Compass has now released their half year results for the year ending 2014.

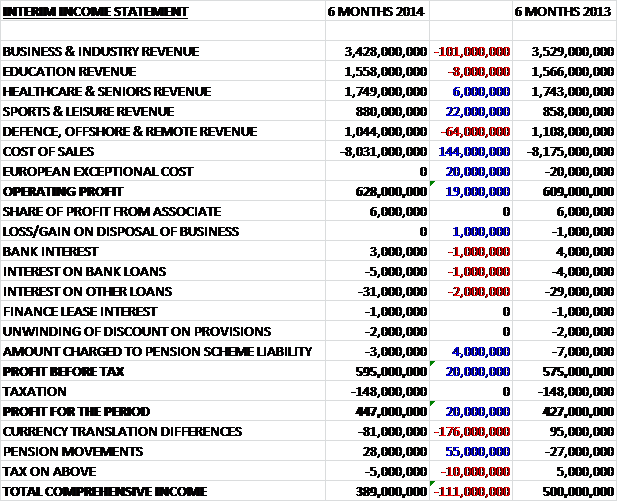

During the first half of the year there were varying fortunes for the revenues of each sector as a £101M fall in business & industry and a £64M decline in defence were partially mitigated by a £22M increase in sport & leisure with education and healthcare broadly flat. These revenues included the positive impact of Easter but were down by 1.6% overall entirely due to adverse currency movements. On a constant currency basis, they were actually up by 4.2%. This overall fall in revenue was more than counteracted by a £144M reduction in the cost of sales and the lack of a £20M exceptional cost. Overall then, operating profit increased by £19M during the period but underlying operating profit was down by £3M to £647M. There was not much in the way of changes in financial costs and taxation was exactly the same as last year so the profit for the half year finished £20M up on the same period of 2013 despite the negative currency issues and stood at £447M.

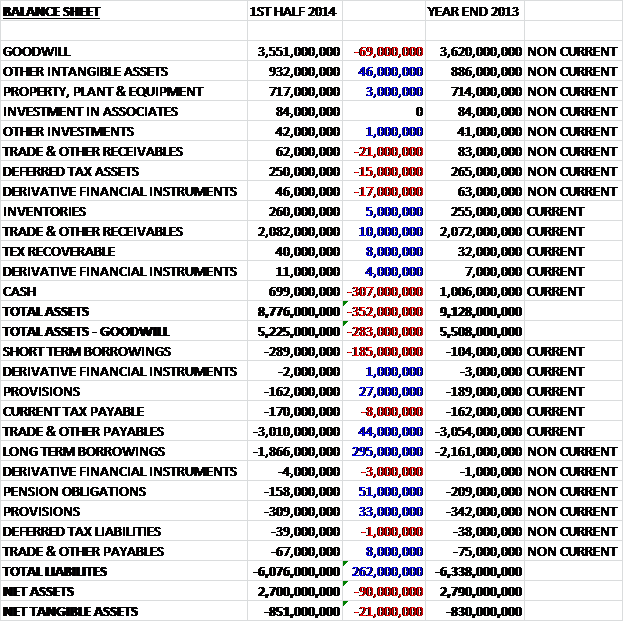

When compared to the end point of last year, asset levels at the end of the first half of the year were some £352M lower. This decrease was predominantly driven by a £307M fall in cash levels and a £69M decrease in goodwill. There were also a few substantial increases in assets with the largest being a £46M hike in other intangibles. Likewise, liabilities also fell, driven by a £110M fall in borrowings, a £51M decrease in pension obligations and a £60M reduction in provisions which all meant that, discounting the goodwill, net assets fell by £21M to -£851M which is actually not that great.

