GVC has now released their full year results for the year ending 2013.

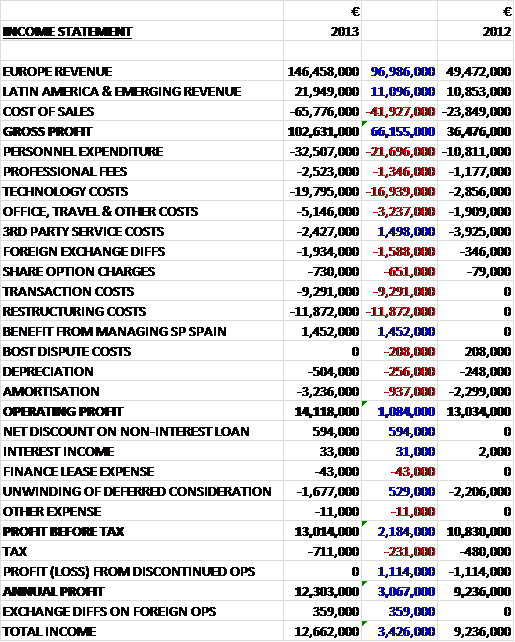

Revenues across both geographical areas increased, with European revenue, making up the bulk of sales, up by €97M and rest of world revenue up by €11.1M. Sports gaming and casino now makes up a similar amount of sales, with sports revenues more than doubling during the year. As would be expected, cost of sales was also up, by the tune of €41.9M to give a gross profit some €66.2M higher than last year. As far as other costs are concerned, we can see that personnel expenditure was up €21.7M and technology costs increased by €16.9M whilst the only cost to reduce was third party service costs, down by €1.5M. There were then a number of one off costs, the largest of which was €11.9M of restructuring costs, €9M of which were redundancy costs, followed by €9.3M of transaction costs mainly relating to legal and other advice. The only one-off gain was the €1.5M received for looking after the Spanish division of the acquisition before William Hill took it over.

So, including all the one-off costs the operating profit for this year was €14.1M, €1.1M higher than in 2012. After this we saw a €594K gain on the net discount on the non-interest loan, actually it is imputed interest which is a concept I find a little hard to grasp. The unwinding of the deferred consideration was €529K less than last year to give a profit before tax some €2.2M better than in 2012 before a slightly higher tax bill was counteracted by the lack of a loss from the disposed business (Betaland) to give the total profit for the year some €3.1M higher than in 2012 at €12.3M.

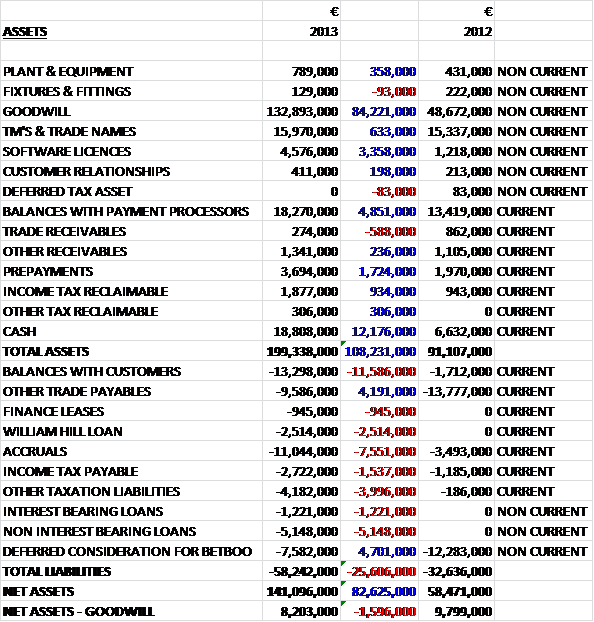

Overall total assets more than doubled to just under €200M. The vast bulk of the increase in total assets was in Goodwill, which increased by €84.2M. There was also a €12.2M increase in cash levels, €3.4M more in software licences and an increase of €4.9M in balances with payment processors, which are funds held by third parties subject to collection after one month or used to make refunds to players. Liabilities also increased, with the largest increases seen in balances with customers, up €11.6M; accruals, up €7.6M; non-interest bearing loans, up €7.6M and taxation liabilities, higher by the tune of €4M. These increases were somewhat mitigated by a €4.7M fall in the deferred consideration to pay on the acquisition of Betboo and a €4.2M reduction in trade payables. This all meant that net assets increased by a huge €82.6M when compared to last year but the vast majority of the increases in assets were intangible so if we take off goodwill, which I don’t consider to be that helpful to the balance sheet, the net asset level is just €8.2M, which was actually €1.6M lower than last year.

Compared to last year the group made far more cash from its customers but also paid out more. Overall, there was an operational cash outflow of €7.7M, which is €16.9M worse than in last year, and a little disappointing. After operations, the group spent another €6.4M in deferred consideration relating to the Betboo acquisition but received a huge amount of cash with the most recent acquisition, along with €8M of loan from William Hill to help complete the acquisition. The bulk of the cash acquired was involved in the repayment of borrowings and the cash spent on dividends jumped €6.8M to €15M. Overall the group had a positive cash flow of €12.2M for the year entirely related to the cash received when the group purchased Sportingbet.

Clearly the Sportingbet acquisition was the most important event to happen during the year. The acquisition did not include the Australian business that went to William Hill and as part of the agreement, a call option was granted to William Hill over Sportinbet’s Spanish assets. Until the 16th September the group was entitled to receive the economic benefit of these assets after which William Hill took them over. As part of the acquisition the group also received a non-interest bearing loan from William Hill. The first instalment of €2.3M is due before the end of 2014, with another due before the end of 2015 and the last repayment due by the end of June 2016. If GVC declare dividends of more than 58c then there is an acceleration in the repayment of the loan. The acquisition was paid for by the issuance of over 29M new shares to the value of €83.9M.

