Tower resources have now released their results for the year end 2013.

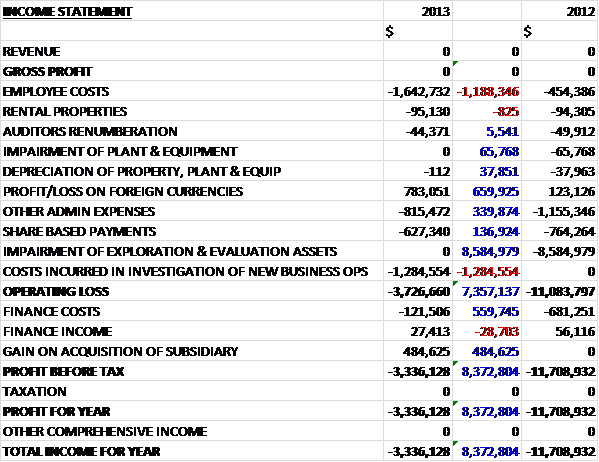

As the group makes no revenue there is no gross profit. Employee costs increased by nearly $1.2M, partly because $729K of these costs were capitalised as exploration and evaluation assets in 2012, and subsequently impaired. These costs now make up the largest expense and the only major one to increase over last year. There was the lack of a $66K impairment charge for equipment, and also a lack of a $8.6M impairment of exploration assets following the Ugandan dry well. Other reductions in costs were a fall in share based payments and other admin expenses. The group also benefited from a profit of $783K on foreign currencies. Finance cots were $560K lower, with the only cost being associated with the SEDA and related loan agreement with YA Global Master. Tower also made a $480K gain on the acquisition of a subsidiary so that the loss for the year was $3.3M, a whole $8.4M better than in 2012.

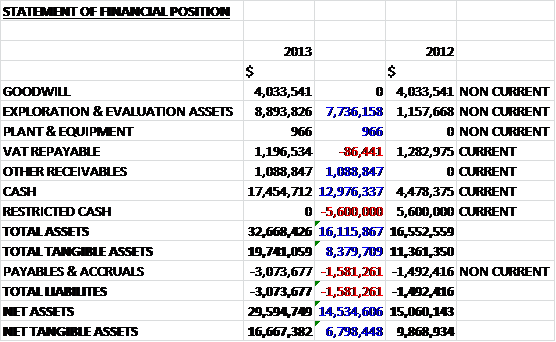

Overall, assets were up substantially over last year. The largest increase was a $13M hike in the cash level following successful share placings. The other substantial increases were a $7.7M increase in exploration and evaluation assets, relating to the Namibian licence, and a $1.1M growth in the value of receivables relating to the Ugandan VAT repayment, somewhat mitigated by the loss of $5.6M in restricted cash. The only liability was payables and accruals which increased by $1.6M, again related to withheld Ugandan tax. Overall then, net assets were up by $14.5M to $29.6M, mainly due to the cash that was received when the group made the placings.

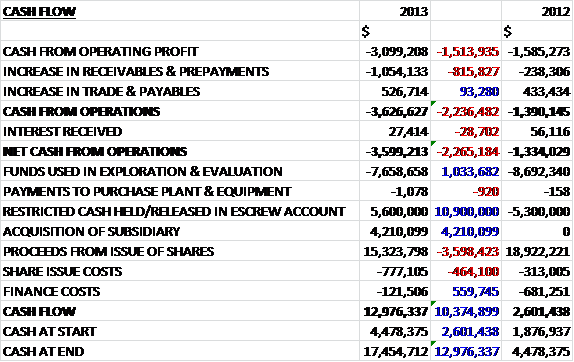

The cash outflow before movements in working capital was $3.1M, this was nearly double the outflow last year. An increase in receivables was somewhat counteracted by an increase in payables and the net cash outflow from operations was $3.6M, worse by the tune of $2.3M. The group did use about $1M less in exploration activities and the $5.6M of restricted cash was released into an escrew account. The group also benefited from a £4.2M cash inflow from the acquisition of Wilton Petroleum and received a net $14.5M from the issue of new shares, nearly $4M less than last year. Finance costs were kept under control, though, and the cash inflow for the year was just under $13M, some $10.4M more than in 2012.

