Alumasc has now released their interim results for the year ending 2015.

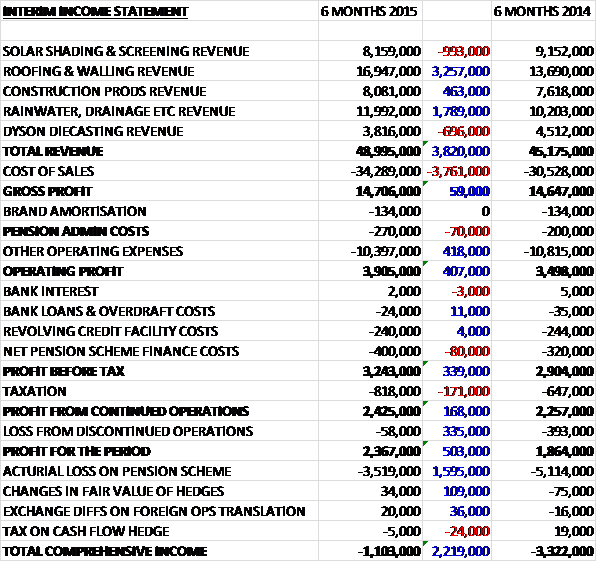

When compared to the first half of last year, total revenues increased by £3.8M driven predominantly by a £3.3M increase in Roofing & Walling revenue and a £1.8M increase in Rainwater, Drainage and House building products revenue. This was somewhat offset by a near £1M fall in Solar shading sales and a £696K decline in Dyson Diecasting turnover. Cost of sales also increased during the period to give a gross profit just £59K higher. Despite a small increase in pension admin costs, operating expenses fell during the period which meant that operating profit was some £407K higher. The total profit from continued operations was just £168K higher due to more pension costs and higher tax and once the loss from the discontinued operations is taken into account (less than last year as the profit on disposal of the Pendock business is include here) the total profit for the half year was £2.4M, an increase of half a million pounds when compared to the first six months of last year.

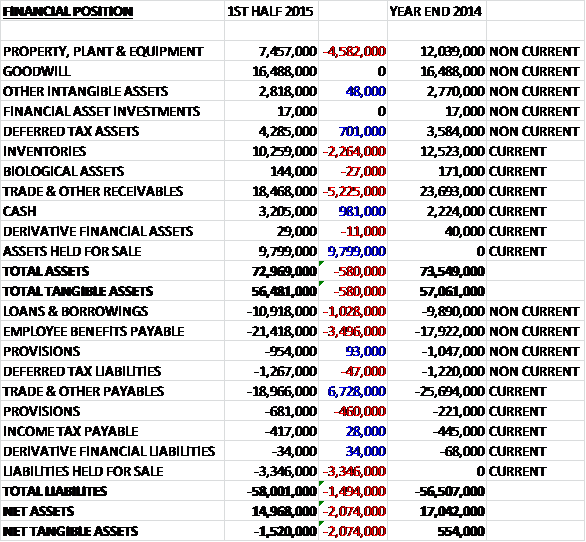

When compared to the end point of last year, assets were down by £580K as falls in property, plant & equipment, trade receivables and inventories were not entirely replaced by the increase in assets held for sale. Liabilities also increased during the year as a £6.7M fall in trade payables was more than offset by a £3.5M increase in pension payables due to a reduction in corporate bond yields, a £3.3M increase in liabilities held for sale and a £1M increase in borrowings. The end result was a net tangible asset based declining by £2.1M into negative territory at -£1.5M.

