Asian Citrus has now released its final results for the year ended 2015.

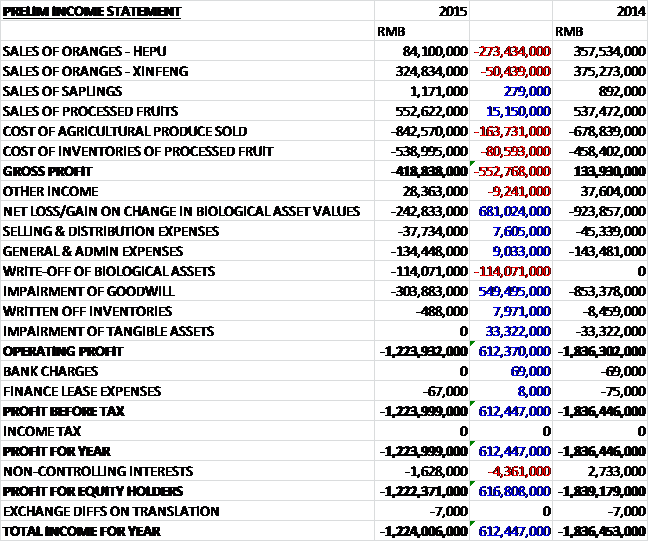

Overall revenues fell during the year as a £1.5M increase in the sales of processed fruit due to increased sales of red dates and medlar juice concentrate, frozen mango and tomato, and a small growth in the sales of saplings was more than offset by a £32.4M decline in the sales of oranges. The cost of agricultural produce sold increased by £16.4M reflecting the increase in consumption of both fertiliser and pesticides and the cost of inventories of processed fruit grew by £8.1M due to an increase in the cost of raw materials because of limited supplies, as well as increased labour costs, to give a gross loss of £41.9M, a negative swing of £55.3M. The decline in biological asset values was not as pronounced as last year but there was an £11.4M write-off of biological assets. The impairment of goodwill was less than last time though (the goodwill associated with the fruit processing business has now been fully impaired) and there was no impairment of intangible assets so that the loss for the year came in at £122.2M, an improvement of £61.7M year on year.

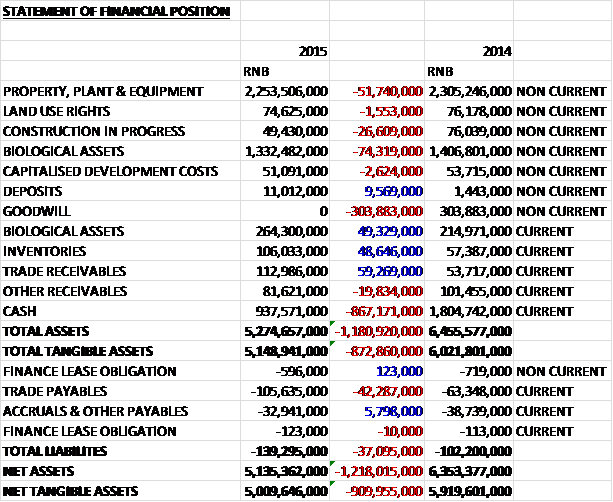

When compared to the end point of last year, total assets crashed by £118.1M driven by an £86.7M fall in cash levels, a £30.4M decline in the value of goodwill, a £2.5M fall in the value of biological assets, a £5.2M decrease in property, plant and equipment, a £2.7M fall in construction in progress and a £2M decline in other receivables, partially offset by a £5.9M increase in trade receivables and a £4.9M growth in inventories. Total liabilities increased during the period due to a £4.2M growth in trade payables. The end result is a net tangible asset level of £500M, a decline of £91M year on year.

