Arbuthnot Bank has now released their final results for the year ended 2016.

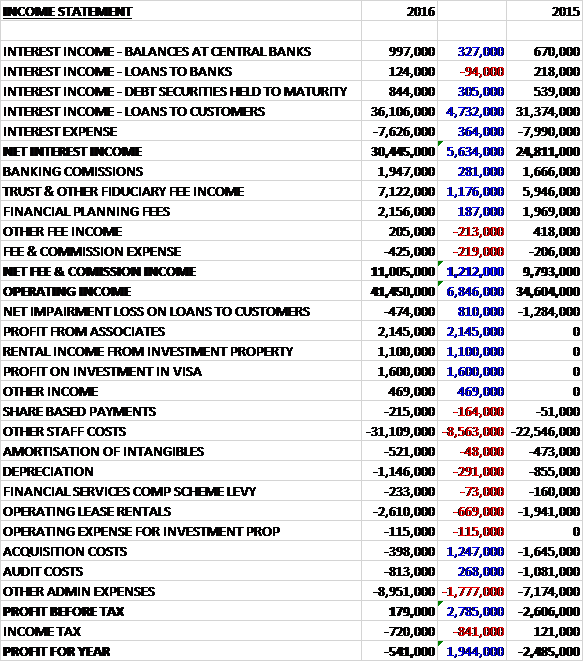

Interest revenues increased when compared to last year, mainly due to a growth in interest income on loans to customers. Net fee and commission income also grew with a £1.2M increase in trust and other fiduciary fee income which meant that the operating income grew by £6.8M. There was an £810K decrease in impairment losses on loans to customers but staff costs increased by £8.6M, including bonuses of £2.3M from the disposal of Everyday Loans, depreciation was up £291K, operating lease rentals increased by £669K and other admin expenses were up £1.8M. There were a couple of new profit streams, however. The first £2.1M in profits from associated was included this year as Secure Trust was mostly sold off, and there was a £1.1M rental income from the new investment property. We also see a one-off £1.6M of profit from the investment in Visa after Visa Inc purchased Visa Europe, and acquisition costs declined by £1.2M. After tax charges grew by £841K, there was a loss for the year of £541K, an improvement of £1.9M year on year.