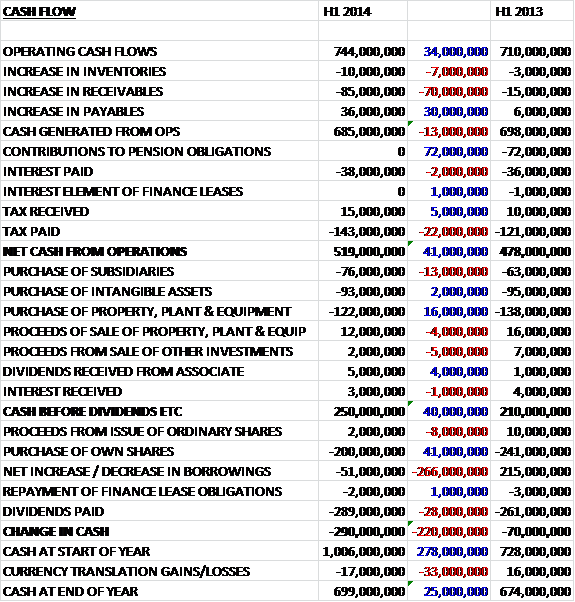

Before movements in working capital, the operating cash flow was up £34M on the first half of last year. An increase in receivables was not entirely mitigated by an increase in payables, due to the seasonality of the business, so the cash generated from operations was down by £13M at £685M. When compared to last year, there was the lack of a one-off £72M payment to the pension scheme, interest was flat at £38M and the group paid out £22M more in tax so the net cash from operations stood at £519M, up by £41M due to the pension payment the group paid last year. The group spent a bit more on the purchase of subsidiaries (£63M on infill acquisitions and £13M of previous contingent consideration) but a bit less on property, plant and equipment so the cash flow after investments was up by £40M. The group then spent £200M on share buybacks (£41M less than in the first half of last year), £289M on dividends ( £28M more than in the first half of 2013) and paid back a net £51M of borrowings, compared to the £215M receipt of new loans last time. Overall then, the cash outflow was £290M compared to an outflow of £70M in H1 2013. This is not bad when the share buy backs are stripped out but it seems that the current dividends are not quite sustainable long term on this cash flow and underlying free cash flow was down by £41M to £345M.

On a constant currency basis, organic revenues were up 6.6% in North America, driven by high levels of business wins across all sectors and some very good retention rates. Continued progress on operational efficiencies helped to deliver an 8% operating profit growth in the region. The business and industry sector grew well, underpinned by net new business and like for like revenue growth with new contract wins including L’Oreal, PDI Dreamworks, Nomura and Canada Post. There was good organic revenue in Healthcare and new business wins included food service contracts with the Baptist Memorial Hospital System, Yale New Haven Hospital and Jackson Madison County General Hospital, as well as the provision of laundry services to Sutter Health and Presence Health.

The Education sector saw good levels of new business, including additional support services contracts under the Texas A&M umbrella, as well as the Virginia Commonwealth University and food service contracts at Trent University and Montclair State University. There was also good organic growth in the Sports & Leisure sector with good new business wins and high attendance at sporting events. New contract wins here included the Indianapolis Motor Speedway and the FedEx Field, home to the Washington Redskins. The ESS business delivered good levels of organic growth with new contracts for Cliffs Natural Resources and the DeBeers Gahcho Kue Diamond project.

Overall, revenues in Europe and Japan were down but operating profit remained flat. Although economic conditions started to improve, like for like volumes remained negative during the first half of the year. Despite this there have been some good levels of new business in the UK, Ireland, France, Spain, Netherlands and the Nordics with underlying retention improving. The retention rate was affected by the planned exit of some of the more uneconomic contracts. Some new food service contracts included Continental and Societe Generale in France, Google in Ireland and the 2014 Ryder Cup in Scotland. New multi-service contracts included Shell in Germany and the Royal Navy in the UK. In Japan the group won a food service contract with Bosch and the Metropolitan Police Academy. In North and East Europe, volumes were broadly flat; in the UK, France, Germany and Japan volumes were slightly negative and in Southern Europe volumes were negative but at a reduced rate when compared to the second half of last year.

Despite reduced revenues in Emerging Markets, on a constant currency basis operating profit increased by £2M to £110M. During the second half of last year, a new management structure was bedded in throughout the region and the costs for this change flowed through to the first half of this year which management expect to largely reverse in the second half. Organic revenue growth in Australia slowed due to the slowdown in the offshore and remote sector which began towards the end of last year. Despite this, the group retained contracts with Conoco Phillips, AngloGold Ashanti and Melbourne Zoo. Outside Australia, emerging markets saw good double digit organic revenue growth due to strong levels of new business, particularly in China and India. In India, the group won new business with HN Hospitals and in China, with Nike. The UAE also delivered above average growth with new wins including the Cleveland Clinic and a food service contract at the New York University. Brazil and Turkey also performed strongly and new contracts in Brazil included Carrefour, Agropalma and Anglo American whilst Turkey saw new contracts for Med Star Memorial Hospital and BSH Logistic.

The board’s expectations for the second half of the year remain unchanged, notwithstanding the translation impact of the strong pound. The pipeline for new contracts is encouraging and the focus on efficiencies gives confidence going forward. If the current spot currency rates continued as they are the group would expect a negative currency impact of about £86M on full year underlying operating profit.

