Avon Rubber have now released their interim results for the year ending 2019.

Revenues declined when compared to the first half of last year due to a £3.8M fall in protection and defence revenue and a £300K decrease in dairy revenue. Cost of sales also fell to give a gross profit £2M lower. Depreciation was down £400K but other selling and distribution costs were up £900K. Amortisation increased by £900K and there was a £2.9M charge relating to the GMP equalisation. This meant that the operating profit declined by £6.1M. Finance costs were slightly lower and tax charges fell by £300K to give a profit for the period of £2.8M, a decline of £5.7M year on year.

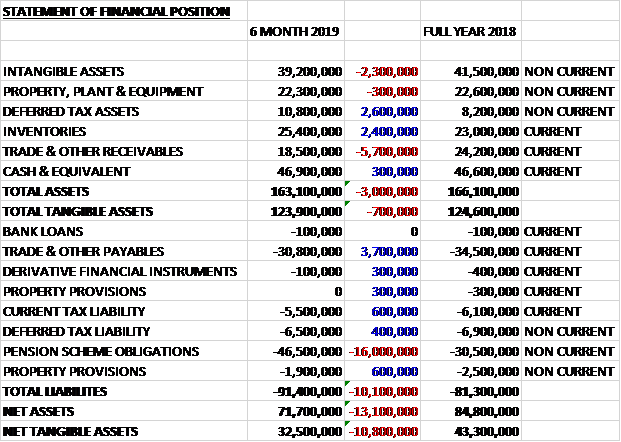

When compared to the end point of last year, total assets declined by £3M, driven by a £5.7M fall in receivables and a £2.3M decline in intangible assets partially offset by a £2.6M growth in deferred tax assets and a £2.4M increase in inventories. Total liabilities increased during the period as a £3.7M decrease in payables was more than offset by a £16M increase in pension obligations. The end result was a net tangible asset level of £32.5M, a decline of £10.8M over the past six months.

Before movements in working capital, cash profits declined by £3.4M to £12.7M there was a cash outflow from working capital which was higher than last time but both tax and interest charges reduced slightly to give a net cash from operations of £8.9M, a decline of £7.3M year on year. The group spent £2.3M on fixed assets and £1.8M on purchased software so the free cash flow came to £4.8M. Of this, £3.3M was spent on dividends and £1.3M on their own shares to give a cash flow of £200K and a cash level of £46.9M at the period-end.

The operating profit in the Avon Protection division was £6.1M, a decline of £2.6M year on year. Military revenues rose but both law enforcement and fire revenues declined. The group were awarded two significant long term contracts with the US DOD. The M53A1 framework contract, which also covers additional products has a maximum value of $246M and a minimum five year duration. This framework is accessible to a number of different customers within the DOD including all four military service branches. The first order under the contract worth $20.2M was received in March with deliveries starting in the second half of the year.

The M69 sole source contract to supply the DOD with the M69 Joint Service Aircrew Mask for Strategic Aircraft, related accessories and engineering support extends their portfolio reach into the aviation sector for the first time and has a maximum value of $93M and a minimum five year duration. The first orders, worth $17.8M, were received in February with deliveries also starting in the second half.

These contract awards support their portfolio as it transitions from being historically focused on the M50 mask system to becoming a multi-product portfolio. Having grown orders ahead of revenue, these contracts together with a broadening ROW military and law enforcement customer base provide the group with greater flexibility to manage order fulfilment scheduling.

The extended US government partial shutdown has impacted profit in the period from their ROW military and law enforcement customers. The admin backlog created continues to reduce and with a strong opening order book, the recently announced mask system contract and a pipeline of other opportunities they have good visibility for the second half of the year.

The military order book of £44.2M has grown significantly in the period driven by the first orders for the M69 aircrew mask and the M53A1 mask and powered air system contracts. Military revenues of £30.9M were 7.2% higher. DOD revenues of £22.9M were lower than last year with lower shipments of M50 mask systems and a different phasing of filters, spares and accessories. This was offset by a £6M increase in revenue from ROW customers reflecting completion of the Norwegian military MCM100 underwater rebreather order.

Law enforcement revenue reduced by 38%. This was significantly impacted by the extended US government partial shutdown. Delays in the timing and shipment of orders resulted in a carryover of revenue into the second half with an opening order book of £8.3M compared to £3.6M at the end of last year. They expect a much stronger second half for law enforcement as a result, the impact of delays in H1 mean that they do not expect to show year on year growth for the business, however.

Fire orders received reduced by 2.3% to £8M. The timing of shipments resulted in revenue decreasing by 11.4% which is offset by the growth in the order book of £1.3M, supporting expectations of a return to growth in the second half. Delays in the NFPA approval process mean they are now expecting to be able to launch their upgraded Magnum SCBA in Q4.

