Bonmarche is a multi-channel retailer of affordable womenswear and accessories and are one of the UK’s largest retailers of affordable clothing for women over fifty. They have 292 stores and also offer online, catalogue, TV and telephone shopping. The immediate parent company is BM Holdings, itself advised by a private equity investment fund of Sun Capital Partners Inc. with a holding of 52.4% of the company.

The group sells gift vouchers. On those transactions, no immediate revenue is recorded and the value is recorded as a deferred income liability. When a gift voucher is redeemed, revenue is recognised and the deferred income balance is reduced. The deferred income liability includes liabilities in respect of some vouchers which are unlikely to be redeemed and the carrying amount of gift voucher liabilities at the year-end is £1.1M.

It has now released its final results for the year ended 2015.

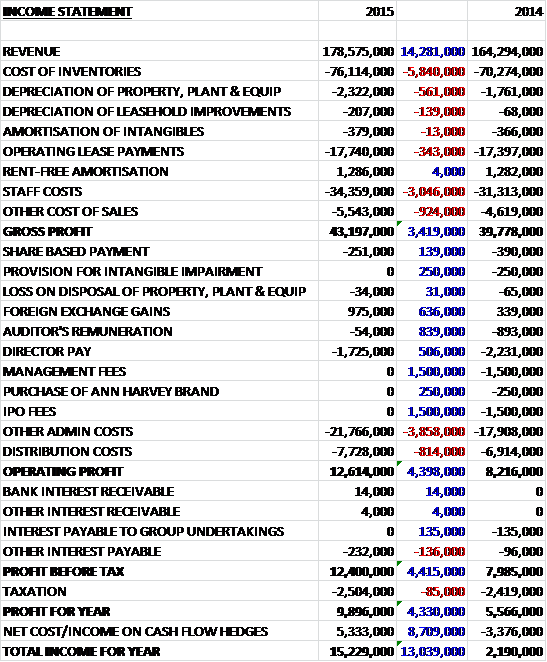

Revenues grew by £14.3M when compared to last year. Cost of inventories increased, as did depreciation, staff costs and other cost of sales so that gross profit was £3.4M ahead of last year. We then see a much lower charge for the audit costs, more foreign exchange gains and the lack of several non-underlying costs that occurred last year, in particular £3M in management fees and IPO costs. Underlying admin costs increased, however, as did distribution costs, mainly related to an increase in volume, to give an operating profit some £4.4M higher. Finance costs and tax were broadly flat so that the profit for the year was £9.9M, an increase of £4.3M year on year.

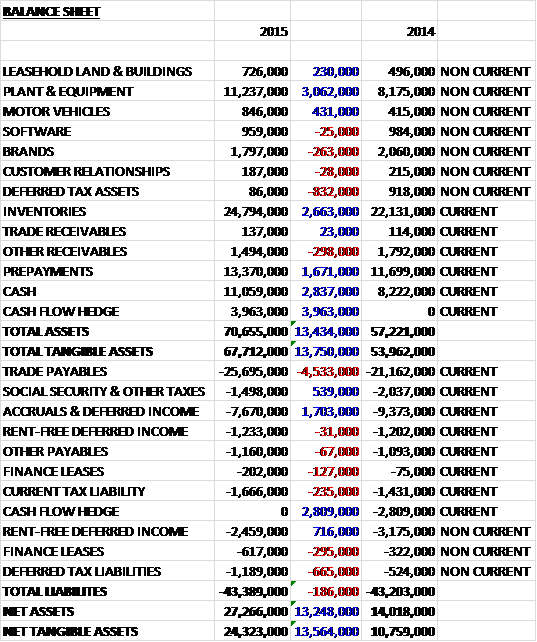

When compared to the end point of last year, total assets increased by £13.4M driven by a £4M growth in the hedging asset, a £3.1M increase in plant and equipment, a £2.8M growth in cash, a £2.7M increase in inventories and a £1.7M growth in prepayments mostly relating to business rate charges. Total liabilities also increased as a £4.5M growth in trade payables was partially offset by a £2.8M fall in the hedging liabilities and a £1.7M decline in accruals and deferred income. The end result is a net tangible asset level of £24.3M, an increase of £13.6M year on year.

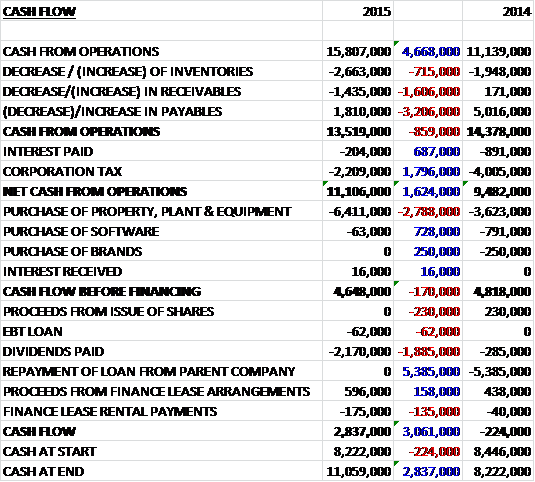

Before movements in working capital, cash profits increased by £4.7M to £15.8M. A working capital cash outflow, however, was offset by a tax and interest rate that combined broadly halved so that net cash from operations was £11.1M, an increase of £1.6M year on year. The group then spent £6.4M on property, plant and equipment, mainly relating the opening of new stores and concessions, the replacement of some lorries and expenditure on store systems, to give a free cash flow of £4.7M, of which £2.2M was spent on dividends to give a cash flow for the year of £2.8M and a cash level at the year-end of £11.1M.

