.

On the 9th April the group made a number of announcements. They included a placing of shares to raise £19.3M to fund the rest of the Namibian drilling; an acquisition of Rift Petroleum, a company with interests offshore South Africa and onshore Zambia and the farm in to block 2B in Kenya alongside Taipan Resources and Premier Oil. The placing was made to institutional investors and the directors were unable to participate as the company is in a close period but it was nonetheless over-subscribed. As the share price improved, the board made the decision that a placing would be less dilutive to shareholder value than the 10% farm out that they have been chasing previously. It does seem to be the correct decision on the face of it but it could indicate that there was a lack of interest in the potential farm out and it would have been nice if the board disclosed that a placing was one of the options they were looking at.

The drill ship is schedule to commence drilling in Namibia around the 17th April. Based on the CPR update the well is targeting risked resources of about 496mmboe. The group has used the balance sheet cash of $14M along with a part of the proceeds from the placing to finance the remaining firm well costs and other PEL0010 license activity, assuming the project continues into the second renewal phase.

The placing also provided the funds to acquire Rift Petroleum and has given the group a 50% interest in the Algoa-Gamtoos license offshore South Africa, which is at an early stage in the exploration process. Before completion of the deal, the vendor will provide $7.4M to fund the completion and processing of the 3D seismic programme and about $2M of funds from the placing will be used to finance other license activity in South Africa and Zambia.

The group has also agreed to farm in to Block 2B onshore Kenya with Taipan resources for a 15% working interest. The costs of the farm in include $5M in respect of back costs and 2014 seismic costs as well as $3M in well costs relating to the Badada-1 well which is anticipated to spud in Q4 2014. This farm in is expected to be complete in May/June 2014 and is conditional on the consent of the other major partner, Premier Oil.

The placing involves 550M new shares at a price of 3.5p and as mentioned, it will raise £19.3M in new funds. The shares will be placed with institutional and some other shareholders but is not open to the public which is disappointing as it means my interest will be diluted. After the placing the group’s share capital will consist of 3,764BN shares. In all the $32M of new funds will be spent as follows: $5.9M on the remaining approval well costs at the Namibian Welwitschia-1 well, $3M on the PEL0010 license activity in Namibia, the 2014/H1 2015 license activity with regards to the Rift Petroleum acquisition, $5 of back costs and 2014 seismic costs in Kenya, $3M of 2014 well costs in Kenya, $5M relating to the signature bonus and 3D seismic in Q1 2015 in Cameroon. The rest is being spent on G&A, G&G, tax and placing costs. It seems therefore that the group is now well financed for the immediate future.

As mentioned above, the group has acquired the share capital of Rift Petroleum, a private exploration company focused on offshore South Africa and onshore Zambia, in exchange for the consideration shares. As well as Tower, a number of oil majors have also acquired acreage in the country including Exxon, total, Anadarko and Shell. Rift Petroleum’s primary asset is its 50% interest in the Algoa-Gamtoos license alongside New Age Energy Algoa and it covers seven blocks and 11,809 Km2 between two license areas that have been farmed in to by Exxon and Total. The license consists of three prospective basins, algoa to the east, Gamtoos to the west and the Outeniqua deep-water basin.

New 3D seismic in the Algoa Canyon play should be available during Q3 2014 whilst mapping of the existing 2D seismic is ongoing. A farm-out process in respect of the license is still ongoing and there are apparently a number of discussions ongoing regarding interests in the block which Tower intends to continue. Rift Petroleum also has rights to acquire a 50% interest in any exploration right granted to New African Global Energy over the SW Orange Basin area covering three blocks and 21,500km2. The group has also successfully bid and been awarded an 80% interest in two blocks (40 and 41) onshore Zambia. Due to the consideration shares agreement, the founder of Rift, Julian McIntyre, will become a significant new shareholder in Tower.

The other main development was the acquisition of the 15% interest in Block 2B in Kenya, currently owned by Taipan Resources. Premier Oil owns a 55% interest with the remainder still owned by Taipan. The group will pay Taipan $4.5M in cash with a contingent payment of $1M on the spud of a second well. The total estimated mean gross unrisked prospective resources was reported as being 1,593 mmboe. Processing of the seismic data is underway and due to be completed shortly and this data will be used to identify a drilling location for the Badada-1 prospect that is planned to be drilled during Q4 2014. There are also drilling campaigns by Africa Oil, Afren and Tullow due to be drilled in the region during 2014.

The final development is that the group has been named as preferred bidder on the Dissoni block in Cameroon and is considered to be a fairly low risk, low volume target. Subject to finalisation of terms with the Cameroon government, the group expect to undertake 3D seismic during Q1 2015.

Despite not being informed that the group was looking to undertake a placing of new shares, the funds raised here should provide Tower with enough funds for the immediate future. The Namibian drill seems to be well funded and the new acquisitions seem give the group a future should the Namibian acreage not provide and commercial quantities of oil. The Kenyan prospect in particular, looks quite interesting. I am still invested here for the moment, at least until the results of the Namibian well are known.

On the 22nd April the group announced that the Drillship will commence drilling operations in Walvis Bay by 25th April. This is a little later than expected due to prolonged acceptance testing by Repsol in advance of it taking the vessel on a three year contract. The drilling itself is likely to take up to 46 days and during the drilling process there will be no updated to the market with an announcement being made only once operations on the Welwitschia-1 well have been fully completed and analysed.

On the 24th April the group announced that the drillship spudded the well on the 23rd April – we’re off!