The operating profit in the Dairy division was £1.9M, a decrease of £700K when compared to the first half of last year. After a weaker environment through Q1 in the key North American and European markets impacted all business lines, Q2 has seen a rebound in dairy market conditions, with improving milk prices reflected in increased farmer confidence which has resulted in improved order intake and a strong opening order book for the second half.

Revenue decreased by 2.6% which was more than offset by a £1.2M growth in the order book to carry into the second half. Interface revenues increased by £200K and were impacted by weaker market conditions in Q1 although order intake increased by 2.7% due to improved market conditions in Q2. Precision, control and intelligence revenue fell by 9.5% reflecting the caution of dairy farmers to commit to capital investment over the period. Strong order intake over Q2 resulted in 11% growth in order intake over the period. There remains a growing pipeline of other opportunities in this market as the improving trading conditions support farmers looking to invest and deliver improved farm efficiency.

Farm Services revenue remained broadly flat. They are more resilient to the dairy market cycle but during the period they have seen a greater level of farm consolidations and closures. They have continued to convert farms to Farm Services but this has been offset by wider market dynamics. They anticipate a return to growth in the second half.

During the period they have taken the opportunity to consolidate all EU commercial operations into the existing Italian facility. This provides a single customer service point for all three lines of the business and at the same time they have also transferred the European liner production in house to support their operational efficiency.

The main on-recurring item relates to the £2.9M increase in pension liabilities following the GMP equalisation ruling.

As a result of the strong momentum in Avon Protection and despite the performance in the first half being adversely affected by the US government partial shutdown and challenging dairy market conditions, the board remains confident in delivering full year expectations. The opening order book for the second half of £59.1M represents a 38% increase compared to the same point of last year. The opening order book and mask system contract provide strong visibility into the second half of the year and the board remain confident in delivering full year expectations. Avon Protection revenues are expected to grow mid-single digit basis and with rebounding milk prices a stronger second half for the dairy division should result in flat revenues for the year.

At the current share price the shares are trading on a PE ratio of 21.8 which falls to 18.5 on the full year consensus forecast. At the period-end the group had a net cash position of £46.8M compared to £46.5M at the end of the year. After a 30% increase in the interim dividend the shares are now yielding 1.2% which increases to 1.5% on the full year forecast.

On the 2nd May the group announced that non-executive director Petrus Vervaat purchased 2,500 shares at a value of £36K.

Overall then this has been a difficult period for the group. Profits declined, net assets reduced and the operating cash flow fell, although there remained a decent amount of free cash generated. There were problems across both divisions. Protection was affected by the US government partial shutdown and the dairy division by a poor milk market and prices. For the second half, these issues seem to have mostly been resolved and there is a good opening order book. A forward PE of 18.5 and yield of 1.5% is not cheap but this is a quality company and I am minded to hold on.

On the 7th August the group announced that it had signed an agreement to acquire 3M’s ballistic protection business and the rights to the Ceradyne brand for an initial cash consideration of £75M and a further contingent cash consideration of up to £21M.

The business is a leader in critical personal protective equipment with established positions with the US DOD and has existing contracts for next generation ballistic helmets and body armour. It operates from three sites in the US and last year made an EBITDA of $10.8M. Recurring annual cost synergies of around £4M are expected to be delivered in the first full year of ownership from integrating IT systems and back office functions. The one-off costs to implement this are expected to be around £8M.

The acquisition is expected to close in the first half of 2020.

On the 16th September the group released a trading update covering the year where they noted that trading in the second half continued in line with expectations. Revenues are expected to grow by 4% on a constant currency basis with the EBITDA margin modestly ahead of last year. The protection division had a strong year, underpinned by the performance of the military business. They have completed the planned initial deliveries of the M69 aircrew mask and the M53A1 mask and powered air system to the US DOD. They have also completed the $16.6M ROW mask system contract announced in April.

Law Enforcement performance has been stronger in the second half but the impact of delays resulting from the extended US government partial shutdown in the first half will result in a year on year revenue decline. Fire performance in the second half has been further impacted by delays in the NFPA approval process for the new safety standard, which has prevented the launch of their upgraded Magnum SCBA. They now expect to launch it in the first half of 2020.

The improved global dairy market conditions experienced in Q2 have continued into the second half, resulting in improved trading conditions. This has resulted in the business returning to revenue growth across all lines.

The US DOD contract awards totalling $340M for the M53A1 and M69 mask systems along with the acquisition of 3M’s ballistic protection business has strengthened the medium-term outlook which leaves the group well positioned to deliver further growth.