Interserve has now released its full year results for the year ending 2013.

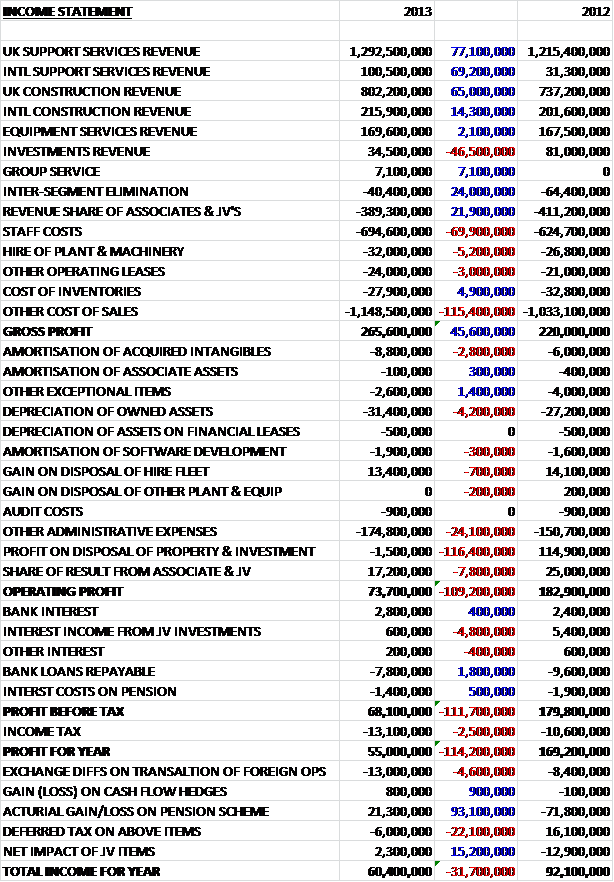

Revenues were up across most sectors and geographic markets, with a £77.1M increase in UK Support Services; a £69.2M increase in international support services, up from just £31.3M last year and a £65M hike in UK construction. Equipment Services were pretty much flat and investments showed a £46.5M reduction in revenue due to the sale of the bulk of the PFI frameworks to the pension scheme. Geographically, the only region to show a decline in revenue was Oceania with the UK, Africa and the Middle East showing the most growth. Cost of sales were also up, but to a lesser degree and gross profit was some £45.6M higher than last year. Admin expenses were also up but the bulk of the difference came from the one-off profit on disposal of investments (£116.4M) that occurred last year and were not repeated in 2013 where a write-down of an investment in the Indian associate actually gave a negative figure, and there was also £7.8M less received from joint ventures, again related to the sale of the PFI frameworks. The “other” exceptional items in 2013 related to bonuses to staff triggered by the exceptional profits on the disposals of the PFI investments. Overall then, due to these one-off costs, operation profit was £109.2M lower at £73.7M.

The main difference in financial income, again came from interest from the joint venture investments being lower (after the PFI disposals) and this, combined with the higher tax rate meant that the profit for the year was £55M, £114.2M lower than in 2012. As the profit on the disposal of investments was £116.4M last year, the difference can be entirely attributed to this and the underlying performance looks rather good, and profit for the year not included exceptional items was £66.1M, £4.1M higher than last year.