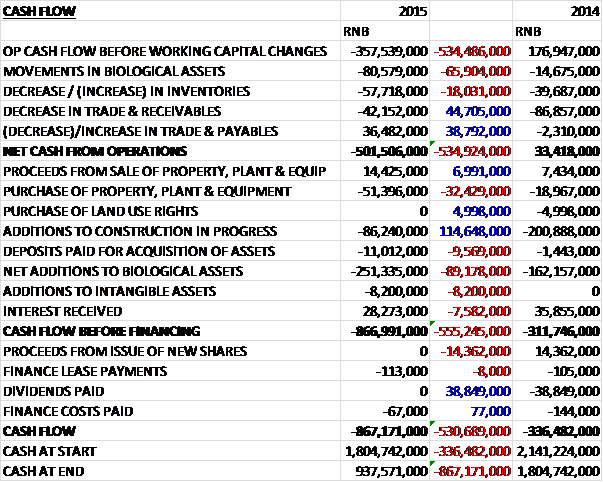

Before movements in working capital, cash losses came in at £35.8M, an adverse movement of £53.4M. We then see an increase in inventories and receivables so that the net cash outflow from operations was £50.2M, an adverse movement of £53.5M year on year. The group purchased a net £3.7M of property, plant equipment, spent £8.6M on construction in progress and £25.1M on biological assets so that the cash outflow before financing came in a £86.7M. There was little in the way of financing items so that the cash outflow for the year was £86.7M to give a cash level at the year-end of £93.8M – this is disappearing fast!

The loss at the agricultural produce business was £84.5M, an improvement of £11.1M year on year. The total orange production yield decreased by 34% to 130,125 tonnes due to extensive damage at Hepu from Typhoons Rammasun and Seagull; the effect of cryogenic freezing rain and frosts in Xinfeng and the effect of high temperatures and drought in Xinfeng area resulting in water scarcity for irrigation which affected the fruit size as well as production volume of the orange crop.

The loss at the processed fruits business was £4.8M compared to a £1.3M profit last year. Sales tonnage decreased marginally but the loss is mainly due to the increased costs of raw materials due to limited supplies, increased material scrap and maintenance costs caused by the low productivity of the production equipment, and increased labour costs. The group has decided to delay further investment in the third plant in Baise City due to deteriorating market conditions. Although it normally takes three to five years for a new plant to achieve full capacity, the group has decided to invest and improve the utilisation at the two current plants which are in full operation.

During the year 317,839 orange trees with a value of about £11.4M were removed due to the infection of Huanglongbing disease which indicated an infection rate of approximately 20% of trees in the Xinfeng plantation and some 2,563 trees were re-planted in June.

The production yield at Hepu fell by 64.6% to 26,278 tonnes due to the extensive damage suffered from the impact of the typhoons and in addition, the average selling price declined by 33.6% and costs increased as a result of the adverse weather. The average price achieved for the summer oranges was £362 per tonne and the average price for the winter oranges was £231 per tonne compared to £545 and £386 per tonne respectively which reflects both the extensive typhoon damage and the poor appearance of oranges infected by citrus canker. The plantation is now fully planted with 1.2 million orange trees. Also a total of 221,769 banana trees were naturally re-seeded from the original trees following the clearance of the damage caused by Typhoon Rammasun. The first crop of banana trees was harvested from July to September with 5,930 tonnes being sold at £314.6 per tonne – about £1.9M that will be recognised in next year’s sales.

The production yield at Xinfeng decreased by 15.7% to 103,847 tonnes owing to the effect of cryogenic freezing rain and frosts in Xinfeng in early 2014 and the effect of high temperature and drought during Q4 2014 which resulted in water scarcity for irrigation which adversely affected the fruit size as well as production volume of the winter orange crop. In addition, the spread of the Huanglongbing disease increased costs. The average price achieved for the winter oranges was £322 per tonne compared to £314 per tonne last year. The plantation now contains 1.3 million winter orange trees.

The construction of the Hunan plantation was completed after 26,960 grapefruit trees were planted during the year. Production at the plantation is scheduled to begin in 2016. The plantation consists of 1.05 million summer orange trees and about 750,000 grapefruit trees.

The group are apparently working on supply chain optimisation which includes methods to reduce costs of pesticides and fertilisers, exploring new export opportunities and changing the product mix in order to improve margins. Also, the group is conducting research on improving quality standards by means of larger citruses, and taste, which they hope should lead to premium pricing of their products in the market.

There is an interesting comment here from the auditor. They have noted that the group purchased fertilisers from a supplier who did not possess a valid business license (the value of this covered about 7.7% of total purchases for the year). The total value of the purchases was £10.4M and there is £2.5M in trade payables. The suppliers’ business registration is not currently included in the records of the state administration for industry and commerce of China. The auditors were unable to obtain sufficient evidence of the commercial substance of the transactions relating to the recorded purchases from the supplier because they were unable to obtain satisfactory documentary audit evidence to explain how the supplier was able to conduct the recorded transactions while not possessing a valid license, they were unable to satisfy themselves of the identity of the supplier and they were not able to determine whether the recorded purchases were free from misstatement.

