President have now released their full year results for the year ending 2013.

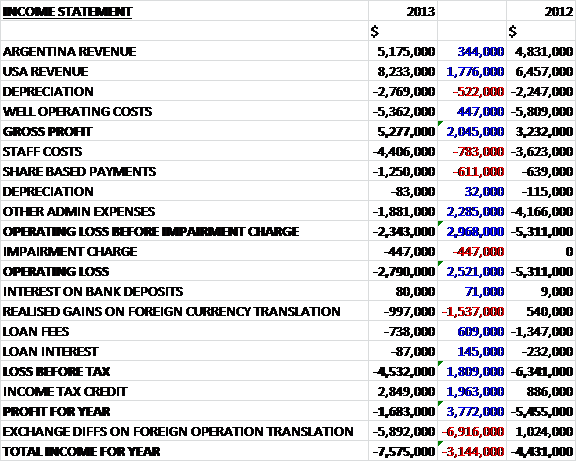

When compared to last year, revenues were up across both territories, with Argentinian sales up $300K and US sales increasing by $1.8M. An increase in depreciation was broadly counteracted by a fall in well operating costs, due to a reduction in the workover programme in Argentina, to give a gross profit some $2M higher than in 2012. Staff costs ticked up $800K and share based payments increased by $600K but these were counteracted by a $2.3M fall in other admin charges, due to the capitalisation of overhead costs following greater activity in Paraguay, and when a one-off impairment charge of $400K, relating to the relinquishment of the PEL132 license in Australia, is taken into account, the operating loss this year was $2.8M, some $2.5M better than the situation last year. Other costs included a loss on foreign translation of nearly $1M due to a weak Argentinian Peso and a loan fee of $700K (actually $600K lower than in 2012) before a $2M hike in tax credits meant that the loss for the year was just $1.7M compared to a loss of $5.4M last year.

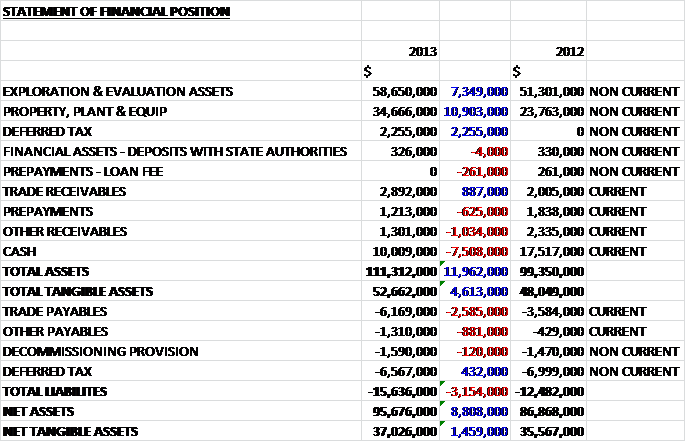

When compared to last year, total assets in 2013 were higher to the tune of $12M. This increase was predominantly due to a $7.3M increase in exploration assets, a $10.9M growth in the value of property, plant & equipment as $11M of intangible assets in Argentina were transferred there, and a $2.3M increase in deferred tax assets as the work programme extended the lives of the US fields which gave rise to a projected future profit that the deferred tax could be set against. These increases were partially mitigated by a $7.5M reduction in cash levels. Liabilities also increased, driven by a $2.6M hike in trade payables and a $900K increase in other payables, somewhat mitigated by a $432K decrease in tax liabilities due to the fall in the value of the Argentinian peso. Overall then, net assets of $95.7M were up by $8.8M but net tangible assets were up by just $1.5M to $37M. Of the intangible assets, $12.5M relate to the exploration assets in Australia which could end up being written off.