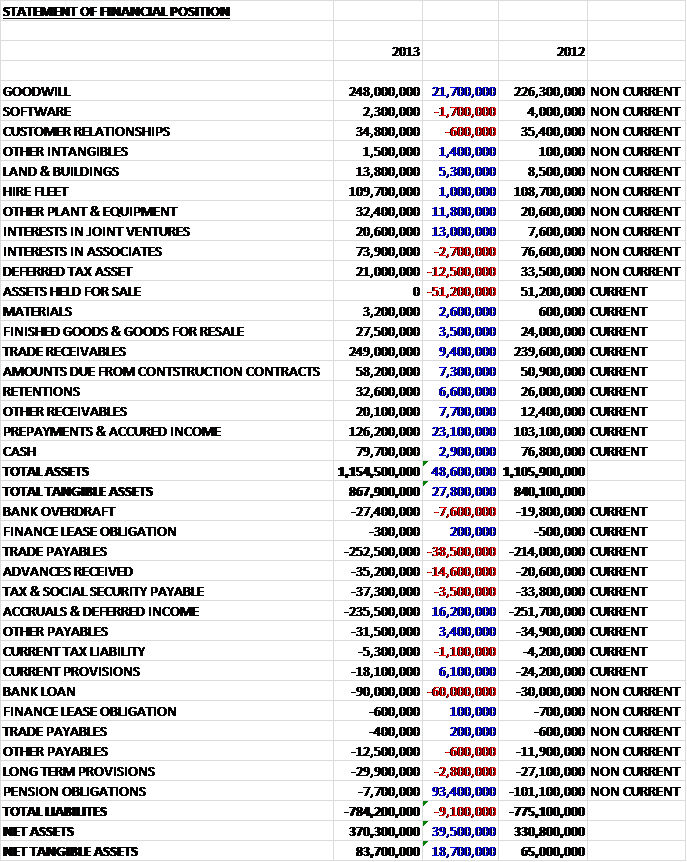

Overall total assets were up by £48.6M. The largest increases were a £23.1M increase in accrued income and a £21.7M hike in the value of goodwill. Other hefty increases included plant and equipment, up £11.8; the value of joint venture interests, up £13M and trade receivables, increasing by 9.4M. These were mitigated somewhat by a £51.2M fall in the value of assets held for sale, relating to the PFIs and a £12.5M reduction in the value of the deferred tax asset. Liabilities also increased during the period, driven by a £60M increase in the bank loan, a £38.5M hike in trade payables and a £14.6M increase in advances received. These are counteracted by a massive £93.4M reduction in the pension obligations and a £16.2M fall in deferred income. Overall then, net assets were some £39.5M higher at £370.3M but when goodwill is taken off, this falls to £122.3M, still £17.8M better than at the end point of 2012.

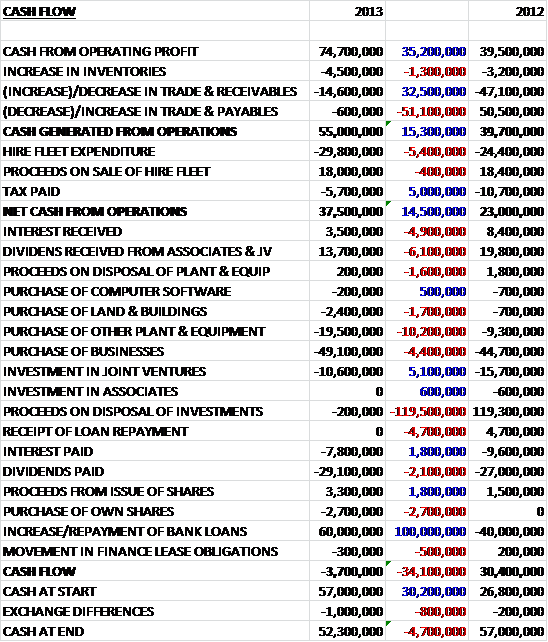

Before the movements in working capital, the cash profits were a remarkable £35.2M higher than last year at £74.7M but an increase in receivables and a small decrease in payables, due to the growth of the business and pressure on payment terms, meant that cash generated from operations was some 15.3M up on 2012. An increase in the cash paid for the hire fleet was counteracted by a decrease in the tax paid so the net cash from operations was still an impressive £14.5M up from last year at £37.5M. Due to the sale of most of the PFI frameworks, both interest received and dividends from joint ventures fell and the group spent another £10.2M on capital expenditure due to investments in back office and refreshing the fleet of the newly acquired businesses. There was also a £49.1M acquisition and a £2.1M increase in dividends. The cash to pay for all of this was received with £60M of new bank loans but despite this the cash flow was still negative to the tune of £3.7M compared to a £30.4M inflow last year. Even if the acquisition was discounted, the group would still have needed further borrowing to remain cash flow positive.

