Photo Me has now released its final results for the year ending 2014.

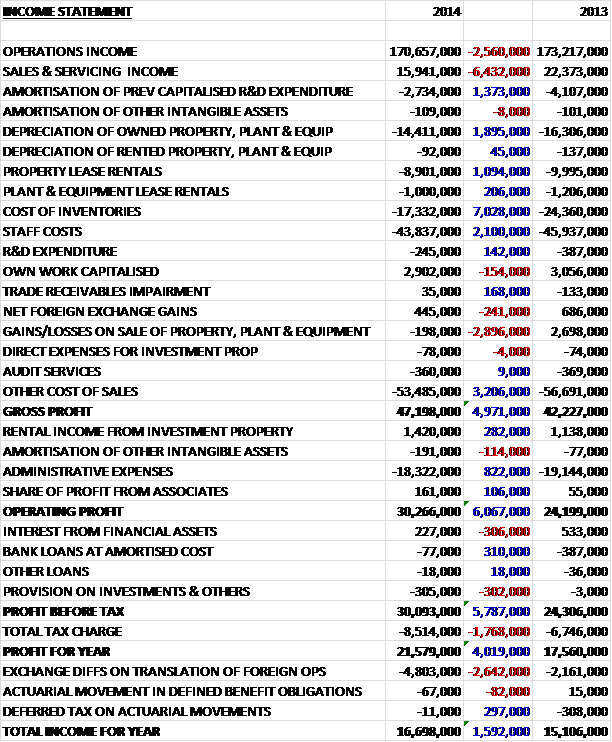

Compared to last year revenue was down across both business segments with operations revenue falling by £2.6M and Sales & Servicing revenue collapsing by £6.4M. The group benefited from a fall of £1.9M in depreciation of equipment when compared to 2013 and a £1.4M decline in the amortisation of capitalised R&D spend. Cost of Inventories also showed a good decline, falling by £7M to £17.3M and staff costs were also down slightly, falling by £2.1M. The group did not benefit from the £2.9M gained from the sale of the property that occurred last year but a further £3.2M fall in other cost of sales meant that gross profits were some £5M higher than in 2013. Due to a fall in admin expenses, operating profit looked even more healthy, up by £6.1M to £30.3M. A decrease in bank loan interest was broadly counteracted by a fall in interest from financial assets but £300K worth of provisions and a £1.8M hike in the tax bill took some toll on the profit for the year but despite this, it still finished up by £4M at £21.6M. A very decent performance.

