Paypoint has now released their interim results for the year ending 2018.

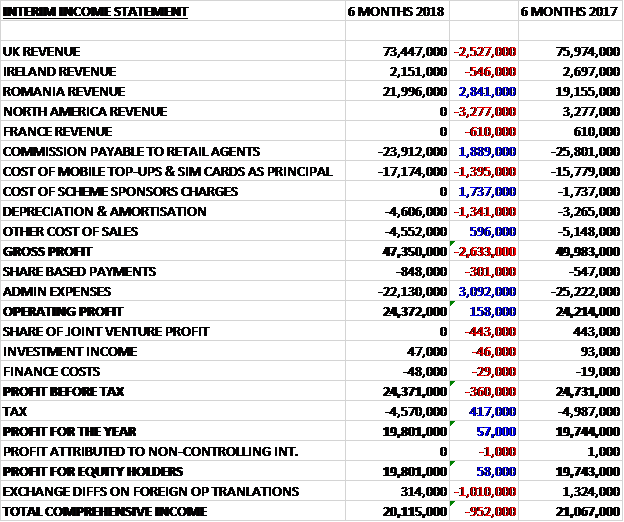

Overall revenues declined when compared to the first half of last year as a £2.8M growth in Romanian revenue was more than offset by a £2.5M decline in UK revenue, a £546K decrease in Irish revenue and the elimination of North American and French revenue. Commission payable reduced by £1.9M and there were no scheme sponsor charges, which accounted for £1.7M last time but the cost of mobile top ups increased by £1.4M and depreciation/amortisation was up £1.3M. After other cost of sales reduced by£596K the gross profit was down £2.6M. Share based payments were up £301K but other admin expenses fell by £3.1M due to the lack of mobile payment admin expenses to give an operating profit £158K higher. There was no share of joint venture profit, which was £443K last time and finance costs were slightly higher but a £417K decrease in tax charges meant that the profit for the period was £19.8M, a growth of £58K year on year. It is also worth noting that the discontinued Mobile business brought in £828K last time.

When compared to the end point of last year, total assets declined by £1.1M as a £20.6MK increase in receivables, a £1.9M growth in other intangible assets and a £1.7M increase in property, plant and equipment was more than offset by a £25.5M decrease in cash. Total liabilities increased during the period due to a £15.8M growth in payables. The end result was a net tangible asset level of £34.4M, a decline of £18.6M over the past six months.

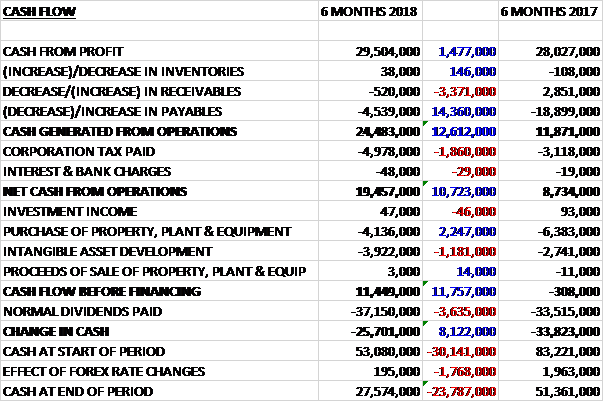

Before movements in working capital, cash profits increased by £1.5M to £29.5M. There was a cash outflow from working capital but this was nowhere near as much as last time and after a £1.9M increase in the amount of corporation tax paid, the net cash from operations was £19.5M, a growth of £10.7M year on year. Of this, £4.1M was spent on property, plant and equipment and £3.9M went on intangible assets to give a free cash flow of £11.4M. The group then paid out £37.2M in dividends to give a cash outflow of £25.7M in the half year and a cash level of £27.6M at the period-end.

Within Retail Networks, the total number of terminal sites grew by 2.2% as a 10.4% increase in Romanian sites was partially offset by a 0.8% decline in UK and Ireland sites. In the UK they introduced standardised service fees for legacy terminals across 14,000 sites and as a consequence saw a 1.9% reduction in the customer base.

Transactions across the retail networks declined by 2.9% with the UK declining by 5.3% and Romania up 6.6%. Transaction value was 2% lower than the prior period but net revenue was up 5%, driven by increased service revenue from Paypoint One. The impact of declining transactions was mitigated by improvements to client mix, renegotiation of symbol commissions, increased average top-up values and increased eMoney volumes which have a higher margin per transaction.

Bill and General transactions were down 6.2% with UK energy transactions falling by 9% due to the Big 6 energy providers losing market share, reduced levels of consumer energy debt, higher temperatures and the continued uncertainty around the impact of smart meters and the delays to their roll out. The MultiPay service performed well, however, doubling transactions in the period. Continued strong growth in Romania resulted in the addition of 14 new clients and the country saw volume growth of 6.2%. Net revenue decreased by 1% as the decline in transactions was mitigated by improvements to client mix.