The largest source of profits come from UK support services with equipment services at £20.1M making up the second most important segment. UK construction contributed £14.7M with international construction contributing £13.1M, although profits here did fall when compared to last year. International support services only contributed £4.1M but this total is growing year on year.

During the year the group made a number of acquisitions. Willbros (TOCO) was acquired in January for £25.7M. That group has an 85% interest in two oil and gas businesses, the main one being based in Oman. Paragon Management was acquired in May for £3M. They are a specialist interiors and property refurbishment business. Topaz Oil and Gas was acquired in September for £27.6M. They provide oil field maintenance, fabrication and construction services in the Middle East. The three businesses are already profitable at the operating level with Toco contributing £1.2M, Paragon adding £1.2M and Topaz contributing £300K in the short time it has been part of the group. Given the outlay, Paragon in particular looks like a good buy.

Support service profits in the UK were up 26% to £56M. The group signed a number of new contracts with various customers during the year, including Dixons, the University of Sussex, the BBC, the MOD, Nottingham University NHS Trust, Southwark borough, the Home Office, Magnox and Meggit. One of the larger contract wins was a five year £150M facilities management contract with the BBC. The services span over 150 locations and include critical broadcast engineering and business continuity services. Another contract was a three year deal valued at £15M to provide back office and facilities management services to five Royal Navy establishments in the South West. Services on this contract include logistics, motor transport, HR, payroll and travel.

The group also had some success in extending existing contracts with a home office contract being extended for a further two years and an extension to include support services to British embassies and consulates across Spain. The joint venture, Landmarc, was awarded a contract extension with the MOD worth £110M to manage military training facilities across their estate. The group are targeting healthcare as an area for growth and last year’s acquisition of Advantage Healthcare have enabled them to extend their service range into community healthcare. Going forward management expects the business to continue its strong progress with particular focus on the UK’s Defence Infrastructure Organisation as they are bidding on six new contracts, two of which they are incumbent.

International support service profits are still fairly minor but they increased by nearly 11% to £4.1M. The main business suffered from subdued market activity, competitive pressure and the re-tendering of the significant Ras Laffan contract in Qatar although performance has been better later on during the period. The profit levels were flattered by the contribution from the newly acquired businesses, although the Oman business was temporarily affected by deferred client expenditure at Mukhaizner. The group is making good progress with the integration of both TOCO and Topaz but there have been some delays on some work, pushing it out into 2014. Adyard, the renamed Topaz business won a contract worth £10.8M for the fabrication of an offshore platform for the Zora Field development on behalf of Dana Gas. Other new contracts included facilities management for Habib Bank in Dubai (already a long standing customer of the construction business) and for estate management services at the Monte Carlo Beach club in Abu Dhabi.

The UK construction business had profits that were fairly flat year on year, being less than 1% up on last year at £14.7M. During the year major infrastructure activity was subdued and the group undertook greater diversification to account for this. An example was the construction of Energy from Waste plants. The £146M scheme in Glasgow, on behalf of Viridor is now underway and the group also have a joint venture with Babcock and Wilcox to design and build another plant in Peterborough, a contract that is worth £15M. The group considerably extended their capabilities in the fit-out market by buying Paragon, a specialist refurb business based in London and have won contracts with HM Courts and Tribunal service so far. During the year various NHS framework projects were undertaken, including completions at Frome Medical Centre, Kettering General Hospital and Langdon Hospital in Dawlish with new awards including Mid-Cheshire Hospitals NHS trust and Hywel Dda Health board in Wales.

In education the group redeveloped the Charter Academy in Portsmouth and were confirmed as selected contractor in the Priority School Building Programme to deliver eight schools in the West Midlands. The group also completed a University Technical college next to the Silverstone race circuit. Towards the end of the year the group was awarded a place on the £250M DIO framework for the East Midlands and Eastern England region. This four year framework has the option of being extended for another three years and will be used to deliver a number of projects each valued at up to £12M. It is not just public sector work that Interserve has been picking up. They have a good relationship with Jaguar Land Rover and the group have started work on a new engine manufacturing centre near Wolverhampton. This was supplemented by two additional contracts awarded during the year and will provide work through to the end of 2014. Going forward, the board see some improvements in the UK for 2014.