As part of the Namibian licence there are a number of exploration commitments for the group. The second exploration period concludes on 22 August of this year with an optional third renewal exploration period up to 22 August 2016 which would require another exploration well to be drilled as part of the license. Drilling of the first exploration well has a budgeted net cost of $27M and other net license costs of $3M. As of the end of 2013 the group paid a total of £3M in cash towards these costs and since this date has so far paid another $3.4M. The cash balance of the group at the moment stands at $44M, so enough to cover the rest of the costs relating to the current drill. During the year as a whole there have been a lot of placings and the shares have become very diluted. Earlier in the year $13.9M was raised to pay for some of the Namibia costs and after the end of the balance sheet date the group raised another $32M via a second placing.

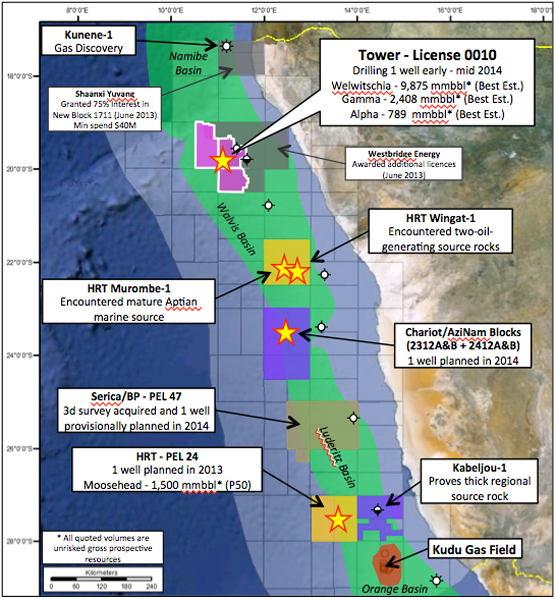

Clearly Namibia is the current focus for the group. The drillship arrived at the well site location in mid-March 2014 where it underwent tests before drilling commenced. Elsewhere in the country HRT drilled the Wingat-1 and Murombe-1 wells and although both failed to find commercial quantities of hydrocarbons, some oil was found at Wingat-1. Tullow Oil farmed in to Pancontinental’s license, PEL37 to the South East in the Walvis Basin and have subsequently undertaken 3D seismic, showing that industry interest in the country continues. The Welwitischia-1 well being drilled by Repsol in which Tower has a stake will target multiple reservoirs within a simple structural closure. The prospects extend from primary targets in the Maastrichtiean and Palaeocene to secondary targets in the Albian carbonate sequences. They are situated on a regional high and are the focus for migration and change from the proven source rocks within the Walvis Basin to the South and the Doplhin Graben to the East. The well is targeting net risked recoverable resources of 496mmboe and will intersect five different reservoir targets to a depth of 3000m. The best chance seems to be the Maastrichtian with a 31% chance of success, followed by the huge Palocean reservoir with a 19% chance. On completion of the Welwitschia-1 drill, there is considerable follow up potential with two new leads – Alpha and Gamma targeting another 91 mmboe risked and have a 12% and 9% chance of success respectively.

The group holds a 50% interest in the offshore Guelta and Imlili, and onshore Bojador blocks in the Western Sahara. Due to the sovereignty disputes with Morocco over the territory, there is little that can be done to advance exploration on these blocks but the cost of holding them is minimal so Tower is just sitting on them for now. Morocco has actually granted some licenses within the territory to Kosmos Energy who are planning a drill this year.

In April the group acquired a 15% interest in Block 2B in Kenya from Taipan Resources who retain a 30% stake and are the operators with the remainder of the interest owned by Premier Oil. Tower paid Taipan $4.5M in cash, 9M Tower shares and a contingent payment of $1M on spud of a second well. The total estimated mean gross unrisked prospective resources is 1,593 mmboe and the Badada-1 prospect is planned to be drilled during Q4 2014.

The group is currently in advanced negotiations with the government of Cameroon having submitted the preferred bid for 100% of the shallow water Dissoni Block in the most recent licencing round. The block is located offshore Cameroon and is the Eastern extension of the Niger Delta Basin. If the bid is eventually successful they expect a 3D seismic survey to take place in 2015. The block is close to current producing fields and next to the Glencore operated Oak discovery and there is also deep gas condensate potential here.

The group are looking to start negotiations on a new license in the Marovoay Block 2102 onshore Madagascar after presidential elections were held in December 2013. The block was relinquished by Ophir Energy and has multiple prospectivity in the Jurassic and Cretaceous sequences. Tower are also negotiating for two blocks (AB3 and AB6) in a frontier basin in Ethiopia after the El Kuran-3 discovery was made in 2013. The country as attracted other oil companies too, with Tullow due to drill this year nearby. The group are also interested in bidding in a new round of Ugandan licenses.