Overall the year was one of two halves, to coin a well-used footballing phrase. A strong performance in the first half was supported by good summer weather, however, the mild autumn created more difficult trading conditions in the second half of the year.

Store like for like sales increased by 4% which increased the market share by 12.8% to 4.4% of the UK women’s value clothing market. During the first half of the year, total sales increased by 11.8% and store like for like sales were up 7.8%. Multi-channel made good progress, growing 50.6% year on year. The warmer than average weather created particularly strong demand for big seasonal categories such as jersey tops, cropped trousers, shorts and swimwear.

In the second half of the year, sales increased by 5.7% with store like for like sales up just 0.2% and multi-channel growing by 25.6%. The group was not immune to the effects of the mild conditions in autumn as customers had less reason than normal to invest in heavier clothing such as knitwear and coats when the product mix in-store had shifted towards these items. In addition, the group have identified that for the coming autumn season, improvements can be made to elements of the outerwear and knitwear ranges. They have also reduced the reliance on coats and knitwear during the early autumn months.

The mild autumn also resulted in increasing levels of discounting activity on the high street, progressively intensifying and culminating in widespread price reductions on Black Friday which continued in the approach to Christmas. This took the edge off December’s full price sales with many sales (including Bonmarche’s) beginning before Christmas which also had the knock on effect of reducing the impact of January sales, leading to a difficult final quarter.

Through the mystery shopper programme, the group have learned that customers want more fashionable products, so they have ensured that they have continued to increase the percentage mix of their contemporary fashion offer but without alienating customers who are slower to make the move away from more traditional items. Many of the more fashionable designs have been introduced via the David Emanuel label which tends to feature clothing focused towards special occasions. This sub-brand accounted for about 12% of sales during the year.

Last summer the group launched their Ann Harvey collection in 23 stores and online, initially as a trial. The trial results have helped them refine the collection for autumn/winter which will be primarily aimed at offering existing and new plus-size customers a more contemporary range than the Bonmarche main range, which does not have a plus-size range, at slightly higher price points. They will offer this range in sizes 18 to 32. As a result of feedback from customers, during late autumn the group also began to test a limited range of menswear in fifty stores. The trial is still at an early stage but they are optimistic that this is an opportunity which merits further exploration. The trials have begun to indicate which products work best in the autumn season and will continue in order to ascertain the same about the summer season.

A key priority during the year was to improve the usability of the website. They have made a number of improvements to the site, including the introduction of a simplified landing page, clearer main banner messaging, a more logical hierarchy of tab messages down the page, fewer category descriptions, and similar search and checkout tabs. Email campaigns have been improved, to be more relevant and to include a broader range of content, for example in relations to promotions, occasion dressing or style tips. Traffic reaching the website via tablets now account for 38% of all traffic and 32% of online sales with sales made via computers declining and the relatively small number of mobile sales increasing. The group therefore began working with their website provider to develop a responsive website but its development has taken longer than originally planned and it is now expected to be launched in July 2015.

The catalogues are now well established as a popular complement to the stores. Although their primary use is to showcase new collections prior to a purchase made in store or online, some customers welcome the facility to order directly from the catalogue via the call centre. Sales made through the call centre increased by 32% compared to the previous year.

During the year the group opened 29 new stores, most of which were concessions, particularly in garden centres. They are pleased with the performance of the six new Solus stores and will be more selective going forward with the garden centre sites but they plan on opening a further 15 to 20 concession locations in 2016, along with testing other concession store formats.

During the year a number of investments were made in the stores. Some of these were part of the continuing moves of making the stores more attractive places to shop and some were less visible infrastructure investments to underpin future growth. New fascias were installed in 18 stores and this programme will grow next year as they plan to replace older store fronts and bring them up to date with the latest branding. The cash desk units were replaced in 209 stores to prepare them for the installation of new tills and they made significant upgrades to the store communications infrastructure, including installation of broadband, Wi-Fi and local networks in each tore, also part of the preparatory work for the EPOS till replacement project.

During the year the group began the project to replace the store systems, including EPOS, with an up to date solution that provides customers with a more coherent experience regardless of the shopping channel used. Good progress has been made installing the infrastructure necessary to enable the system to operate but progress on implementation of the system itself has been slower than they would have liked. They are therefore reviewing their options, including the choice of supplier, to ensure that they progress with the most appropriate solution.