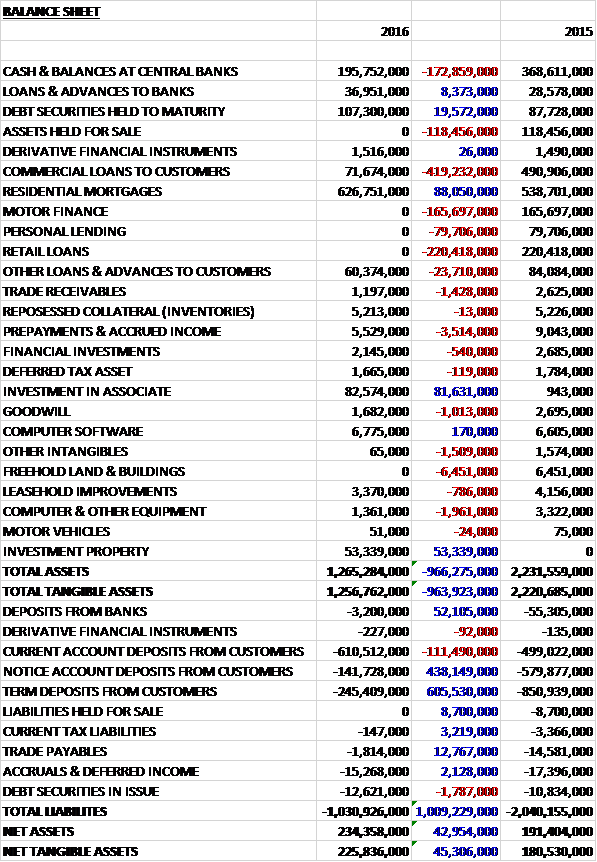

When compared to the end point of last year, total assets declined by £966.3BN mainly due to the sale of STB shares, driven by a £419.2M decrease in commercial loans to customers, a £220.4M reduction in retail loans, a £165.7M fall in motor finance, a £172.9M decline in cash at central banks and a £118.5M fall in assets held for sale, partially offset by an £88.1M increase in residential mortgages, an £81.6M increase in investment in the associate, relating to Secure Trust Bank, and a £53.3M new investment property. Total liabilities also declined during the year as a £111.5M increase in current account deposits from customers was more than offset by a £605.5M fall in term deposits from customers, a £438.1M decline in notice account deposits from customers and a £52.1M decrease in deposits from banks. The end result was a net tangible asset level of £225.8M, a growth of £45.3M year on year.

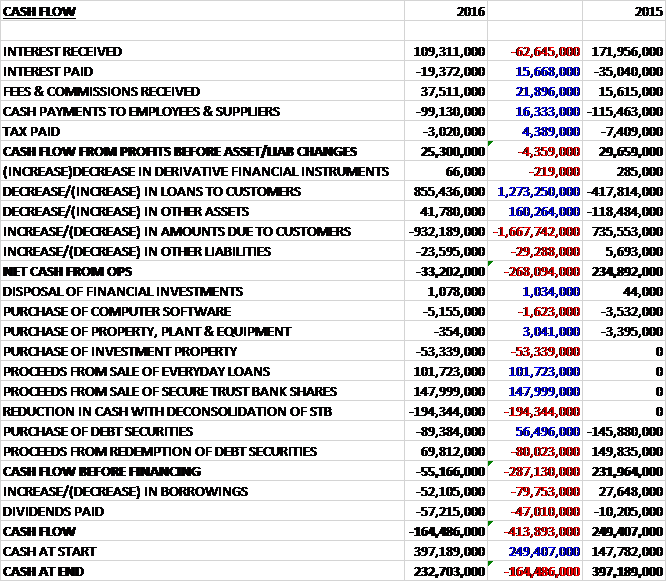

The interest received fall by £62.6M but the interest paid declined by £15.7M, fees and commissions received increased by £21.9M and cash payments to employees and suppliers fell by £16.3M so that after tax payments declined by £4.4M, the cash profit declined by just £4.4M. There was an £855.4M decrease in loans to customers and a £41.8M decline in other assets but the amounts due to customers decreased by £932.2M and other liabilities decreased by £23.6M to give a net operating cash outflow of £33.2M, a detrimental movement of £268.1M year on year. The group spent £5.2M on computer software, £53.3M on an investment property and £89.4M on the purchase of debt securities, although there was proceeds of £69.8M from the redemption of debt securities. There was also £101.7M in proceeds from the sale of Everyday Loans and £148M in proceeds from the sale of Secure Trust bank shares but also a £194.3M reduction in cash with the deconsolidation of Secure Trust. This all meant that before financing there was a cash outflow of £55.1M. There was a £52.1M decrease in borrowings and £57.2M paid out in dividends to give a cash flow of £164.5M and a cash level of £232.7M at the year-end.

It is quite difficult to determine an underlying profit position given the number of transactions that has taken place over the year but from a pre-tax profit of £179K, we can take of the £2.3M of bonuses relating to the sale of ELL, add on £1.7M for a full year associate income from STV; deduct £1.6M which related to the profit on the Visa investment and perhaps take of the £398K in acquisition costs, although this is a little less clear-cut if there is a policy of acquisitions going forward. If we are prudent and leave those costs in, the underlying profit from continuing operations was £2.6M, an increase of £360K using the same measures the prior year.

The profit received from Secure Trust Bank was £2.1M, a reduction of £17.5M year on year due to the sale of the shares. The profit received from the Private Bank was £8.8M, an increase of £2.7M when compared to last year. The Dubai office contributed £900K of this profit, an increase of £800K year on year. Customer loans increased by 29% during the year.