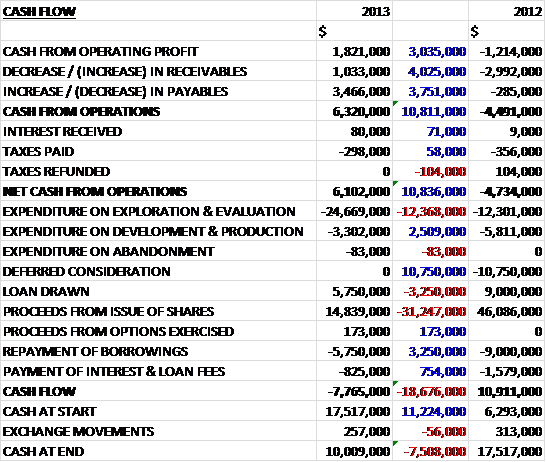

Before movements in working capital, the operating cash flow was $1.8M compared to an outflow of $1.2M last year. There was a decrease in receivables and an increase in payables which helped contribute to a cash inflow from operations of $6.3M, an improvement of £10.8M over 2012. The group then spent $24.7M on exploration and evaluation of the Paraguay asset and a further $3.3M on development and production. In order to pay for this, the group received $14.8M from the issue of new shares to the International Finance Corp which reduced the cash outflow to $7.8M for the year which left the group with $10M left in cash reserves – this is getting to the stage where President may have to think about raising some more cash.

Argentina is edging towards breaking even at the operating level, making a loss of just $462K compared to a $2.5M loss last year. During the year a well stimulation campaign was concluded, targeting two old wells and one current producing well. This campaign proved successful and at an oil price of $77 per barrel and $1M in stimulation costs, the carbonate and A6 intervals in Dos Puntitas and Pozo Escondido are commercial. Beam pumps have also been installed to increase production as the wells decline and average daily production rates increased by 7% over last year and oil prices held firm at $74 per barrel. It is thought that Argentina has the potential to deliver future production and reserve growth.

The US assets are the only ones that are profitable, making an operating profit of $4M this year, an improvement of $1.1M over 2012. Production was up 29% to 236 boepd with current production standing at 204 boepd. Oil prices remained strong and new exploration leads were identified. There is currently no production taking place in Australia but work continues to explore the potential of the PEL 82 license and the group has commissioned an independent geological consultancy to undertake seismic reprocessing of the existing 3D data. A report on their findings has indicated a new unconventional play in the block with significant prospective resource of 904 bcf. The license was then extended for a further year and now expires in September 2015.

Although Paraguay does not yet make any revenue, this is clearly where the group is targeting the majority of its exploration. They have now acquired both 3D and 2D seismic data and completed some geological and geophysical studies with a view to commencing the three exploration well drill in 2014. After the balance sheet date President were offered an 80% participating interest in the Hernandarias block in the Chaco region of Paraguay as operator. President will fund the first $17M of a work programme, including one well to be drilled to test the Devonian at any time within the next three years. The block is located immediately north of the existing Pirity and Demattei concessions.

The new seismic data identified two structural play fairways each containing two petroleum systems. The first is the Cretaceous petroleum system, identified from old 2D seismic data and it is an extention of the Palmar Largo trend in Argentina. The second is a newly identified Paleozoic petroleum system that has charged the large condensate producing fields in southern Bolivia and NW Argentina. In order to prepare for the drilling campaign, President has entered into a contract with Schlumberger for the provision of project management of the site and entered into a drilling contract with Queiroz Galvao Oleo e Gas, a Brazilian company with a view to spud the first well in May 2014.

An independent review of the prospective resources identified three areas that are estimated to have unrisked prospective resources of 1,093 mmboe with net risked for President of 647 mmboe and net risked prospective resources of 130 mmboe. These figures are based on the assumption that all eight prospects become discoveries and not the mean expectation for the drilling campaign.

So far, The International Finance Corp invested $24M in President shares and have a right to appoint a non-executive director. The funds from this investment are to be used for the 2014 Paraguay drilling campaign and to finance environmental and socially responsible operations. This is a good new shareholder with a lot of clout but may hold President to task over some of its demands.

During the year, the group appointed two new directors. Miles Biggins is the new Commercial Director. He is a petroleum engineer and worked for Shell for 15 years and then as Business Development Manager at Northern Petroleum. Dr. Richard Hubbard is the new Chief Operating Officer with 40 years’ experience in the E&P business and worked for BP as Chief Geologist and on the executive board for Statoil.