International Construction profits fell by 8.4% to £13.1M. The market in the Middle East, where much of Interserve’s clients are based, experienced increased levels of competition and therefore lower margins were achieved. During the year the group won a £110M contract for the redevelopment, expansion and upgrading of the Mall of the Emirates in the UAE on behalf of their long standing client, Majid Al Futtaim. Market conditions in the UAE as a whole started to show signs of improvement and the group also secured work for the office of the Crown Prince of Dubai, EMAAR Boulevard restaurants, Chalhoub Group (retail), the government of Fujairah (roads) and Dubai Festival City (retail). In addition, they were awarded a contract from General Electric to construct the new engine maintenance centre in Dubai, a contract to carry out extensive fit out work for the Four Seasons Hotel and road and infrastructure work for Meraas.

In Qatar market conditions were more subdued but the group were awarded a contract for the construction of the Lusail Tower and civil engineering in connection with a new desalinisation plant at the Ras Abu Fontas power and water station. They were also awarded work by Siemens to provide civil and building works in the energy sector and by Doha Festival city for sire enabling, which may be a gateway to more contracts at that major development scheme. In Oman, work was completed for Daewoo on the Sur Independent Power Project, including civil engineering works on the largest seawater intake structure in the country. Further work was secured with a range of clients including HSBC, the Wave Muscat and Petroleum Development Oman. During the year the group exited their Indian business as they seemed unable to make it work. This incurred a loss on disposal of £5.1M. Going forward, the board see some early signs of recovery in UAE and Qatar and the group have broadened their range through joint ventures.

Profits in Equipment Services increased by more than 25% to £20.1M due to increased activity in global infrastructure markets. In anticipation of improved market conditions the group increased their capital expenditure here to facilitate growth, a trend that management expect to continue into 2014. There are also plans to expand into new territories such as Singapore, Kurdistan and Colombia and to also grow their presence in Chile, Panama, South Africa and the US. In the Middle East and Africa, performance was good as increased demand in Saudi Arabia in particular drove sales. For example the group supplied more than 15,000 tonnes of equipment to Roots Group for the expansion of the Grand Haram Mosque in Makah. In Oman, equipment was supplied for the construction of a technical college for armed forces in Muscat and for the new Salalah international airport. After restructuring last year, performance in South Africa also showed a big improvement.

In Australia, demand for equipment services weakened somewhat during the year reflecting the reigning back of a number of large natural resources projects. Elsewhere in Asia Pacific, there was an increase in demand with notable projects in the region including the application for the group’s Airodek system in a redevelopment programme for the Channel Court shopping centre in Hobart, Tasmania where the operational efficiencies of this system helped accelerate the project. In Hong Kong, growth was driven by increased government expenditure on major transport projects, on which the group supplied shoring equipment for the widening of the Tolo highway. They also provided equipment on a project to connect a new underground railway to the West Kowloon Terminus.

In the UK, the equipment services business performed well with much of the success down to providing a major formwork and falsework to a casino, hotel and cinema complex being built near Birmingham. Across the rest of Europe, the market remained slow and the group took steps to cut costs in Ireland and Spain to manage their cost base in those markets. In the US the construction market showed signs of growth which contributed to a much improved performance and the group extended their West coast operations around San Francisco and Los Angeles. In Chile the group supplied a large scale framework and shoring project to create walls and slabs for the new hydroelectric plant in Laja. Going forward, management see further improvement in the sector as the business improves margins and benefits from global economic trends. To support the expected growth they will be investing in their equipment fleet to facilitate further geographic expansion.

Investment profit was just £800K compared to £6.6M last year due to the transfer of much of the assets to the group’s pension scheme. Financial close was achieved on the Alder Hey Children’s NHS foundation trust project and phase of the Help for Heroes accommodation on the Armada PFI project in Plymouth was successfully integrated into the existing contract. Facilities at the St Helens Building Schools for the Future project became fully operational during the year. Group services costs were up by £1M on last year. This was due to an increase in investment in back office capabilities such as IT, training and communications and the group expect this level of investment to continue in the medium term.