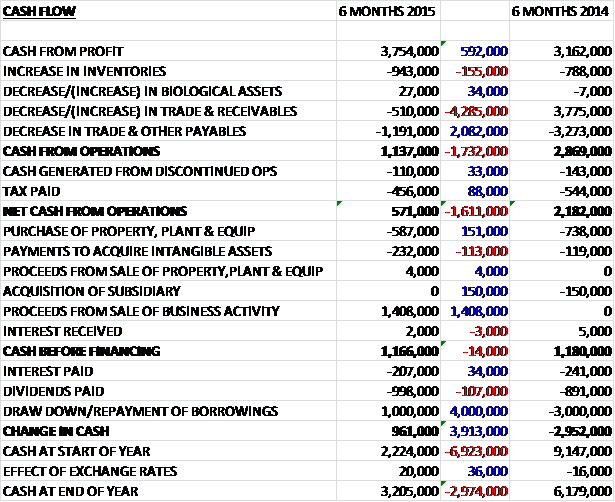

Before movements in working capital, cash profits were some £592K higher at £3.8M before this was somewhat eroded by an increase in receivables, an increase in inventories and a decrease in payables so that cash from operations was £1.1M, a decline of £1.7M on last year. After the cash outflow from the discontinued operations and tax was taken into account, the net cash from operations was down £1.6M at just £571K. All of this cash was spent on the purchase of property, plant and equipment but the £1.4M received from the sale of Pendock allowed the group to spend £232K on intangible assets, £998K on dividends and pay the £207K in interest payments. The resultant £961K of positive cash flow was due to the £1M drawdown of the banking facilities. The cash flow here is flattered by the sale of the subsidiary, without which there would be no cash to spend on dividends but if the group get a better grasp on working capital, this may improve for the second half.

Energy Management profits for the half year stood at £2.6M, an impressive £1.2M increase on the same period of last year. The increase was driven by Roofing & Walling profits which were £1.1M higher at £2.2M as actions taken over recent years to strengthen management and sales resources, introduce new products and expand the geographical range start to bear fruit against a backdrop of an improving UK market place. It’s worth noting that these strong results are despite the fact that the Kitimat smelter refurbishment contracts is now largely completed and only made a modest contribution during the year. In contrast Solar Shading and Screening struggled somewhat with profits declining by £58K to £386K. Enquiry levels and order intake has shown signs of improvement as the UK new build commercial property market starts to pick up in the South East of the UK but market activity remains some 30% below the pre-recession peak. Notable projects continued, including the large commercial building in London that is now near completion and the final project in Chiswick Park where the majority of work is now done. Steady progress was made in developing export markets with some success in North America but it does not sound like this will be enough to replace the completed large London projects.

Water Management and Other profits were down by about £300K at £2M. The decline was driven by the £326K fall in Construction Product profits to £556K as the business did not have any of the large individual projects in the UK that occurred last year. The multi-million dollar project at Doha port won last summer is under way and will also benefit the second half whilst the scaffolding business performed well, benefiting from both a broadening product range and routes to market. Rainwater, Drainage and house building products remained fairly flat, falling by just £38K to £1.4M on revenues that increased by 17%. The lower margin here was due to investments in new product development and in adding new capacity that gave rise to some additional costs.

Dyson Diecasting profits were £441K lower at £338K which was a solid performance given the fact that levels last year benefited from the initial stocking of some new product lines. At APC a modest trading loss was seen, an improvement on last year’s performance, due to the recovery actions taken but as announced previously one client decided not to renew a contract as certain engine variants were updated. As if this was not enough, the business also received some significant retrospective claims for alleged quality and delivery issues on the work that had come to an end and whilst some claims have been settled, the group remain in discussions to resolve the remaining matters. Provisions against the expected value of the settlement of the claims more than offset the improved trading performance, resulting in a £400K increase in APC operating losses to £1.1M. This loss was partially mitigated by the £800K gain on disposal of the Pendock business. The net asset level of APC on the balance sheet is £6.5M and management seem confident they can recoup this on any sale which would be a great result if achieved and really help with the cash flow and perhaps do something about the stubborn net debt levels. It could also be used to acquire other business and the board have stated they are seeking Building Products acquisitions to complement organic growth activities.

