Avon Rubber has now released its interim results for the year ending 2015.

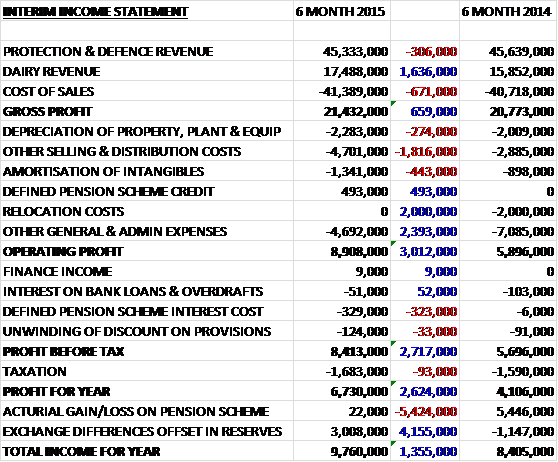

When compared to the first half of last year, revenues increased as a £1.6M growth in dairy sales was partially offset by a £306K fall in protection and defence revenue. Cost of sales increased slightly to give a gross profit some £659K ahead of last time. Distribution costs increased but admin costs fell during the year which included the lack of a £2M relocation cost that occurred last year and a £493K pension scheme credit this year to give an operating profit some £3M higher. We then see an increased interest cost on the pension scheme and a slightly increased tax bill to give a profit for the half year of £6.7M, an increase of £2.6M compared to the first half of 2014, although the underlying profit increased by a much smaller amount.

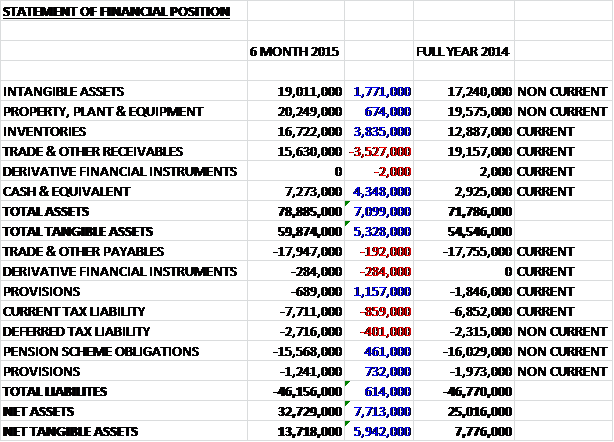

When compared to the end point of last year, total assets increased by £7.1M driven by a £3.8M growth in inventories, a £4.3M increase in cash levels and a £1.8M growth in intangible assets, partially offset by a £3.5M decline in receivables. Liabilities fell during the period as an £859K growth in current tax liabilities and a £401K increase in deferred tax was more than offset by a £1.9M fall in provisions due to the payment of £1.6M with regards to property obligations and £471K being paid with regards to facility location – the remaining provisions are all for property obligations. The end result is a £5.9M increase in net tangible assets to £13.7M – this looks to be a good performance.

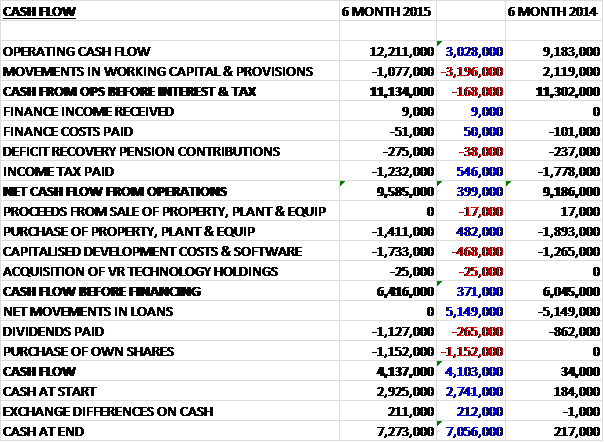

Before movements in working capital, cash profits were some £3M higher than during the first half of last year at £12.2M but adverse working capital movements meant that cash from operations fell by £168K to £11.1M. This was reversed by a decline in tax paid so that net cash from operations stood at £9.6M, a £399K increase. Of this cash, £1.7M was spent on development costs and £1.4M was used to acquire property, plant and equipment which led to a very healthy free cash flow of £6.4M, up by £371K. Roughly equal amounts of this cash was used to pay dividends and purchase their own shares to give an excellent six month cash flow of £4.1M that meant the cash pile at the period end was £7.3M.