Going forward, it seems that aggregate market conditions are improving. Management expect further progress in revenues and profit growth in 2014, along with the successful integration of a number of acquisitions offsetting slightly weaker near term performance in international construction. The group is somewhat exposed to currency changes with the Qatari Rial and the Australian Dollar the most important, so the current strong pound may have some adverse effects. In the last year the impact of currency changes led to a reduction in net assets of some £13M.

After the balance sheet end the group announced the proposed acquisition of Initial Facilities Services for £250M. In order to pay for the purchase, the group are issuing new shares representing 10% of the share capital to institutional investors. Going forward, the group are targeting both organic and further acquisitions and they seem bullish for 2014.

Overall then, this was a good update from Interserve, profits are up across most businesses with the exception of International Construction and there is a very good cash from operations, albeit it did not cover capital expenditure. The group is still fairly reliant on the public sector but there seems to be some work done on diversifying, which brings me on to the Initial acquisition. The client base of Initial is much more skewed to the private sector and it really does seem like a good fit. However, £250M is a lot of cash to spend on the business and the increased borrowings do bring somewhat increased risk. Net debt for the year stood at £38.6M in 2013, compared to a net cash position of £25.8M the year before reflecting continuing investments in acquisitions and capital expenditure. The dividends have increased each year over the last five years, with a further 5% increase this year. At the current share price they represent a 3.2% yield, rising to 3.4% next year. The underlying P/E ratio is 14.5, and according to consensus this will fall to an undemanding 12.5 in 2014. This seems pretty cheap to me and had I not recently purchased some shares I would probably be buying.

On the 12th May the group announced an extension and addition to the MOD support services contract to manage the National Training Estate, running until 2019 with an option to extend for a further five years. The contract is worth £322M and is one that the Interserve have been involved in since 2003. The new contract also includes over 30 extra sites and services include booking, accommodation, feeding and refuelling of the military units, along with office duties, site maintenance, catering, cleaning, vehicle maintenance, logistics and a range of specialist rural estate and land management services.

On the 13th May the group released a statement covering the first quarter of the year. They stated that conditions in most of their markets had improved, work winning during the period was good and the integration of Initial was making some early progress and was on-track. During the quarter, work was won with the Department for Education, Christie NHS Foundation, Foreign and Commonwealth office, Mercedez-Benz, CBRE, Haribo, Centre for Process Innovation, University of Birmingham, Scottish National Blood Transfusion Service and Southampton City Council, along with the National Training Estate contract mentioned above – still fairly skewed to the public sector but it is good to see a few private companies on that list too. Internationally, the group won contracts in Oman, UAE and Qatar including the Doha Festival Cit and the Al Jazeera News Network. Equipment services continued to show good growth with new projects including the Abu Dhabi International Airport and motorway upgrade works in the UK.

On the 9th July the group released a statement covering some board changes. Nick Salmon and Russell King will be joining as non-exec directors in 2014. Nick is the senior independent director at United Utilities and was previously CEO of Cookson from 2004 to 2012. Russell is the senior independent director at Aggreko, has been Chairman of GeoProMining and held various management roles in ICI and Anglo American. At the same time, non-executive director David Thorpe will retire to devote more time to his private equity roles after serving five and a half years as a director at Interserve. On the same day the group announced that trading in the first half of the year performance has been strong with further development of future workload. The integration of the acquired support services business is progressing as planned and following the completion of a $350M private placement loan note, they remain well placed to continue investment – that is quite a chunk of debt and I hope they don’t spend it all at once! I remain a holder.

On the 29th October the group announced that a partnership led by Interserve has been named as preferred bidder to provide probation and rehabilitation services in Manchester, Cheshire, Merseyside, West Yorkshire, Humberside, Lincolnshire and Hampshire as part of the Ministry of Justice’s Transforming Rehabilitation programme. The contract is expected to be worth about £600M over seven years and the other partners are Shelter, Addaction, P3 and 3SC. The partnership will take over the delivery of all probation and rehab services to low and medium risk offenders who are released after serving prison sentences of less than 12 months.