Top-Up transactions reduced by 12.4% as a result of the continued decline in the UK mobile top-up volumes which was partly offset by an increase in UK eMoney top ups and Romanian top ups. Net revenue increased by 7.6% to £10.3M, despite transactions declining as a result of renegotiation of symbol commissions, increased average top-up values and increased eMoney volumes which have a higher margin per transaction.

Overall Retail Services transactions increased by 6.1%. Parcels volumes increased by 13.6%, card payment transactions increased by 5.5% and ATM transactions by 3.4%. Net revenue growth of 13% was greater than transaction growth, mainly as a result of strong growth from PayPoint One service fees, standardised service fees for legacy terminals, improved card payment margins and the change in VAT treatment in the second half of last year for card payments resulting in a benefit of £500K. These benefits were partially offset by the revised commercial terms with Yodel for parcels with an impact of £1.4M on a like for like basis.

Excluding the admin expenses from the mobile payments business last year, admin expenses grew by 8.3%. These higher costs relate to PaypointOne rollout, IT investment costs in relation to CRM, Paypoint One and data centre migration, people costs and irrecoverable VAT which increased by £300K due to the change in VAT treatment of card payments. The increase is weighted to the first half of the year and the board expect minimal growth in the second half as the investment required to deliver Paypoint One to their retailers decreases

After the period-end the group acquired Payzone SA in Romania for an initial consideration of £1.4M plus £400K in deferred consideration. Last year the business produced a pre-tax profit of £200K.

Going forward, the full year outlook remains in line with previous guidance. The group remain on target to achieve 8,000 PaypointOne sites by March. With the launch of EPoS Pro and the focus on increasing their pricing mix, they expect continued growth in the average weekly fee per site. They also plan to implement an option for retailers to have net settlement for card payments. In ATMs they intend to growth their network in the second half while also reviewing the implications from LINK’s recent proposals to reduce the interchange rate for their ATM business. ATMs remain an important business for them but they may adjust their network plans to remove sites that become unprofitable should the proposals to reduce interchange revenues go ahead.

In parcels, underlying trends remain favourable with increasing outlets and continued growth in UK online shopping. Following the restructure of the Collect+ joint venture with Yodel last year, the group now have the opportunity to extend their network to other carriers so they expect continued growth in parcel volumes with the addition of new carriers.

In UK bill payments and top-ups, the group will continue to add more clients to their MultiPay service and extend it to other sectors but there is uncertainty relating to the roll out of smart meters and the general long-term decline of cash and top-ups which will continue to impact the payments business. They hope to continue to renew key contracts with an improvement in revenue per transaction rates, however. In Romania the focus over the next six months will be to start network optimisation, integrating the business and to drive cost efficiencies following the Payzone acquisition.

At the current share price the shares are trading on a PE ratio of 14.6 which increases to 14.7 on the full year consensus forecast. After a 2% increase in the dividend the shares are yielding 5.7% which grows to 6.5% on the full year forecast.

Overall then this has been a solid period for the group. Profits were up due to the lower rate of tax, otherwise they would have been lower due to no contribution from the mobile business. Net assets declined as more capital was returned to shareholders but the operating cash flow improved with a decent amount of free cash flow being generated.

Romania continues to be strong but the UK is more mixed. Generally speaking revenues are holding up as a better product mix is offsetting lower transactions. Whether this can continue given the apparent structural decline in the UK top-up market and the generally lower use of cash is really the crux of the matter here. The forward PE of 14.7 is not very exciting given the lack of growth but the yield of 6.5% looks interesting. The dividend is not sustainable at this level but the shares could be worth a look. A tricky one this…

On the 15th January the group released a trading update covering the quarter to the end of December. Group like for like net revenue grew 3.6% to £31.8M. Actual net revenue declined 4.3%, however, as last year there was a one-off VAT recovery of £2.4M. The decline due to the VAT recovery was partly offset by strong growth in Paypoint One service fees and a strong performance in Romania. Group retail networks transaction volume reduced, as expected, by 1.7% due to lower UK bill and general volumes, partially offset by strong volume growth in Romania.

UK retail services net revenue decreased by 18% reflecting revised commercial terms with Yodel and the card payment VAT recovery. Card payment transactions grew by 3.4% and ATM transactions grew 1.4%. In light of the performance of some of their ATM sites and Link’s proposals to reduce the interchange rate, the group have started an initiative to reallocate a portion of their ATM estate to better performing locations. Collect+ Parcel service volumes declined by 3.1% as a result of reduced volumes in Yodel.

UK bill and general net revenue decreased by 3.3% as transaction volumes declined by 10.5%. This was driven by a 14% reduction in prepay energy volumes, offset somewhat by continued momentum in Multi Pay where transactions increased 80%. The strategy of pursuing an increased mix of smaller but higher yielding clients continues to perform well, partly offsetting the impact of reduced transactions. UK top up transactions declined by 16% as a result of UK prepaid mobile transactions reducing by 19%, partially offset by increased eMoney top-ups.

Romanian net revenue grew by 42%, mainly driven by the acquisition of Payzone in October with its integration progressing well.

Overall performance met the board’s expectations and the full year outlook remains in line with previous guidance.