The bank has continued their plan to diversify into other areas of financial services and has taken steps to in developing their commercial banking proposition. Initially the coverage was aimed at London and the SE but this has now been extended to the SW and NW. The team in Manchester has recently moved into their new premises in the building previously occupied by the Bank of England with the team seeking to provide a service to mainly owner managed commercial clients. The commercial banking division has seen its lending balances grow to £76M with deposits reaching £51M. In addition the division also has a healthy pipeline of approved lending that should see it grow substantially in 2017.

The private bank has continued to develop as planned. The loan book grew by £64M to £683M and deposits were £947M, an increase of £50M. Despite the market turmoil during the year, the investment management business grew assets under management by 25% to close the year at £920M. The loan to value decreased by 1% to 45% but overall the loan book remained well secured.

In December 2016 the group completed the purchase of a private banking loan portfolio from Duncan Lawrie Ltd for a consideration of £42.7M. The portfolio was purchased at a 5% discount following the decision by Duncan Lawrie to close their banking operations.

In June the group acquired premises in the West End of London, comprising 22,450 sq. feet of office space and about 7,000 sq. feet of retail space for £53.3M. The property is held as a leasehold from the Crown Estate with a review every five years. The property is currently fully tenanted, generating annual income of £1.8M. It is accounted for as an investment property and this year it generated £1M in profits. The intention is to create a small suite of offices from where the private bankers would be able to meet clients in the West End out of part of the building.

The group have also reached an agreement with the shareholders of Renaissance Asset Finance to acquire their lending business. The business provides lending solutions mainly to high net worth individuals and businesses seeking to purchase assets and equipment with relatively short term financing arrangements. This will open up new distribution channels for the group. The loan portfolio currently stands at £55M. The first payment in cash is estimated to be around £2.1M, equal to net assets of the business on completion. The remaining three payments are performance related with the maximum amount payable limited to £6.5M.

In June 2016 the group received €1.3M in cash following Visa Inc’s acquisition of Visa Europe. As part of the deal, they also received preference shares in Visa Inc which have been valued at their future conversion value into Visa inc common stock. The board have assessed the fair value of this investment as £569K.

In December 2015, STB agreed the sale of its non-standard consumer lending business, ELL to Non Standard Finance for £106.9M in cash. The disposal completed in April and on completion there was a realised gain on disposal of £116.8M. In June 2016 the group sold 6 million shares in STB which reduced their holding from 52% to 19%. From this date they accounted for their remaining shareholding as an associate. The group received £150M for the sale and realised a profit on the sale of £100.2M. The other associate, Tarn Crag recorded a loss of £197K.

The chancellor announced the introduction of a corporation tax surcharge applicable to banking companies with effect from the start of 2016. This is levied at a rate of 8% on the profits of banking companies after taking into account an allowance of £25M. This will increase the group’s future tax charges accordingly.

Going forward the short term economic outlook remains uncertain. The US seems to be taking a significantly more protectionist stance on their economy and the UK has triggered Article 50 to begin the process of exiting the EU.

The group actually made a loss this year so looking at PE ratios is not an option but on next year’s consensus forecast the shares are trading on a PE ratio of 30.6. After an increase in the dividend the shares are yielding 2.2% which increases to 2.4% on next year’s forecast.

On the 4th May the group released a statement covering the first part of the year. The group has made a good start. Lending balances are more than 36% higher than the previous year and are 16% higher than at the year-end. Customer deposits have increased beyond £1BN for the first time and now stand at £1.1BN.

Overall then this has been an important year for the group as they divested Secure Trust Bank which became an associate. This has obviously affected the performance with operating cash flow, net assets and profits all down. On a like for like basis, the underlying profit increased, however. The remaining bank seems to be performing well with loans to customers increasing and the Dubai office starting to contribute meaningfully to results. The group seem to be using the proceeds of the share sale to diversify somewhat with the new office building and Renaissance Asset Finance being the latest acquisitions. This good performance comes at a price, however, with forward PE at 30.6 and a yield of 2.4%. This seems a little bit too expensive to me.