Profit at the Protection & Defence division was £6.2M, a £1.5M increase when compared to the same period of last year, although it should be noted that this includes £2M of exceptional relocation costs relating to the Lawrenceville facility that occurred in 2014 and if these are removed, there was a £500K decline. The decrease arose from the mix of product shipped, being heavily DOD biased, whereas the comparable period had a heavy non-DOD weighting. The DOD contract enables the group to fulfil other orders as and when they arise and meet the DOD’s demand in periods when other orders are lower. The division benefited from cost savings following the consolidation of the US sites, increases in sales to Fire customers as the new Deltair product gained traction and AEF enjoying a successful period.

As touched on above, M50 respirator sales to the DOD were significantly higher than in the first half of last year, increasing from 58,000 to 112,000 systems. During the period a further order was received for 160,000 masks which means that there is good order coverage well into 2016. The group did not deliver any M61 filters during the period, compared to 162,000 pairs last time as a competitor qualified its filter and fulfilled its first order, which seems like a concerning development. In the long term, the board believe end user demand will grow but obtaining shore term visibility of future orders is challenging. Having said that, some further filter requirements are expected in the second half of the year. Last year included the delivery of the 52,000 C50 order but sales to foreign military, law enforcement and first responder customers reduced year on year but there has been a decent level of enquiries for the respiration protection products and the pipeline of individually smaller sales opportunities has grown with the group poised to deliver a richer mix of sales in the second half of the year.

There was a strong growth in sales to the North American Fire market following the release of the new Deltair SCBA. The product is designed to meet new US regulations and to deliver enhanced operational performance and it has been well received by the market and remains one of only four units to receive approval to date. The number of enquiries has given the group confidence that the product can continue to enhance its market share further. Other DOD spares sales were lower than in the same period of last year reflecting the timings of orders and delivery schedules. Order intake has been positive and higher levels of revenue in this area are expected in the second half of the year. The industrial escape product, launched in 2014, was well received in oil and gas markets and AEF saw a continuation of the high level of order intake experienced last year. In total, the order intake during the first half in the division totalled £47M and at the period end, the closing order book stood at £38M.

The funded development programme with the US Air Force to design and test the MM53 Joint Service Aircrew Mask progressed well with the prototype product passing the customer’s design review during the period. The customer expects the production phase of the programme to commence in 2017. The Emergency Escape Breathing Device received NIOSH approval in late 2014 and the group expects to hear from the US Navy with regards to an order in the second half of the year.

Profit at the Dairy division was £3.3M, a £600K increase when compared to the first half of last year. The group grew in all of its markets, supplemented by the positive translation effect of the stronger US dollar with an increasing proportion of higher margin Milkrite sales also contributing to the increased profit. Globally, milk prices have remained at acceptable levels and farmer input costs have been favourable meaning that there has been less pressure on farmer revenues and margins and therefore normal levels of demand for the consumable products. In Europe, Milkrite’s market share increased as a result of the increased sales force, enhanced technical support and larger distribution network. The Impulse Air mouthpiece vented liner continued to gain traction with its market share increasing from 2.6% to 3% over the past six months.

In the US, the Milkrite Impulse Air mouthpiece vented liner continued to perform well, with its market share increasing from 21% to 22% during the period. The Cluster Exchange Service was launched in the US and Europe in 2014 and growth rates are exceeding expectations. By the end of the period, it was servicing 342,000 cows on 1,100 farms. The service enhances the value of each direct liner sale made and should lead to a more robust and sustainable business model. In China, year on year revenue grew strongly against a weak comparator period. In many other emerging markets, including Brazil and India, the number of dairy cows being milked using automated milking processes is growing rapidly which is adding to the market potential for the products sold. A distribution centre was opened in Brazil during the period to serve the South American market with the first sale being made late during the period and the start-up is expected to make a positive contribution to profit by 2017.

Trading is normally weighted to the second half and it is believed that this will be the case this year. There is a strong forward order book in Protection and Defence and it is expected that the momentum in Dairy will continue. The board therefore expects to meet market expectations for the full year.

After a 30% increase in the interim dividend, the shares are currently yielding just 0.8%, increasing to 1% on the consensus forecast for the full year. There is a net cash position of £7.3M, a good increase when compared to the £5.5M of net debt at the end of last year and a £2.9M increase when compared to the end point of last year. There is also plenty of headroom with £26.5M of undrawn bank facilities available.

