Havelock Europa has now released their full year results for the year ending 2013.

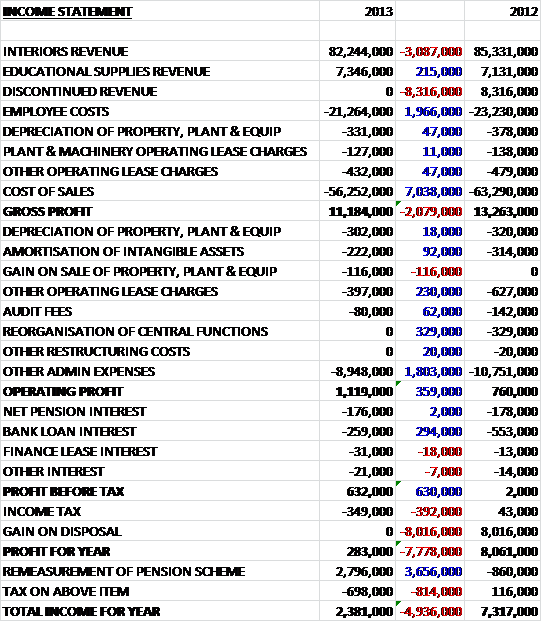

Revenues for the year fell when compared to 2012, driven by a £3.1M reduction in interiors (due to reduced fit-out business for education clients) and an 8.3M fall in discontinued revenue. Employee costs were nearly £2M lower than last year and cost of sales fell by £7M, presumably partially due to the disposal, so gross profits were only down by the tune of £2.1M. This was reversed by a decline in admin expenses, including the lack of £349K worth of reorganisation and restructuring costs which gave an operating profit some £359K higher at £1.1M. Financial costs were reduced due to lower interest costs on borrowings to give a profit before tax and the disposal of £632K compared to close to zero last year. A tax refund was reversed to a £349K tax charge so the profit for the year was £283K, lower by £7.8M due to the £8M gain on disposal of the Showcard business achieved last year.

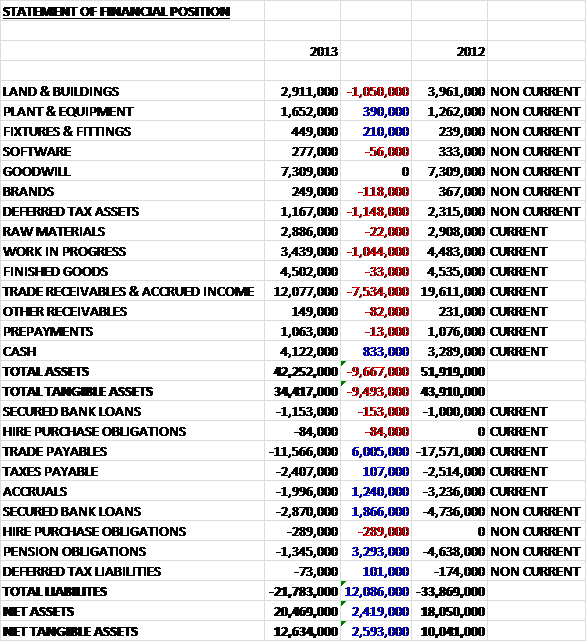

When compared to last year, total assets were down by nearly £10M. This was predominantly driven by a £7.5M fall in receivables, along with just over £1M less in the value of land/buildings, deferred tax assets (due to some losses being brought forward and put against this year’s tax bill) and inventories. The only major increase was a £833K hike in cash levels. Similarly, liabilities also fell during the year, down £12.1M driven by a £6M reduction in payables, a £3.3M fall in pension obligations due to a strong performance in the pension investments, a £1.9M fall in bank loans and a £1.2M reduction in accruals. This all meant that net tangible assets were some £2.6M higher at £12.6M, which seems a pretty decent outcome.

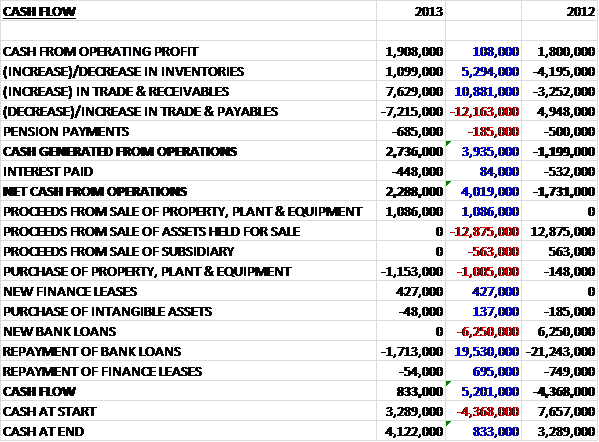

Before movements in working capital, cash profits were fairly flat on last year, up by just £100K. A favourable swing in inventory levels and receivables, however, meant that net cash generated from operations was up by some £4M to £2.3M despite a large decrease in payables due to shorter payment times, and significantly is now positive. We then see that the £1.1M gained from the sale of property, relating to Fontana House that previously housed the Showcard business, was spent on a £1.2M purchase of different plant and equipment, including the £700K purchase of new laser cutting equipment which has given rise to productivity improvements and represented a spend of £1M more than in 2012. The group then gained £427K from new finance leases before paying off £1.7M in bank loans which left the cash flow positive at 833K compared to an outflow of £4.4M last year. This looks pretty good actually, with a positive cash flow despite the repayment of loans.