This is potentially very important as I am sure I recall that a director, or perhaps previous director, had owned a fertiliser supplier and it seems to me that it is quite likely that cash has been syphoned off to this “supplier” under the cover that more fertiliser was required following the storms and various diseases that have befallen the group. It is also notable that by far the largest expense is the £42.4M spent on fertilizers which made up more than half of all cost of sales.

At the period end the group had capital commitments of about £4.4M mainly in relation to the construction of the farmland infrastructure in Hepu plantation and the acquisition of plant and machinery in the fruit processing business.

During the year Mr. Ng Cheuk Lun was appointed as an executive director, Mr. Ng Hoi Yue became an executive director, deputy CEO, after resigning as non-executive director, Mr. Ng Ong Nee was appointed chairman. There is going to be a bit of a cull in directors with CFO Ng Cheuk Lun (he didn’t last long) and executive directors Cheung Wai Sun and Pang Yi will step down after the AGM.

The group is loss making so there is no PE ratio and I cannot find a broker prediction for next year. There is also no dividend being paid – prudent given the cash burn no evident here.

Overall this past year has been a bit of a disaster for the group. The loss did improve but this was only due to lower impairments and the underlying loss increased. Net tangible assets declined year on year and the operating cash loss increased with the cash pile disappearing fast. The loss attributable to the processed fruits venture is disappointing with an increased cost of raw materials due to lower supplies along with a growth in labour costs taking their toll. The losses at the Hepu plantation were pretty catastrophic with the typhoons reducing yield to just 26,000 tonnes and the canker reducing the average selling price at the same time as costs increased. At Xinfeng things were little better with yields falling to 104,000 tonnes as the poor citrus trees here had to battle cryogenic freezing rain, drought, a heatwave and Huanglongbing disease.

Going forward, the Huanglongbing disease is likely to adversely affect the Xinfeng plantation but I would have thought things should improve at Hepu with the banana crop underway and Hunan where production of oranges should start in 2016 – although we haven’t yet had a plague of locusts so I guess that is always a worry. The dealings with the fertilizer company seem very dubious too – the auditor actually seems to have done its job and uncovered some potentially dodgy dealings with the fertilizer company that is not actually a fertilizer company – I wonder where that £10.4M has actually gone…

In all then, things should be getting better but with all the odd and stuff going on here, these shares seem pretty dangerous to me so I am steering clear.

Following the inexplicable jump up, the shares seem to be on a decline again now.

On the 18th December the group released an update covering the winter orange crop. The crop from the Hepu plantation, which was impacted by poor weather, will supply about 4,700 tonnes of oranges in H2 2015 compared to 7,146 tonnes last year. It is expected that the selling price will increase by 3%, however. The crop in the Xinfeng plantation was damaged by the outbreak of Huanglongbing. It is estimated that the production output for H2 will be about 11,000 tonnes compared to 103,847 tonnes last year and the outbreak is likely to have an adverse effect on the results for 2016 too. Reflecting these issues, it is expected that the selling price for the crop from Xinfeng will be about 24% lower this year.

As a result of the reduction in the production volumes at both plantations and the anticipated lower selling price at Xinfeng, the board estimates there will be a reduction in revenue and profit generated in 2016. Things are pretty desperate here and there seems no end in sight, I will be ending my coverage of this company until things start to turn around (I doubt they will, but you never know!)

I know I said I had written my last piece on this company but the latest bit of news is a peach. I might actually just keep an eye on Asian Citrus for entertainment value. On the 29th December (always a good time for stock market releases) the group informed the market that instead of the initial estimate of 18% of the Xinfeng trees being infected by Huanglongbing disease, the actual total is likely to end up being closer to 80%! Despite chucking a load of pesticide and fertilizer at the problem, the prevalence of the disease on surrounding plantations has meant they have been able to fight it and the whole Xingeng plantation is being permanently shut down. The board estimate that this will lead to an approximate £85M of asset write-downs.

They also helpfully reiterate that they are not covered by insurance and there will be no reimbursement of the losses. They also state that investors are advised to exercise caution when dealing in the shares of the company! I’d say, “investors” would have to be mad to buy any shares here. I actually can’t believe anyone would still own any stock as this company has become a laughing stock and is clearly on its last legs. I wonder if I can open up a short here?