Going forward, the group is committed to funding a three year exploration programme on the Matorras and Ocultar license areas in Argentina at a cost of $2M each. After these three years are up, the group needs to decide whether to drill or drop the licenses. In Paraguay the group intends to drill up to three exploration wells in the Pirity Concession at an anticipated cost of $50M. Other items that occurred after the balance sheet date was the raising of $50.8M through the issue of new shares.

It does seem that President is making some progress with its concessions. Whilst a positive cash flow is still some way off, the US assets are profitable at the operating level and the Argentinian assets are creeping towards profitability following successful well rejuvenation programmes. The focus of the group this year, however, is Paraguay. There are three exploration wells targeting a huge potential reservoir. The performance of the shares both in the short term and longer term really does hinge on results here. Although clearly risky, I am happy to be invested for the ride.

On the 29th May the group announced that it has achieved its full participating interest in the Pirity Concession with the company now having a 59% interest. The drilling rig has now arrived at the Jacaranda well site, which is the first location for the programme. Rigging up is in progress and the well should spud within the next two weeks.

On the 10th June the group announced the acquisition of LCH, a Paraguayan company that held a 5% interest in the Pirity concession. As a result of the acquisition, President now owns a 64% interest. The group paid just over 10M shares with an aggregated value of $5M and further warrants over 4.3M shares with a value of $2.5M that can be exercised a price of 47p. Additionally, LCH had a potential right to a 5% interest in the Demattei concession and in the event that the right is granted, the LCH shareholders will receive further President shares with an aggregate value $4M.

On the 16th June the group announced the spudding of the Jacaranda 1 well. The well will drill multiple independent reservoir targets with total gross mean prospective resources of 624 mmboe. It will be drilled to a depth of 4,200m and is expected to take approximately 70 days to drill with a further update given when it has reached this depth.

On the 16th June the group announced the results of the audit of new significant prospective resources. This involves the Lapacho system, an independent, newly identified prospect. A third lower Devonian/Silurian petroleum system was identified basin-wide. To date some 11 large structural prospects and leads have been identified in the Santa Rosa play in the Pirity and Demattei concessions which offer giant gas condensate potential. Combined with the 25 prospects and leads identified previously in the shallower plays. There are now 36 potentially drillable features in the Pirity basin. The largest prospect is the Santa Rosa (otherwise known as Lapacho) with estimated gross mean unrisked prospective resources of 5.2 Tcf gas and 157 MMbbls condensate. Due to this, the group now anticipate the inclusion of a Lapacho x-1 well on the Pirity concession within the initial three well exploration programme. The Tapit x-1 well may also be deepened to test the Santa Rosa at that location. To make way for this new well, the group have postponed the Yacare well. Overall then, this is a very interesting new potential discovery.

On the 30th July the group announced the purchase of the 50% of Puesto Guardian Field not already owned by President. Puesto Guardian is located in the Noroeste Basin in NW Argentina. There are five fields in the concession, where maximum production of 9,000 bopd was reached in the early 1980s. President farmed into 50% of the concession in 2011 on a non-operated basis and it currently has gross production of 300 bopd at a price of $77.2 per barrel. The concession borders other exploration blocks owned by President. There are many shut in wells in the concession and a three well frac campaign demonstrated proof of concept that many historically shut in wells, properly worked over and stimulated could generate an increase in oil production and good payback.

The purchase came about because the other partner in the concession, Tripetrol Petroleum are looking to raise funds for other campaigns outside South America. The group will pay an initial $5M in cash from existing cash reserves with further cash payments of $880K due in 2015 and $1M due in 2016. The group have also agreed a waiver of long outstanding debt owed by the sellers of $1.6M and will pay a consulting fee of $20K a month for six months to effect a smooth transition. Additionally, should production attain 1,000 bbls/day, the group will pay royalties of 5% on proceeds, capped at $11M to the sellers. The current $84K a month operating fee that President pays will also cease.

