Tristel have now released their half year results.

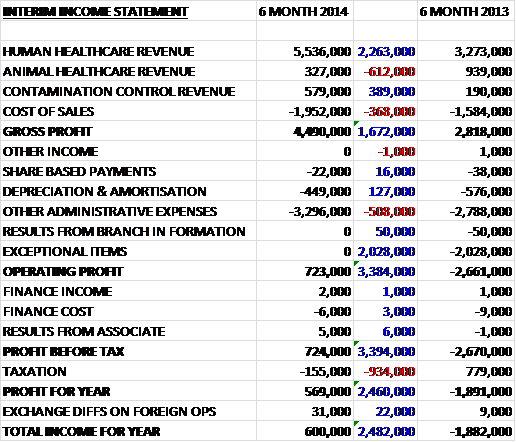

Overall revenues increased fairly substantially. Human healthcare was up £2.3M to £5.5M and Contamination Control more than doubled to £579K but this was mitigated somewhat by a £612K crash in Animal Healthcare revenue. Cost of sales also increased to give a gross profit up some £1.7M to £4.5M. Admin expenses increased year on year, up £508K to £3.3M but the group benefited from the lack of over £2M of exceptional items that occurred last year so operating profit improved £3.4M to £723K. There was a big swing in the amount of tax paid by the group and overall profit for the year stood at £569K, a £2.5M increase on the first half of 2013. Not a bad performance.

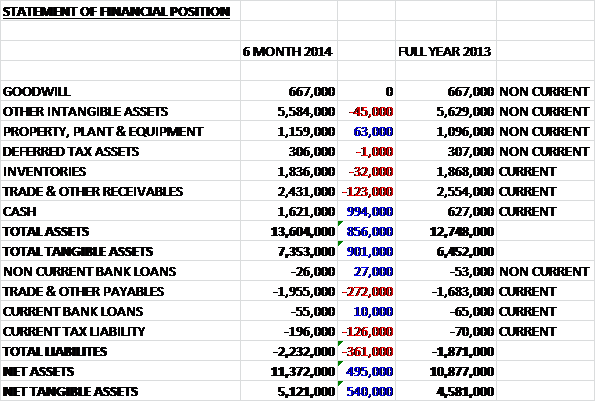

Total assets increased by £856K from the end point of last year. The only two increases were a near £1M hike in cash levels and a £63K increase in property, plant and equipment. This was somewhat mitigated by a £123K fall in receivables and a £45K reduction in intangible assets. Liabilities also increased during the period, driven by rises in payables and tax liabilities. The resulting net asset level was £11.4M, up by nearly £500K.

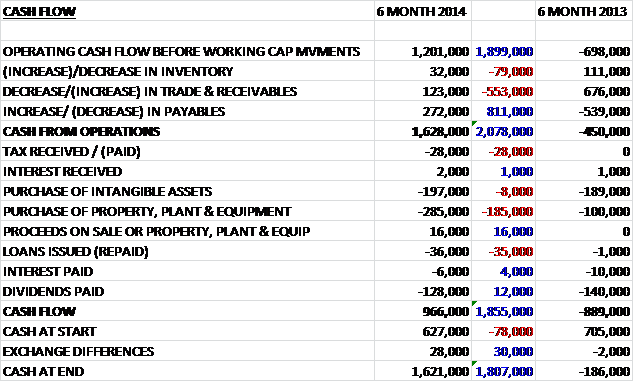

Before working capital movements, the cash flow was a decent £1.2M, which compares well to the £700K outflow in the first half of last year. There was a decent control on working capital, with the group able to increase payables in particular, to give a net cash from operations of £1.6M, £2.1M better than in the first six months of 2013. There was an increase in capital expenditure, and in particular a £185K hike in the purchase of property and equipment, and there was a reduction in the amount paid out in dividends. This meant that the cash flow for the half year was a fairly decent £966K, a whole £1.9M improvement on the situation during the same period of last year.

Sales into the Human Healthcare market grew 88% to the UK and 40% to overseas markets. The growth was led by the Wipes System which is used in ENT, cardiology and ultrasound departments. The main markets outside the UK were Germany, Italy and Australia. Sales of the surface disinfectant products grew by 91% to £800K, so they still make up a small segment of the earnings in this sector. Overall gross profit in this sector increased from £2.2M to £4M.

Sales of the contamination control products increased by 54% to £600K. These products are used in pharmaceutical manufacturing environments, hospital aseptic units and labs. The board believe that this is an area that should experience further growth going forward. Gross profit in the contamination control sector increased from £55K to £297K. Animal Healthcare profits collapsed from £608K to £206K following the loss of the distribution agreement last year.

Going forward, the board believes there is potential for further growth in the current product range and they are constantly looking for new innovations. Examples during the period in question include a new version of the Wipes System that provides barcoding and electronic traceability which extends the product’s intellectual property protection; and a new delivery system for Chlorine Dioxide that the group are calling Tristel Revolver for use in antiseptic units.

At the end of the half the group was in a net cash position of £1.5M compared to net debt of £400K last year. An increase in the interim dividend gives a yield of 1.4% at the current share price. Fairly modest, but nice to have. This is definitely an improvement on last year’s trading as Tristel moves away from its declining legacy products and the overseas growth is good to see. It does seem like this has further to go but any investment here is a bit of a risk. I already have a decent holding so will not be buying any more at the moment. Sill a hold for me.

On the 28th April the group released a trading update for the year. They announced that the momentum seen in the first half has continued resulting in a pretax profit of about £1.5M. This was ahead of market expectations and the group also mention that cash balances have strengthened, exceeding £2.2M at the year end. This is all very encouraging and I am tempted to top up again.

On the 10th June the group released a statement covering the full year. They experienced a rise in sales in all three sectors and across most geographical markets. The pace of growth was higher than previously anticipated and costs remained stable. Therefore their expectations for pre tax profit this year has increased to £1.75M, up from £480K last year. Great stuff!

On the 28th July the group released a trading statement suggesting that results for the year would be better than expected last June. Full year revenues increased by 28% and pre tax profit should come in at £1.8M before share based payments with a net cash position of £2.6M. All good stuff, might be tempted to top up on weakness.