Traditionally the group tends to experience some bias towards the second half of the year with regards to profits but this is not expected to occur this year as some large construction projects are expected to make more of a significant impact in the first half. The order intake for building products increased by 30% to £48.9M, some of which will be scheduled for next year but at the half year point, the value of the order book was £19.2M, a similar level to the end of last year as billings of these larger projects during the year offset the general growth. The board expect to be able to grow the Building Products business both this year and beyond but I suspect the engineering products business is becoming more and more peripheral.

Net debt remained at the same level as the end of the year at £7.7M. The increased interim dividend of 2.5p, when added to the final dividend of 2.8p means the shares yield 4.1% at today’s share price which is expected to increase to 4.4% next year. Overall, I feel this is a bit of a mixed set of results. It seems that in general the group are seeing some good recovery in some areas but the fact that this year will not be skewed to the second half suggests that management are not expecting a stellar performance during the next six months. Also the continuing problems at the APC business, which can hopefully be offloaded and the fact that the group seem unable to make much of a cash profit, partly I guess due to the hefty pension deficit payments mean that I am finding it hard to invest here despite the positive market reaction to the update.

As we can see the price has been drifting somewhat and going nowhere since the end of last year but yesterday’s spike up may be the start of a run.

On the 13th February it was announced that CEO Paul Hooper purchased 17,861 shares for a total value of £24,000. This now gives him 104,643 shares and seems a good vote of confidence.

On the 25th February it was announced that AXA Investment Managers sold 25,000 shares with a value of about £37.4K. This is quite a small sale really as they still own just under 14% of the company.

On the 2nd April it was announced that non-executive director Jon Pither sold 16,000 shares which was worth just over £24K. This was apparently for tax reasons but director selling is never good to see in my opinion. He now owns 254,131 shares equal to about 0.7% of the company.

On the 26th of June the group announced that it had completed the sale of APC to the Shield Group for a cash consideration of £5.8M which is less than the net asset level of £6.5m that the board suggested they should be able to get for the business. The defined benefit pension obligations will be retained by Alumasc. Last year, APC generated an operating loss of £1.4M but the performance of the business did improve in the first half of this year. The expected one-off costs associated with exiting the business are expected to be about £2M, of which approximately £1.5M will be cash costs. The proceeds of the sale will be used to support the development of the group’s building products activities, including the relocation, modernisation and expansion of its rainwater and drainage business currently located on the same site as APC.

In addition, the group released a trading update where they stated that performance in the second half of the year was better than expected. The outlook continues to improve and the building products divisional order books currently stand at £23.7M compared to £19.2M at the half year point. The order intake in the current year has been over 20% ahead of the same period last year. This seems like a good update to me.

On reflection I have decided to take an initial position here. I am still a little concerned about the level of debt and the pension liability but trading seems to be picking up along with the UK commercial construction industry so the shared do look pretty cheap on a forward looking basis, that pension deficit notwithstanding.

On the 15th October it was announced that the group had won a significant project on the east coast of the US to design and supply a custom screening solution to a new gas fired power plant. The project is expected to generate about £3M of revenue for the group in the 2017 financial year. Levolux will provide an architectural screen around the plant’s two buildings to improve their visual impact on the surrounding area. The screen design is based on the patented “Infiniti System” of extruded horizontal aluminium aerofoil louvres fixed to each building through concealed fixings giving the louvres a seamless appearance. This contract demonstrates the ability to win contracts in the important North American market.

On the 22nd October the group released a trading statement at the AGM. They made a satisfactory start to the new year and demand from the group’s core UK construction market is apparently encouraging. The order book continues to rise and year to date revenues from continuing operations are marginally ahead of last year. They have seen some evidence that capacity constraints within the construction industry generally have caused delay to some projects. This will have an impact on timing but the board continue to believe that management’s expectations for their full year financial performance will be achieved. Cash performance remains strong and there is only a modest level of debt as a result. The market has taken this as a profit warning and I suppose it might be – it is notable that they expect to perform against their own expectations rather than market expectations so I might sell out here.