Bioquell has now released their final results for the year ended 2017.

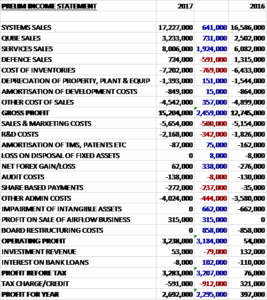

Revenues increased when compared to last year as a £591K decline in defence sales was more than offset by a £1.9M increase in services sales, a £731K growth in Qube sales and a £641K increase in systems sales. Cost of inventories increased by £769K but depreciation was down £151K and other cost of sales decreased by £357K to give a gross profit £2.5M higher. Sales and marketing costs increased by £500K and R&D costs were up £342K. There was a net £338K positive swing to forex gains but share based payments were up £237K and other admin costs grew by £444K. There was no impairments, which cost £662K last time and no board restructuring costs (£858K last year). In addition there was a £315K profit on the sale of the Airflow business so the operating profit grew by £3.2M. A decline in investment revenue was offset by a fall in loan interest but tax charges were up £912K to give a profit for the year of £2.7M, a growth of £2.3M year on year.

When compared to the end point of last year, total assets increased by £4.2M driven by a £5.8M growth in cash, partially offset by a £950K decline in trade receivables and a £717K decrease in the value of development costs. Total liabilities also increased during the period as a £392K decline in other payables was more than offset by a £558K growth in current tax liabilities and a £354K increase in the warranty provision. The end result was a net tangible asset level of £19.9M, a growth of £3.7M year on year.

Before movements in working capital, cash profits increased by £2.6M to £6.2M. There was a modest cash inflow from working capital and interest payments reduced to give a net cash from operations of £6.9M, a growth of £2.8M year on year. The group spent £757K on property, plant and equipment; £132K on development costs and £52K on other intangible assets to give a free cash flow of £6M. Of this, a net £34K was spent on share acquisitions which meant that the cash flow for the year was £6M and the cash level at the year-end was £14.6M.

The profit in the Bio business was £4M, a growth of £1.4M year on year. The loss in the Defence business was £35K, a detrimental movement of £237K when compared to last year. The group intends to grow revenues by expanding its global life science sales and marketing team with particular focus in the US. The current level of recurring revenues is 42%. They are working to increase this level by selling service packages to customers at the time they purchase new equipment, and by converting long standing customers onto upgraded equipment which uses only the group’s own consumables.

In the short term the board anticipate that R&D costs will continue at a roughly similar level. They continue to work on extensions to their product portfolio rather than on major new product developments. The £100K increase in engineering costs was attributable mainly to the hiring of additional staff in the quality department. Capex continues to run significantly below the depreciation charge reflecting the investments needed to support the growth of the business that have been completed over recent years. A refurbishment programme for the group’s RBDS equipment will increase capex in 2018, which is expected to be around £2M.

On the 8th January, after the year-end, the group disposed of its airflow spare parts business to Crowthorne, having disposed of the legacy Airflow service business during the year.

Going forward the business has started 2018 in line with expectations and the board remains confident in delivering further growth in profits.

At the current share price the shares are trading on a PE ratio of 33.5 which falls to 28.7 on next year’s consensus forecast. At the year-end the group had a net cash position of £14.6M compared to £8.8M at the end of last year. The group is considering returning further cash to shareholders by way of share buybacks during the course of 2018 in lieu of paying a dividend.

Overall then this seems to have been a relatively strong performance from the group. Profits were up, net assets increased and the operating cash flow improved. The Defence business is struggling somewhat but this is more than made up for by the bio business, which is performing well. The shares are not cheap, however, there is no dividend and the forward PE is 28.7. Nevertheless, there is a strong net cash position here and I am holding on to my shares.

On the 23rd April the group released a trading update covering the year ended 2018 where they stated that trading had been in line with board expectations. They also stated that they expect further progress in the New Year despite the recent strengthening of sterling against the dollar.

On the 25th May the group announced the disposal of its defence business. It is being sold for an initial consideration of £400K with a further contingent consideration of up to £600K if it wins a specific contract for which it is bidding. Last year the business made an operating loss of £35K and any gain/loss from the disposal will not be material.