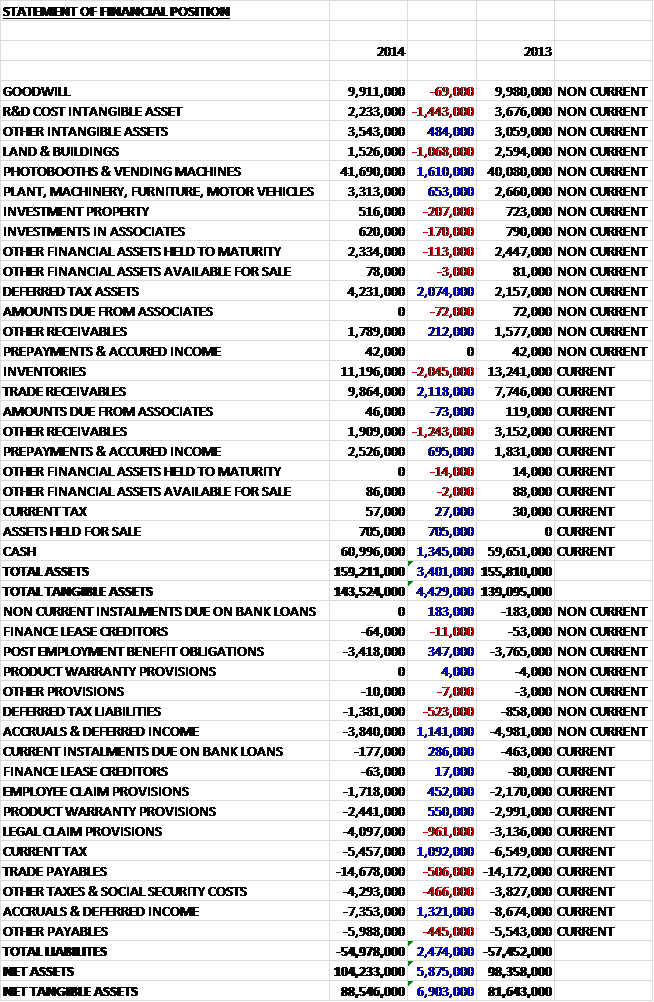

When compared to the end point of last year, assets were up £3.4M driven by a £2.1M increase in trade receivables, a £2.1M increase in deferred tax assets, a £1.6M hike in the value of the machines, a £1.4M growth in cash levels and £705K of assets held for sale relating to vacant land at the Bookham head office site. This is somewhat mitigated by lower inventories, capitalised R&D costs, buildings (relating to the lower value of the rental property after future rents were sold) and “other receivables”. £2.1M of the other intangible assets are “droit du bail” – payments in France for the right to occupy a space to site vending equipment. Liabilities fell during the year, driven by a £2.5M reduction in accruals & deferred income and smaller falls in the level of tax liabilities and both employee claims and product warranty provisions. These falls were mitigated by a near £1M increase in legal claim provisions and a half million pound increase in trade payables. Overall then the net tangible assets increased by £6.9M to a very healthy £88.5M.

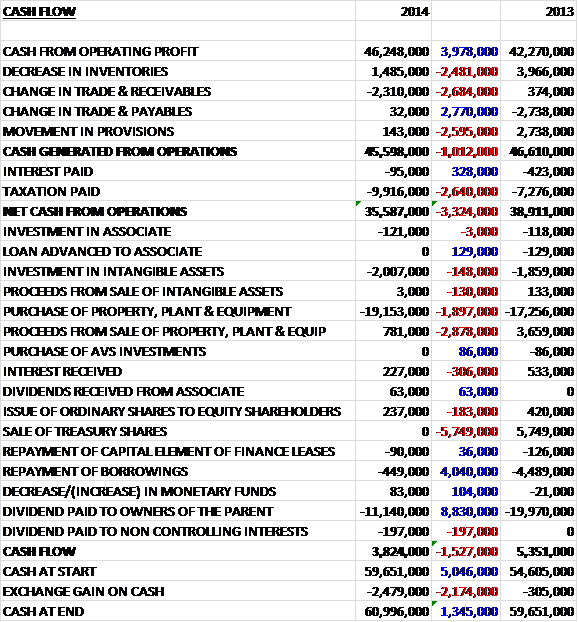

Before movements in working capital, cash profits were nearly £4M higher than last year. Movements in provisions and inventories, however, meant that cash generated from operations before tax was some £1M lower than in 2013. The group then paid more in tax and the net cash from operations came in at £35.6M, some £3.3M less than during last year. The bulk of this cash (£19M) was spent on plant and equipment, presumably new machines, and this spend was £1.9M more than last year. The group also earned £2.9M less from the sale of property, plant and equipment, presumably relating to the investment property rents sold last year. There was also the lack of £5.7M gained in 2013 from the sale of treasury shares. Now that borrowings are negligible, there is much less (£4M less than in 2013) spent on repaying loans and the group also spent £8.8M less on dividends. The result of all this is a positive cash flow of £3.8M, some £1.5M less than last year, mainly due to higher tax paid and movements in working capital. Not quite the stellar performance that occurred in 2013but this is still very impressive and it can be seen that both substantial capital expenditure and dividend payouts can be maintained using operational cash flow.

The group has capital commitments of £6.1M for the supply of property, plant and equipment but given the cash reserves, there is no issue of this not being met. The group has managed to sell land at the head office site valued at £705K for £4.2M which will be yet more cash to add to the hoard.

Photo-Me has been trialling heavy duty laundry units in France and Belgium sited predominantly outside supermarkets. The results from the trials from both a durability and takings standpoint were sufficiently good that an aggressive roll-out of the products has commenced in France and Belgium initially, with other European countries to follow. At the end of the year, the group has 519 units n field and following the relocation of the manufacturing capability to Hungary, the target is to have about 2,000 units in field by the end of 2015. The machines are very cash generative and have an EBITDA margin of about 50%.

Operating profit for the Operations segment was £30.7M, a £2.6M increase over last year. This division makes up the vast majority of group profits and the company benefited from the progressive rollout of the higher margin Starck booths, growth in the laundry estate and lower manufacturing costs. The overall estate grew as the removal of 553 low value amusement machines in the UK was counteracted by 1,260 new photobooths (mostly Starck), evenly split between the three geographic areas. In the UK the group obtained a contract to run machines located in Morrison supermarkets, which included 300 booths and there was a good performance in both Japan and France but Germany showed some weakness after a strong performance last year. Due to the lower manufacturing costs, the group is gradually expanding into new territories and operations have been established in Thailand, South Korea, Malaysia, Vietnam and Poland.