The group announced the appointment of a new non-executive director, Carol Arrowsmith who will become chairman of the remuneration committee. She is currently a partner in Deloitte and Vice Chairman of the UK business, although she is retiring at the end of the month. For many years she led the executive remuneration practice at Deloitte so she seems to be more than qualified for the role.

During the period the group completed the £400M share buyback programme and begun a new £500M scheme and they are now £95M through that new programme. Although the group plans to continue this scheme, it will be suspended until payment of the special dividend on 29th July and this programme is now expected to be completed in 2015. Compass is intending to distribute another £1Bn to shareholders in the form of a special dividend and share consolidation. The special dividend will be 56p and the share consolidation will turn every 17 shares into 16 new ones.

Overall then, this update was fairly decent if a bit mixed. The group is clearly suffering from the stronger sterling this year and there seems little prospect of a let up in that regard. We saw profits increase, but only because there was no European exceptional cost this year; net assets fell due to a decline in the cash levels and the operating cash flow was better last year only because of the payment to the pension scheme last year. Like many companies of this size, they do not seem to have enough operating cash for all the returns to investors. They do have a large cash pile but this will be completely driven down after the special dividend, which although nice, I don’t really see the business case for it. Trading looks likely to improve in the second half as they investment in emerging market management structure works its way through and Australia notwithstanding, that region does look exciting. Europe also seems to be slowly improving and North America remains strong.

Net debt at the six month point stood at £1.405BN, an increase from the £1.310BN at the same point of last year. The board announced an increase in the interim dividend to 8.8p, which, when combined with the final dividend gives an annual yield of 2.5% at the current share price but when combined with the special dividend, the yield is a very impressive 8%. Steady as she goes here really. I am happy to hold for the income and the safety at the moment.

On the 12th June the group confirmed that shareholders had approved the return of capital. The consolidation of the shares is expected to occur on the 7th July.

On the 30th July the group released a statement covering Q3 trading. Overall performance was good with organic revenue up 4%. North America experienced a strong performance with organic revenue up 6.5% with good levels of new business experienced. Margin also improved by about 10 basis points. The decline in organic revenue in Japan and Europe slowed somewhat and was down 1.2% compared to the same period of last year. The exit of poor contracts was largely finished during this quarter an although still negative, volumes showed some signs of improvement. Double digit organic revenue growth in emerging markets was counteracted by an acceleration in the slowdown of the Australian offshore and remote sector, resulting in organic revenue growth of 6.5%. The return of cash to shareholders has now been finished and the share buy back programme has been resumed. Sterling continued to strengthen during the quarter and should the current exchange rates continue through the final quarter there would be a negative translational currency impact of £92M on operating profits. Overall expectations remain positive and unchanged and the pipeline of new contracts is apparently pretty decent. Overall, this is a good update, currency challenges not withstanding and I am happy to hold.

On the 29th September the group released a trading update covering the final quarter of the year. There was another good performance with further strong growth in North American and Emerging markets along with an improvement in Europe and Japan. The full year saw a 4% organic revenue growth. In North America the strong organic revenue growth seen in the first half of the year accelerated in the second half with high levels of business wins and good retention rates. There was good growth in Healthcare and Sports & Leisure and the sales pipeline is good. Overall in the region, organic revenues are expected to be about 6.5% higher for the full year with a modest improvement in margins.

Conditions in Europe and Japan improved throughout the year and there was a healthy pipeline of work, reflecting the investments made in the sales teams. The contract exits previously announced have now been completed and volumes declined at a slower rate than in last year. Overall, sales are expected to fall by 1.5% but there is expected to be a decent margin growth. In Emerging markets there was a good organic revenue increase, expected to improve by 8% for the full year. Most countries in the region enjoyed strong levels of new business driven by an increased desire to outsource but as hinted at previously, there was a slowdown in the Australian offshore and remote sector. The profit margin benefited from the investments made at the end of last year and after reduced margins in the first half, an increase in the second half leaves them flat over the whole year.

The group has spent £115M on acquisitions over the year and received £23M following the disposal of a support services business in North America. The company has been battling a strong Sterling throughout the year and at the current spot price there is a negative affect of £1.176B on revenue and £89M on operating profit, the effect is in translation only. The outlook for the full year remains unchanged and going forward the improvement in Europe, the continued strengthening in North America and the margin improvement in Emerging markets points to a positive outlook, offset somewhat by the potential of continued sterling strength and a further slow down in the Australian business. I have topped up with a few more shares.