This concession seems to have been somewhat neglected to date but this seems to be about to change now that President have taken over operations. They will spend the next few months considering the next steps, minimising costs and maximising profit with a new independent CPR due to be comissioned before the end of 2014. This seems to be a decent acquisition that has not cost much in cash. I guess the main driver on this was that the sellers were unable to make the investments needed so this is probably a good result. The timing does make me worry that there is some hedging going on just before the first Paraguay results are announced, however.

On the 13th August the group released the results of the Jacaranda well. The announcement certainly came with a lot of spin and unlike President, I am going to say it how it is from the off. It is disappointing that commercial levels of hydrocarbons were not found during the drill. There, not too hard to say I would have thought! Anyway, it is actually not all bad news. The well was drilled to a depth of 4500m, 300m deeper than planned and under budget. The well confirmed that the Devonian petroleum system of Bolivia and Argentina extends in the Pirity basin of Paraguay. Over 800m thickness of the source rock was found (it was still present at TD) which indicated that hydrocarbons were present at some point and maturity levels above 4200m are within the oil window and below this level they are in the gas condensate window.

The hydrocarbon shows comprised of Methane and Pentane which apparently indicated liquid hydrocarbons. The basic issue was the fact that the carboniferous sandstone was not sealed and hydrocarbons have migrated away. There is an indication that there may be reservoir sand below the Devonian source rock, only some 150m below the current TD. It is a little infuriating that the drill could not go that little bit extra to test it but the well have been suspended to allow deepening at a later date. The next target is now the Lapacho well which will target a discrete well defined fault block trap to target gas and condensate, and the well should be spudded before mid September. The Tapir well will be drilled after this one. This is certainly a disappointing result but it is only the first of three wells so I am still in for the duration.

On the 14th August, the group confirmed the farm in of the Hernandarias block in Paraguay. The concession is believed to contain the same Paleozoic play system that has been confirmed at Jacaranda . Three high graded prospect areas were identified from recently acquired and historic 2D seismic data. The structures are present at drill depths from 2000m downwards and well costs will be lower in this concession than in the Pirity concession. At this time, the group has acquired a 40% interest and will earn a further 40% upon fulfilment of the remaining commitment under a $17M work programme, which is defined to include seismic acquisition and one well over the next three years. So far, $1.6M has been spent with $15.4M remaining to be spent over the next three years. The sole partner in the concession is Hidrocarburos Chaco, a locally owned company.

On the 4th September the group released an update. The Lapacho well was spudded ahead of schedule on the 2nd September with the estimated time to target depth given as 70 days. Seismic data indicated the presence of a 400m section predicted to contain thick reservoir Santa Rosa Formation sands lying at a depth of 4,300m, immediately below the Devonian source rock. The greater Lapacho area is considered to contain gross mean unrisked resources of 5.2 Tcf and 157 mmbbls of condensate. The well itself will target gross mean unrisked resources estimated at 1Tcf of gas and 30 mmbbls of condensate.

The group also updated on the Jacaranda well. Having consulted independent experts, the view is that the Devonian rock formation encountered is most closely analogous to the Cretaceous Mancos formation in the US. This formation holds 100 to 140 Bcfe /Km2 in shale and associated formations. The Jacaranda area is now estimated to hold 20 to 28 Tcf gas in place in shale on the basis of the Mancos data. Mapping suggests this formation shallows to the North which may place it into the oil window. The group reckon that the potential for commercialisation of gas in Paraguay is good as there is no domestic production and incentive tariffs unique to Paraguay make the monetisaion of this type of resource tangible. I have decided to add a few more shares as they seem to have stabilised.

On the 11th September, the group announce that the Eagle Crest exploration well established a gross initial production in August of 492 bopd and 2,312 mcf of gas per day, a total of approximately 875 boepd. It is expected that the well will be brought on normalised production in the near future and additional exploration prospects at East Lake Verret and East White Lake are being evaluated. Prior to this well, Louisiana net production was running at 230 boepd. In Argentina with production at Puesto Guardian running at 300 bopd, the group is taking steps to rationalise the cost structure of the field and it is currently contributing $150K per month in cash to the group.