Also today the group announces that after fifteen years at the company, the last seven of which were as CEO, Peter Slabbert is stepping down from his role and is leaving Avon Rubber on the 30th September. He is apparently leaving for a change in lifestyle but this is a bit of a blow as he has no doubt been an exceptional CEO.

Overall then this has been a fairly decent updates. Underlying profits edged higher, net assets improved considerably and the strong cash generation continues apace. The excellent performance in the dairy division, driven by lower farmer inputs, new products gaining traction and increased orders in China was partially offset by a slightly disappointing performance in protection and defence with a new competitor meaning that M61 filter orders ceased, although the second half is expected to improve with the new emergency escape breathing device expected to secure orders from the US Navy. The dividend yield remains low but there is a large amount of net cash that could be used to invest into the business or return to shareholders. The retirement of the long standing CEO is a bit of a blow so I hope the successor will be able to continue with his success. I remain holding the shares with an eye on the performance of the defence business.

There has been some recent weakness in share price with a sideways trend so far this year but the long term uptrend based on the 200 day moving average is still intact.

On the 6th August the group announced that they are acquiring InterPuls for a cash consideration of €25.75M along with the acquisition of €4M of net debt belonging to the company. Interplus is a family owned company in Italy that has developed a range of specialist milking components, including pulsators, milk meters, automatic cluster removers and vacuum pumps. In addition to traditional milking components, they are also expending into high-tech sensors and devices to monitor the life cycle of a cow, analysing milk production, reproduction and health data to provide critical management information to increase the operational efficiency of the farm. The acquisition generates goodwill of just under €20M and profit before tax was €2.3M last year. The group expects the acquisition to be significantly earnings enhancing in 2016. It should broaden their product range, client base and geographic reach and seems a decent if slightly expensive acquisition to me.

On the 2nd September the group released a trading update. In the Protection and Defence division, as expected, deliveries of the mask systems to the DOD remained at a similar level to that seen in the first half of the year and the group received their first M61 filter order of the year for 123,000 pairs which will be partially fulfilled before the year end. The non-DOD markets have performed well without the benefit of any significant individual impact orders. A number of high value opportunities are in the pipeline and they now expect to see the benefit of these orders next year. The flexible fabrications business is expected to show a strong second half of the year. The development programme with the US Air Force for the JSAM MM53 continued to progress well and they have been awarded additional funding to support the next year of testing with a production contract expected to follow thereafter. The integration of HUDstar Systems is progressing well and positive benefits are expected next year.

In the Dairy division, the positive momentum generated in the first half of the year has continued and trading remains strong. Take up by farms of the Cluster Exchange Service remains at encouraging levels in both North America and Europe. The continued positive performance in both areas of the business therefore leads the board to expect that the outturn for the current year will be in line with current market expectations.

On the 1st October the group announced the appointment of Rob Rennie as CEO from December. He has held a number of positions at Invensys, with the most recent role being president of the energy controls group, a division with annual sales of more than $400M. This group included Eurotherm, a supplier of industrial and process control, measurement and data management solutions. He was the driving force behind the evolution of Eurotherm and was part of the team that sold Invensys to Schneider Electric in 2014.

On the 6th October the group released a statement covering trading in the year a whole and the year has ended strongly. This was primarily driven by the receipt and rapid fulfilment of a late order for respirators from a customer in the Middle East. This, together with strong trading in the American law enforcement market, leads the board to expect the adjusted operating profit for the year to be significantly ahead of current market expectations. A number of high value Middle Eastern opportunities remain in the pipeline and the board expect to see the benefit of these orders in 2016.

This sounds like a great update to me, with the promise of further next year. I suppose the only mitigation is whether these orders will be sustainable on an ongoing basis but nonetheless, really pleased with this update and surprised the shares have not gone higher.

On the 9th October the group announced the acquisition of the Argus thermal imaging camera business of EV2 technologies for £3.5M in cash which will be funded from existing debt facilities. Argus is a designer and manufacturer of thermal imaging cameras for the first responder and fire markets with revenues of £5M last year. It is expected that the acquisition will be modestly earnings enhancing in the current year and it is a strategic addition to the fire and first responder product range and should generate longer term product development opportunities for the protection and defence business.