The group made the vast majority of sales in the UK with only 6% coming from exports. They are very heavily reliant on one client, though, as Lloyds Banking makes up 38% of all revenue during the past year. Currently financial services overall make up 43% of their customers with retail making up 20% of revenue and education making up 37%. Going forward, the group are looking to diversify into healthcare and overseas retail to try and make up for a slight decline in the education market. Another risk is the banking covenants that the group still has to test against. A lot of progress has been made to reduce debt in recent years but EBITDA and EBIT to interest and cash performance are all tested quarterly.

Operating profit at the interiors division was £2.1M, up from just under £500K last year. During the year activity in the educational sector reduced as projects completed and new funding was put in place. This reduction in revenue was counteracted by an increase in financial services revenue, both from branch projects and work on offices – I would have thought a lot of this would have come from the LloydsTSB split and rebrand. Activity in the retail sector was flat and included the completion of projects for a major supermarket chain and out of town retailer, both of which were new areas of activity for the group. Overseas revenue grew and a contract to support the Far East activities of a major retailer was won. The increased profit from the division, despite lower revenues was due to increased efficiencies, including the acquisition of a new laser cutting machine. An investment was also made in new drawing office software that should further improve efficiency and provide benefits to customers going forward. The group are also looking to replace their ageing IT systems which in the long term should make them more efficient but would necessitate some capital expenditure.

Operating profit at the educational supplies division was down from £472K last year to just £258K in 2013. The reduction in Educational supplies profit was primarily due to Stage Systems. At Teacherboards, direct to school sales remained steady and there was good growth in web based sales. Both businesses work closely with the Interiors business and a lot of their work stems from that. After becoming the largest shareholder, Andrew Burgess has now got a place on the board and does seem to be driving some positive changes.

The group expect the improving UK economy to offer further opportunities for new business but the potential for destabilisation should Scotland gain independence should be considered considering the group is based there – it is something that management are keeping an eye on. As well as the improvement to the retail economy, the government has also made announcements for more education spending, which should filter through to new projects for the group by 2015 but next year work in the educational sector to reduce again. The reduced educational work volume should be taken up by new business wins in other areas and as long as the work with Lloyds continues, the more modern equipment the group invested in this year should give rise to further efficiencies next year.

Net debt at the end of the year stood at £300K, a big improvement on the £2.4M of debt at the end of last year. At the current share price the P/E ratio is a staggering 31.8 but the market is forecasting earnings growth for the group and next year this falls to a more normal 14.3. It still seems pretty high for what is still a bit of a risk though. Due to the slightly precarious nature of the profit levels the board have not proposed a dividend for this year which is probably prudent.

Overall then, this is a pretty decent update. I am particularly pleased to see further debt repayments and an increase in net tangible assets. The group do have a tendency in their reports to put a positive spin on things, however (there was no mention of falling profit in educational supplies in the write-up for example), so it can sometimes be forgotten than this is still a very tentative improvement. The markets Hevelock operate in are still difficulty and we already know that education volumes will be lower next year. Given the end of the Lloyds bank rebrand I would have thought it might be difficult to maintain financial service revenues too. I guess the question is whether the foray into healthcare and an improving market in retail can negate these issues. I am still holding the shares but as I am now finally breaking even I may consider an exit if there are any signs of problems.

On the 14th May the group announced that the Finance Director, Grant Findlay had resigned. Although this was unexpected for me, it clearly wasn’t for Havelock as they already have a replacement in Ciaran Kennedy who will join in mid-June. Previously Ciaran was operations director at Kier’s Scottish utilities business and was previously finance director at May Gurney before they were acquired by Kier. It always worries me when a finance director leaves unannounced but one could argue that Grant’s nine years in the role were not exactly successful and the new man looks to be a decent appointment.

On the 2nd June the group released a statement at the AGM and indicated that the first half is proving to be quiet, however, discussions with clients suggest that work may pick up in the second half. The group still expect education to be subdued this year but they have given a number of quotations for work starting in 2015 that they can hopefully convert into some new business. This update doesn’t say much but I find the tone a little worrying.

On the 23rd June the group announced that Ciaran Kennedy had started as Finance Director and Company Secretary as announced previously.