In October the group acquired Wilton Petroleum and with this acquisition came with cash to the tune of $4.3M after the cash used to pay for Wilton is taken into account. Granted the group also issued $2.6M worth of shares for the acquisition but there was still a $485K gain recorded. The other main acquisition, which occurred after the balance sheet date, was that of Rift Petroleum. The group purchased Rift in exchange for 550M Tower shares (50% of which are subject to a lock-in period of one year) , worth the equivalent of about $32M. The acquisition gave Tower exposure to a 50% interest in the Algoa-Gamtoos licence in South Africa, alongside New Age Energy. The block is between two others that have recently been farmed in by Exxon and Total and contains three prospective basins – Algoa, Gamtoos and Outeniqua. New 3D seismic is expected to be available by Q3 of this year whilst mapping of the 2D seismic is underway. A formal farm-out process for the license will resume once the 3D seismic has been interpreted. Rift also came with rights to acquire a 50% interest in any exploration right granted to New African Global Energy over the SW Orange Basin covering three blocks. Finally, there is also an 80% interest in two blocks onshore Zambia with a farm out here expected from late 2014.

These are interesting times for Tower. They are currently drilling the most important drill of their existence in Nambibia with a higher than 30% chance of success. They have also diversified into other regions, notably Kenya and South Africa. In order to do this, however, they have issued a lot of shares and they are far more diluted than at this time last year. At the end of the day this is still a bet on whether oil will be found in Nambia and I am happy with my small stake that I have here and will wait with baited breath for some news about the current drill.

On the 21st May the group announced that there had been a delay to the Namibia drilling schedule and that they do not expect operations to recommence until the end of the month. Following the spud of Welwitschia-1 and installation of the drill casing it was noticed that the wellhead housing had slumped and a decision to plug and abandon the well was made and to re-spud the well as Welwitschia-1A 50m away. This new spud occurred on the 1st May with no recurrence of the problem. A further operational delay was caused by a fault with part of the Blow Out Preventer (BOP) control system. Drilling has been suspended whilst Repsol, the operator and Rowan take measures to rectify the problem so that drilling can be continued safely which is likely to occur towards the end of the month. The well had been drilled to a depth of 1,879m and drilling into the primary target section should occur shortly after the restart of operations. Despite these delays, the well is still likely to be completed within budget. This delay is a little frustrating but apparently not uncommon with the use of new equipment as we have on the Rowan Renaissance. It sounds as though it is not likely to impact on the budget and has no bearing on the outcome of the well so not much has changed really.

On the 27th May the group released a corporate update. In Namibia, they expect the fault in the BOP control system to be resolved shortly and drilling should now recommence in the first week of June and be completed within budget. In Kenya, the group has received consent from Premier Energy regarding the 15% farm-in to the Block 2B in Kenya. Preparations for the first well, Badada-1, are underway with spud expected towards the end of 2014 or early 2015. In Zambia the group have met with the Ministry of Mines and Energy, the Zambian Environmental Management Agency and the Zambian Geological Survey Department and is now in the process of preparing for geological fieldwork in August 2014. In South Africa the processing and interpretation of 3D seismic acquired over the Algoa-Gamtoos license is currently underway and expected to be completed in Q3 2014. Total are to spud a well adjacent to this block in June which could give some clues as to the quality of this licence. In Cameroon, negotiations with the government over the preferred bid on the Dissoni block are continuing.

On the 3rd June the group announced the completion of its farm-in to block 2B onshore Kenya as mentioned previously. The recently acquired 2D seismic data is being used to determine the drilling location of the first well, Badada-1 which is expected to spud at the end of 2014 or early 2015. It will target gross mean unrisked prospective resources of 251 mmboe.

On the 4th June the group announced that Repsol had recommenced drilling on that morning.

On the 16th June the group released a statement that basically said the well was dry. The evaluations suggest that the Palaeocene, Maastrichtian and Upper Campanian section reservoirs were less well developed than thought and no hydrocarbons were encountered. Also, current expectations from the operator are that costs will now be around 10% higher than the gross budget, which is new news. The cost of continuing the well into the deeper targets would apparently added another $40M gross to the costs so the decision has been made to plug and abandon the well and study the current data to determine whether to drill a second well to test these deeper reservoirs. The group say that the prospectivity of the deeper section remains unchanged but reading between the lines I think the group will focus on some of its other licenses now. Damn. Worth a punt, but this time it hasn’t paid off (as was the likelyhood given the 35% cos.