Ashley House has now released their final results for the year ended 2017.

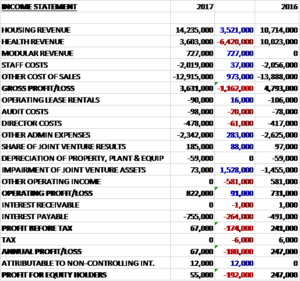

Revenues declined when compared to last year as a £3.5M growth in housing revenue and a £727K increase in modular revenue was more than offset by a £6.4M decrease in health revenue. Cost of sales also reduced but the gross profit was £1.2M lower. Admin expenses declined by £118K and there was an £88K growth in joint venture income. There was no impairment of the joint venture assets this time, which accounted for £1.5M last year but other operating income was down £581K to give an operating profit £91K higher. Interest payment grew by £264K, however, which meant that the profit for the year was £55K, a decline of £192K year on year.

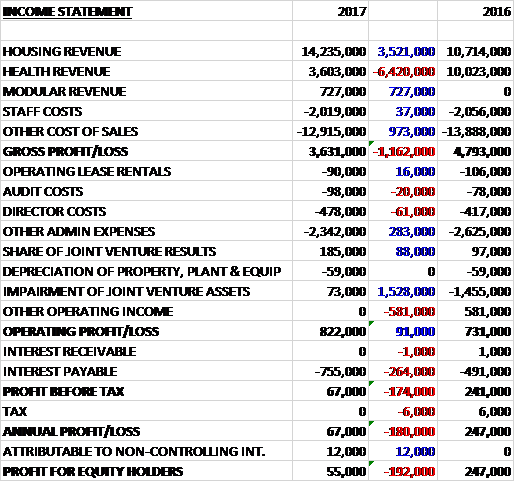

When compared to the end point of last year, total assets increased by £318K, driven by a £438K growth in retentions held on contracts, a £415K increase in goodwill, a £352K growth in the value of joint venture assets and a £317K increase in trade receivables, partially offset by a £1.3M decline in amounts recoverable on contracts and a £373K fall in amounts due from associates. Total liabilities also increased during the year as a £519K decline in accrued expenses and a £783K decrease in trade payables was more than offset by a £626K increase in the bank loan, a £444K growth in deferred income and a £307K increase in retentions held on contracts. The end result was a net tangible asset level of £3.3M, a decline of £558K year on year.

Before movements in working capital, cash profits declined by £1.6M to £818K. There was a cash inflow from working capital and after interest payments grew by £264K the net cash from operations came in at £241K, a growth of £166K year on year. The group spent £262K on joint venture shares, £157K on tangible fixed assets and £427K on an acquisition to give a cash outflow of £605K before financing. The group took out a net £626K of new loans which gave a cash flow for the year of £66K and a cash level of £89K at the year-end.

The last few months has seen the completion of two further extra care housing facilities in Harwich and Walton, both for Essex County Council. The group has continued to extend its housing pipeline although the delivery of these schemes continues to be delayed by the Government’s intention to restrict housing benefit to the LHA rate. The board believe a resolution to the issue of the cap is close but in the meantime they have been working with funders to create contractual structures that allow them to proceed with developments.

The two developments in Essex were funded by their partner, Funding Affordable Homes, and leased to the registered provider One Housing. The Harwich development consists of two buildings with a total of 70 one and two bedroomed apartments with communal facilities and Walton features 60 apartments with similar communal facilities. In the year the group also completed two developments for the charity HFT, one a block of seven flats for people with learning difficulties and the other a 12 bed unit for residents with dementia.

Despite the continuing difficulties with Government funding in the health segment, the group is currently on site with three health developments, including the diagnostic and treatment centre in Durham and two GP surgeries, in Swansea and Wivenhoe (Essex). All three projects are funded by Assura. In the year they also completed the refurbishment of lab facilities in Basildon Hospital.

The effective Government hold since late 2015 on funding extra care housing developments has restricted the group’s ability to reach financial close on many of their pipeline schemes but they have continued to grow the pipeline during the year including adding schemes such as care homes that are not dependent on the resolution of the LHA cap. The housing pipeline now stands at £197.9M across 23 schemes compared to £162.7M across 18 schemes last year. The health pipeline shows five schemes valued at £14.1M compared to £20.6M across ten schemes last year.