After the successful trial, the group now has laundry machines in France, Belgium, Ireland, Germany, Netherlands and the UK and as well as supermarkets, units are also present at campsites, universities, military barracks and riding stables. Digital printing kiosks are focused on Continental Europe, particularly in France and Switzerland. The market for printed photos is fairly mature but there continues to be innovation with regards to the products offered. There has been a continued reduction in the numbers of Amusement machines but the group has recently introduced some 4D experience rides to the estate and the business remains profitable.

Operating profit for the Sales & Servicing segment was £3.5M, a vast improvement on the £638K loss last year. Of this, £1.3M was from the sale of laundry units. The decline in revenue was due to the falling minilab sales, as was expected, and the lower staff costs, R&D costs and the previously mentioned laundry sales accounted for the increase seen in profits.

A lot of progress is being made on reducing costs. There is now a centralised logistics platform for the group which has led to savings from reduced stock levels and staff numbers. The focus going forward is on manufacturing costs with the use of new technology and low cost manufacturing bases. The cost of producing a photo booth has reduced dramatically in recent years, which has enabled the group to consider moving into some emerging markets. The Laundry units have now also been outsourced to Hungary which will give cost savings in future but did not occur until early 2014.

There are a number of ways that the group is looking for growth. They have a strong market position in their established countries and adding new units is quite difficult to achieve. However, as mentioned above, 300 new units have been added to Morrison supermarkets and a new contract has been negotiated to station photobooths within the London Underground network. Therefore the focus has to be on new markets. As well as the new countries mentioned above, China is still an immature market and the group now has 500 units in the country with a view to having 1,200 by the end of 2015 with an additional 200 in South Korea.

The group is also looking to increase prices cautiously to determine whether there is an impact on demand. A price rise as a result of a software upgrade has been affected in Japan and the group is targeting a price increase in one of the smaller European markets to determine the effect. I can’t help thinking this is a bit greedy. It would surely be less risk to expand into the new markets, rely on new products and reduce the manufacturing costs (all of which are being done) rather than to try and raise prices and risk killing the proverbial goose that lays these golden eggs.

The principal operating cost is the commission paid to owners of the sites where the machines are positioned. The commission paid on the laundry units is generally lower as they are usually stationed in outside areas and the rate over the whole estate is currently about 32%. This commission is an area the group is focusing on, along with logistics and manufacturing costs.

Net cash at the year end point was £63.1M, an increase of £1.7M on last year. This is certainly quite a substantial cash pile the group is sitting on. The total dividend for the year of 3.75p was a 25% increase over last year and the board are looking at another 30% increase next year with the possibility of special dividends too as the board issue a rather bullish outlook statement. The current yield is 4.1% but it looks as though this could rise in the coming year. The current P/E ratio is 24.6, falling to 21.2 next year. When the huge cash pile is considered, this actually seems fairly good value for a company of this calibre.

Overall then, this was a good set of results. Profits are up on slightly lower revenues, net assets are up and there was a strong cash flow, despite a slightly lower operational cash flow due to working capital movements and higher taxation. The yield is decent, with a very real possibility of further payouts; there is no debt and a huge cash pile. The shares are not massively cheap but I still see these as a decent buy. They are my largest holding at present, as situation that I am very comfortable with.

On the 12th September the group released an interim management statement. It was reported that the momentum seen last year has continued with an increase in profitability in the year to date in line with expectations. Profitability has improved across all geographic regions with Asia increasing profits by 50% and the UK and Europe both increasing profits by over 15%. At constant exchange rates, overall the group increased profits by 25% on a small increase in sales but the continued strength of Sterling reduced results by about 5%. The manufacturing facility in Hungary is working well and the expected increase in production remains on track. In France and Belgium, there was continued revenue increase for laundry machines sited for at least one year and results from the newly launched countries have been promising. The net cash position was £55M, a similar level to the same stage last year after payment of the special dividend. The board remain confident for the outlook for the full year. All good – if these were not my largest holding I would consider topping up.

On the 23rd October the group announced a statement covering the first five months of the year. They said that the positive trends announced in the last update had continued and on a constant currency basis, turnover has improved compared to the same period of last year and pre tax profits have moved ahead strongly so that the board are confident of the outlook for the full year. The Photobooth business is performing well with growth in all major geographic areas and a particularly strong performance in Japan. Progress with the rollout of the laundry units continued to go well and the total deployed is now over 700 units, more than 600 of which are located in France. The group is focused on deploying laundry units in 3 other countries and intends to expand to most of the other countries where they are already present. The financial performance of the laundry business has been strong and the cash position of the group remains very strong. All good, positive stuff.