Laura Ashley has now released their full year results for the year ending 2014.

Retail revenue was down when compared to last year with store revenue falling by £3.3M and E-commerce/mail revenue down by a disappointing £1.5M. This was somewhat mitigated by a £400K increase in non-retail revenue, driven by increased franchise income. Staff costs increased somewhat but the cost of inventories was down by £7M. This all meant that gross profit was down by £800K. Looking at other costs, we can see that a £1.7M adverse swing in exchange gains/losses was counteracted by small falls in depreciation and store operating leases. Overall, operating profit was nearly flat, down by just £200K to £19.1M. There was a disappointing £900K fall in the share of profits from associates, relating to the Japanese business, but the big moves were a one-off £3.2M gain on the sale of investments, relating to the Moss Bros shares, somewhat mitigated by £2M worth of store closure costs. A lower tax bill meant that the profit for the year was actually up by £1M to £15.7M but when the sale of the Moss Bros shares are ignored, there was a small reduction in profits compared to last year.

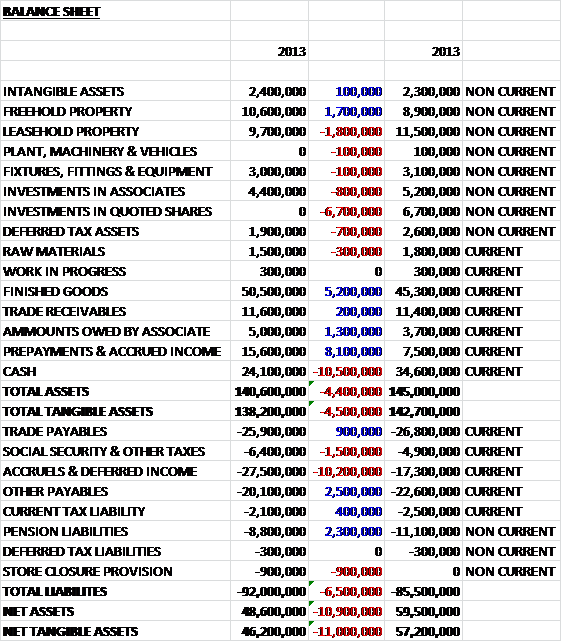

At the end of the year, total assets were £4.4M lower than in 2013. The fall was driven by a £10.5M reduction in cash and a £6.7M fall in the investment in quotes shares relating to the sale of the Moss Bros shares. This was somewhat mitigated by an £8.1M increase in prepayments, including £8M to be received regarding the sale of the shares, and a £4.9M hike in the value of inventory. When compared to the previous year total liabilities increased by £6.5M, driven almost entirely by a £10.2M hike in the value of accruals, mostly relating to £7.3M paid in dividends after the balance sheet date. This was only slightly counteracted by a £2.5M reduction in payables and a £2.3M fall in the pension liabilities. This all meant that net assets were some £10.9M lower at £48.6M.

Before movements in working capital, cash profits were down by £1.5M on last year. As we have seen from the balance sheet there was a fairly large increase in the level of inventories which meant that at £16.8M, the net cash from operations was some £5.6m lower than in 2013. This cash did not cover the dividends, however, as at £18.1M they do not seem that sustainable at this level. The dividend also dwarfed capital expenditure, which at £3.2M was £1.3M up on last year and included investment in IT and the purchase of a property for the development to enhance facilities offered by the hotel (clear as mud, then). Overall, the cash outflow was £10.5M, some £10.1M worse than in 2013 and nowhere near enough to cover the huge dividends. At the end of the year, however, the group still has £24.1M of cash so there is plenty of room for manoeuvre.

Although the contribution from total retail was down slightly, the slack was taken up by non-retail profits including franchising, licensing & manufacturing, and at this point the non-retail profits make up more than 1/3 of the total profit. Total furniture sales decreased by 1.4% and in response the group has increased the breadth of their offering in beds and cabinet furniture with some success achieved with some of the newer ranges. Sales of Home Accessories increased by 0.8%, with the ranges also proving popular with the group’s franchise customers. Decorating sales were up an encouraging 1.9% with significant growth seen in ready-made curtains and paint. The poorest performer was Fashion, where sales decreased by 6.5% this year. Within the year, the second half did perform better than the first half however, and Q4 actually saw a 1.5% growth which indicates that the group may have turned the fashion division around – the figure for the first half of the new year will be important.

During the year the group opened two new stores and closed 5 resulting in a 2% fall in total selling space. The number of franchise stores increased by 20 during the year with new stores in Japan, Australia, Hong kong, Singapore and UAE. Revenues for the franchise stores increased by 4.2% and this is clearly the growth driver for the group. Conversely licencing income collapsed by 21% which was mainly due to the one-off promotional licensing that occurred last year, giving a difficult comparison. New licenses were awarded for new branded kitchens and beauty products. The hotel has now been fully refurbished and launched as a Laura Ashley boutique hotel at the end of July. Revenues for the hotel are expected to grow significantly in the coming year.

As well as the UK, Ireland and France, the group also sells a full product range via online portals to Germany, Austria, Italy and Switzerland and they plan to offer fully translated French and German websites in the coming year which should give a boost to these territories. In the UK, Ireland and France the group also provide the Design service which provides bespoke interior design solutions, the use of which has been growing this year.

Trading conditions do seem to be improving overall. After a difficult first half to the year, the group saw a like for like sales growth in the second half and the first two months of the new year have seen like for like sales growth of 2%, which is an encouraging start that the board believe will be maintained.

The group is still in a net cash position of £24.1M, albeit down from £34.6M last year. At the current share price the P/E ratio is 12.1, which is not too expensive given the cash pile. During the year the group announced two special dividends along with the interims and finals. At the current share price the yield, including the special dividends is a huge 13.5% and even without the special dividends the yield is 7.7%. Operationally the group seems to be making slow progress but the turn-around in fortunes for the fashion division at the start of the current year is encouraging. The franchise income also seems to be improving well and I will be holding on to my shares at this time, for the amazing income level if nothing else.

On the 12th June the group released a statement covering trading in the first 19 weeks of the year. In all, total retail sales were down by neatly 1% but like for like sales increased by 0.7% with Fashion and Home Furnishings recording growth. Two stores were opened and three closed during the year whilst 5 franchise stores were opened in Japan and another 4 in South Korea, although three franchise stores were closed. During the period the group also launched a French language website with a German one to follow shortly (not before time!). Overall, not has changed with this update. Growth levels seem a little disappointing but this was no disaster.

On the 4th August, the group announced that non-executive directors Ms. Ho Kuan Lai and Ms. Frances Boon Wah Ling had resigned with immediate effect. No indication was made of any possible replacements.