A significant development this year was the increased involvement in F1 Modular, and the acquisition by F1M in March this year of the assets of an experienced offsite manufacturer. The business is now a 76% subsidiary of the group with the remaining shares held by F1M management. It has a growing pipeline with places on local authority frameworks LHC1 and LHC3 and most recently obtained a place on the new ESFA schools framework. The business works in the private sector building retail units and housing although it is increasingly focussing on satisfying demand in the affordable housing and education sectors. F1M is currently in production with a pilot scheme of affordable houses in Banbury and social housing bungalows in Consett.

The current economic conditions create uncertainty over the level of new schemes required by social housing clients; the ability of the company to process its pipeline of extra care schemes due to the LHA rent cap; the level of new schemes required by the NHS; the contribution earned to cover the cost base; and the availability of corporate finance in the sector. The group’s ability to progress its significant pipeline of extra care housing schemes has been stymied since 2015 due to the LHA rent cap. The group has therefore developed relationships with specialist funders who are able to acquire extra care housing schemes on a forward-funding basis, ahead of the Government’s solution to the rent cap. The board expects these relationships to enable a number of their extra care housing schemes to progress to contract in the second half of the year.

Going forward, the first half of the New Year has to date been challenging with no schemes reaching financial close, but an agreement with new partners will mean a much improved outlook for the second half. The group are working to extend and widen their financing options to ensure they are able to continue to invest in their pipeline as new agreements are developed and the delivery of the pipeline is accelerated.

At the current share price the shares are trading on a PE ratio of 114.9 but this falls to 4.3 on next year’s consensus forecast. No dividend was paid or recommended. At the year-end the group had a net debt position of £2.5M compared to £2M at the end of last year.

On the 26th October the group announced that the Government is set to drop its plans to cap housing benefit in the supported living sector to LHA rates. This change should enable the group to unlock many schemes in its housing pipeline.

On the 24th November the group commented on this week’s budget and the move to increase funding for both health and housing property schemes. Within health, significant funding is being directed to Sustainability and Transformation Partnerships which, amongst other things will facilitate closer integration between health and social care. Within the housing sector, the government is committing increasing funding benefiting the group’s modular offsite offer as well as supported living.

The group has also noted the positive reaction by its funding and registered provider partners to the government dropping its plans to cap housing benefit in the supported living sector. Subject to there being no material changes in the forthcoming consultation process, the group is confident that their housing scheme pipeline can now progress.

They are targeting financial close on two housing schemes in the next few weeks. One is a traditional build and the other is modular with the start of the build phase expected in the early New Year. The group continues to look to extend and widen their financing options to enable them to grow, to further invest in their pipeline.

On the 15th December the group announced that they had signed a joint venture agreement with Morgan Sindall to develop extra care and supported living housing. They will transfer the majority of the pipeline schemes from their housing division to the joint venture, which Morgan Sindall paid £4M for a 50% interest. The group have already received £2M with a further £500K due in early January and the remaining £1.5M contingent on certain completion mechanics, expected in early 2018.

With the recent budget changes signalling a positive change of policy in this area, the board believes that the creation of the joint venture with accelerate delivery of their pipeline, providing a platform to grow the business to the benefit of both partners.

Other than two current housing schemes which are shortly due to reach financial close, all extra care, care and supported living pipeline schemes will become part of the joint venture and will then constitute the entirety of the group’s housing division. Following the transaction the group will continue to operate across three divisions. Its existing modular business and its health property development divisions are unaffected by the transaction. The group intends to apply the consideration received by the company in connection with the transaction to pursue their strategy and provide working capital to all of their activities.

Going forward the board expect the interim results to show a loss but they expect to be profitable for the full year. They consider that this joint venture agreement will enable them to de-risk a significant area of their business and build a stronger project pipeline.

On the 22nd December the group announced that director Maureen Moy sold 550.000 shares at a value of £72.6K. She remains interested in 4,600,000 shares.

Overall then this has been a difficult year for the group. Profits fell, net assets declined and although the operating cash flow improved, this was due to working capital movements and no free cash was generated. The first half results will be poor, with no schemes reaching financial close but the big news has been the lifting of the LHA cap and the joint venture with Morgan Sindall which really shows a way forward to monetise the impressing housing pipeline. The health pipeline is looking rather poor, however, but the group should be profitable for the full year. Indeed, the consensus forecast for the forward PE is just 4.3, suggesting the shares are good value if this comes to pass.

This is an interesting one, the near term half year results will be poor but further out things really seem to be more positive and I am wondering if this could be a good high-risk punt at these levels.