They have identified the opportunity to improve stock availability across the entire product range and during the year they introduced a trial to rest whether shortening the lead time between picking an item in the warehouse and delivering it to stores would help achieve this. The results were apparently encouraging and in the coming year they will make investments in their delivery operation to shorten the time take to deliver to stores.

The group have not traditionally used conventional paid advertising to promote the brand but instead rely on their magazine and TV shopping. For the magazine they distribute 40,000 copies four times per year and this year it was updated to reflect the other brand developments. The partnership with the Ideal World TV shopping channel has continued to work well, and the focus during the year was to increase the number of weekly shows, increased to two-hour slots during peak selling times. This has proved successful and this activity continues to generate a small profit, as well as fulfilling its main purpose which is to create awareness of the brand amongst a wider group of potential customers.

During the first half of the year the cost of the hedged US dollars was greater than for the corresponding period last year but the level of discounting during the period was slightly lower due to strong sales. The exchange rate effect was the stronger of the two and as a result gross margin was 56.5%, 0.8% lower. During the second half of the year, the effect of these two variables reversed. The average rate at which the group bought dollars to meet their requirement was better than in the previous year but as trading conditions became more difficult and more discounts were applied to maintain rates of sale. Again, the exchange rate effect was the stronger and the margin in the second half increased by 1.2% to 58.2%.

I don’t really take much notice of awards usually because they all seem to just be purchased by the company that wins but I did notice that Bonmarche were voted second to John Lewis in the Clothing and Shoes category for Which, and that award does have some kudos in my view.

There have been a number of board changes. Tim Mason was Chairman and a partner of Sun European Partners, whose affiliate is the company’s largest shareholder. He stepped down as a partner of Sun and therefore also as Chairman in April. John Coleman replaced Tim as Chairman and Michael Kalb who is a senior MD at Sun and has been working with the company since its acquisition by Sun, joined the board as its appointee as a non-executive director

The group is rather susceptible to exchange rate changes as they pay most of their overseas suppliers in US dollars. They do enter into forward foreign currency hedges to cover up to 100% of forecast inventory purchases for a year so a 10% weakening of the dollar would decrease profits by just £92K. In addition they are also clearly susceptible to changes in the economy in general as a slow-down in consumer spending could materially affect the group’s financial condition. The other big risk involves weather conditions. Prolonged unseasonal or extreme conditions may have a material adverse effect. Finally, and very topical at the moment, is the risk of an increase in the minimum wage as they pay most of their non-management employees minimum wage so an increase has an adverse impact on costs.

The group doesn’t currently have any debt but there is a committed revolving credit facility of £10M available should seasonal working capital fluctuations create the need to use it (although this was not necessary at any point during the past year). There are capital commitments of £1.4M outstanding at the year-end and in line with most other retailers, there are some hefty operating leases outstanding here with £65.3M at the end of the year.

Going forward it is believed that the outlook for the business over the next year is positive. They have multiple growth opportunities to build upon as the market gradually recovers but the board remain neutral in their assessment of the likely effect of external factors on their business.

At the current share price the shares trade on a PE ratio of 15.8 which falls to 14.6 on next year’s consensus forecast. The shares are currently yielding 2.2% increasing to 2.5% on next year’s forecast. At the year-end there is a net cash position of £10.2M compared to £7.8M.

Overall then this seems to have been a good year for the group. Profits were up, net assets increased and operating cash flow grew, with plenty of free cash generated. In the first half of the year, things progressed well with good summer weather leading to a strong performance but in the second half of the year a mild autumn reduced sales and also increased promotions. This effect was offset by favourable USD exchange movements, however. Both like for like store sales and online sales increased in the year and a number of changes being made suggest growth should continue, with more contemporary fashion ranges, more choice for plus size customers, the trial of a menswear offering and improvements to the website all taking place.

The group currently trades on a forward PE of 14.6 and a dividend yield of 2.5% so with no debt, this looks fairly good value. I like this company, they are trading well and the shares are not too expensive. Of course, the issue of inclement weather is never far away and could ruin trading through no fault of the company but overall I might look to take a position here.

On the 30th July the group announced a trading update for Q1. Sales in the quarter increased by 3.8% but like for like sales fell by 1.7% after they increased by 13.5% in Q1 last year, mainly as a result of inconsistent spring and early summer weather. At this early stage of the year the board are confident of achieving its expectations for the year.

On the 18th September the group announced its intention to join the main market and to cancel its shares on AIM, which seems to be a good idea to me. Also, they noted that having reviewed current trading, trading expectations for the full year remain unchanged. It is expected that the full year performance for 2016 will be weighted towards the second half of the year as the benefits of stronger like for like sales growth due to weaker comparatives, new stores and an improved online offering are realised. The board expect the results for H1 2016 to be broadly in line with H1 2015.