The acquisition of Sportingbet was done to mitigate the earn-out payments arising from the 2011 Superbahis transaction with Sporting bet – one solution, just acquire the company you are paying! The group have also acquired software and additional customers in over 20 additional markets. On acquisition Sportingbet was in quite a bad way, it has a €50M deficit in working capital, was loss making, had fully drawn down on its banking facilities, relied heavily on finance leases and was burning cash. Since the acquisition, the group has turned its performance around and it generated €3.8M of clean EBITDA in Q4. The acquisition was part paid for by William Hill, part by the issuance of new shares to the existing shareholders of Sportingbet and part by a small loan from William Hill.

As can be seen from the results, the group is still paying deferred consideration relating to the Betboo acquisition and higher earnings from the business has meant that this consideration has increased. The agreed payment terms are now four consecutive monthly payments starting in October 2013 of 25% of the NGR for the period commencing January 2013 to the end of September. From October there will also be nine monthly payments of €228K with the final payment taking place in June of this year. There is also an earn-out dependent on certain revenue shares with a floor of €200K per month for the 40 months ending January 2017. In all total deferred consideration is capped at €18.5M but it still seems rather substantial with the payment in 2014 expected to be €4.4M.

The group seems to have made very food progress with debtor days, halving from 82 days to 40 days. There also seems to be a fairly decent diversity of contribution by market as in Q4 the largest origin was Turkey, at 30%; followed by Eastern Europe at 22%, Central Europe at 20%, CasinoClub at 18%. Latin America at 5% and the UK makes up 4% of profit. The group has been working on its mobile offering and has seen a 19% increase in mobile sportsbook NGR and in-play betting now accounts for about 70% of total sports wages placed. Football, tennis and basketball make up the vast majority of sports bets. During the year the group has suffered considerable headwind in the form of the strengthening Euro and during the past year has impacted the group to the tune of €25K a day which makes the underlying sales performance even more impressive.

As mentioned, the group do have an exposure to currency movements. The loss during the year due to foreign exchange was €1.9M, although €1.1M was a one-off translation of the Sportingbet ledgers from Sterling to Euros. In Turkey and Brazil currency conversions are handled by intermediaries so they do not handle these currencies, however these weak currencies are likely to impact profits by about €5M this year.

In the next year the group is looking to achieve further synergies following the acquisition, improving the product offering and looking for new acquisition targets, but they are not currently considering any that will undermine the maintenance of the shareholder dividend. They are also looking to capitalise on the upcoming world cup that is taking place this year by making significant investments in marketing and they are confident that they will meet current market expectations in the coming year. The group is continuing dialogue with regulators in the markets that they operate in but there remains some regulatory risk, particularly in Turkey where the group earns a lot of its revenue and the authorities have made motions to outlaw gambling.

At the current share price the P/E ratio is 18 but next year consensus expects this to fall to a rather cheap 7. The group now pays a dividend every quarter and have announced an 11.5c dividend this time with a special dividend of 4.5c. The yield is 8.2% currently which is pretty spectacular and likely to get even higher during the coming year and I believe is ample reward to put up with the regulatory risk and the slightly confusing annual report!

Overall then, the group has made remarkable progress in turning around Sportingbet, which by all accounts was failing and it will be interesting to see the profits they make now it is contributing to the bottom line. The group is clearly not risk free as they have operations in regions where in some cases, the government has openly stated it is not happy with gambling taking place and it might just be me but I find the language used in the annual report quite difficult to understand. I still don’t get what the agreement with Superbahis is for example. Aside from these issues, however, the shares look cheap. The future P/E ratio is very low the yield seems pretty much the best I have seen from a company growing at the rate of GVC. I am holding at the moment, having topped up fairly recently and will probably hold off until I see some evidence of positive cash flow at the operating level before adding more.

On the 14th May the group released an AGM trading statement covering some of Q2. Net Gaming Revenue was on average 8% higher than last quarter and 11% up on that of the same quarter last year. This includes the adverse currency movements and on the constant currency level, the increase was even higher. The mobile product fared even better with revenues per day double that of last year. The board is encouraged with the strong trading so far this year and are confident that current market expectations will be met for the full year. Decent progress seems to have been made.

Also on the 14th May the group announced that it was entering into a joint venture agreement with Betit. The initial commitment is €3.5M which will be taken from cash flow and will give GVC a 15% share in the joint venture. The group has a call option to acquire the outstanding shares which much take place between July and the end of September 2017. The minimum call option price is €70M with the actual price determined by certain revenue targets and other multiples. If GVC is unable to find the funds for this purchase, then Betit would acquire GVC’s shares at a nominal value. So, basically it seems that the group has deferred some €70M of this acquisition for three years. Betit is an opportunity to enter the lucrative Nordic gaming market and it is already generating daily revenues in excess of €40K. Whilst this is a great opportunity to enter a good new market, I am not sure if the deal is structured in the best possible way – could the group not purchased a higher stake in the business now in order to reduce higher payments later when the joint venture is making more money?

On the 15th July the group released a statement covering the first half of the year, including the World Cup period. A quarterly dividend of 12.5c was announced, which was higher than both last quarter and the same quarter of last year and including the special dividend announced last quarter, represents a dividend yield of a staggering 11.6%. Total NGR in the quarter was €54.8M, up 9% on last quarter and total revenues for the first half of the year were €105.1M, up 45% on the same period of last year despite adverse movements in exchange rates during the period. The results were boosted by the World Cup which also contributed to more customers and greater market penetration, with over 81,000 customers added during the quarter. Overall, all positive stuff and I remain a holder.