E2V has now released its interim results for the year ending 2016.

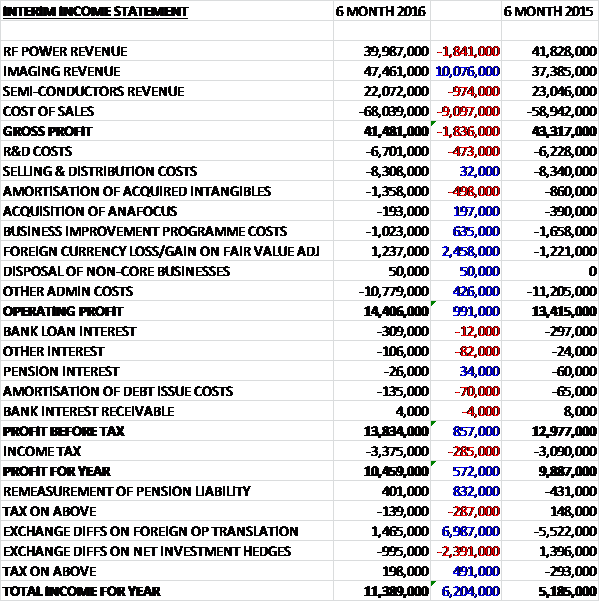

Revenues increased when compared to last year as a £1.8M fall in RF Power revenues and a £974K decline in semiconductors revenue was more than offset by a £10.1M growth in Imaging revenue reflecting a £4.4M contribution from Anafocus and a forex benefit of £2M. Cost of sales also increased to give a gross profit some £1.8M higher than in the first half of 2015. R&D costs increased somewhat as did the amortisation of acquired intangibles but underlying admin costs fell due to lower management incentives and there were a number of lower non-underling costs such as a £635K decline in business improvement programme costs and a £2.5M swing to a foreign currency gain on the hedging instruments. Finance costs then increased and tax was slightly higher so that the profit for the half year was £10.5M, an increase of £572K year on year.

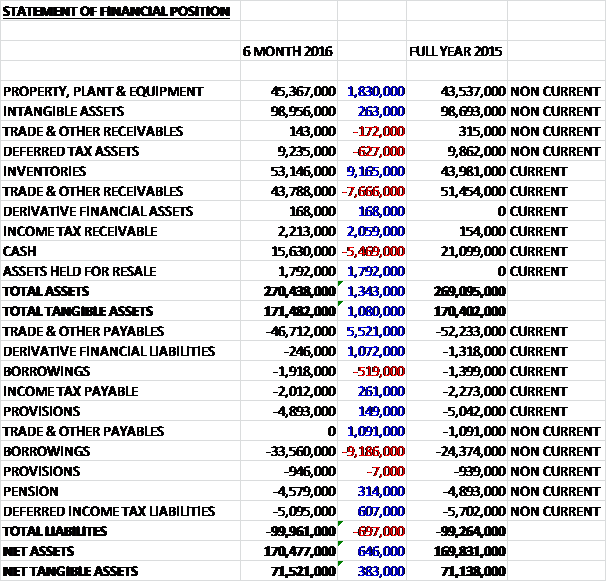

When compared to the end point of last year, total assets increased by £1.3M driven by a £9.2M growth in inventories, a £2.1M increase in income tax receivables, a £1.8M growth in property, plant and equipment, and a £1.8M asset held for sale, partially offset by a £7.7M fall in receivables and a £5.5M decrease in cash. Liabilities also increased as a £9.6M growth in borrowings was partially offset by a £6.6M decline in payables, and a £1.7M fall in derivative financial liabilities. The end result is a net tangible asset level of £71.5M, an increase of £383K over the past six months.

Before movements in working capital, cash profits fell by £1.8M to £19.7M. There was then a large cash outflow from working capital with a particularly big increase in inventories. A higher tax payment then meant that the net cash from operations was £8.1M, a decrease of £11.2M year on year. The group spent £6.6M on fixed tangible assets and £1.8M on the acquisition of the subsidiary to give an outflow of £571K before financing. The group then spent £3.7M on treasury shares and £7.9M on dividends before an income of £7.1M from new borrowings meant that there was a cash outflow of £5.4M during the period to give a cash level of £15.6M at the end of the first half of the year.

The operating profit in the imaging business was £4.6M, an increase of £1.9M year on year. In professional imaging the industrial vision market is driven by the increased use of sensors in industrial automation where the group sees high single figure market growth rates. The new product launches are making new markets and winning market share in industrial vision. The acquisition of Anafocus has brought new customers and strengthened their existing relationships and provides growth through innovation leading to new product lines and winning custom programmes. In the first half, the combination of new product introduction has doubled growth. In space, governments increasingly seek to maintain independent observation capabilities and the expansion of climate change monitoring is driving growing demand for new observation satellite programmes.

Excluding AnaFocus, organic growth was 15%. Professional imaging represents two thirds of the division’s revenue with the balance coming from space. Underlying growth came from strong demand in automatic data collection, machine vision sensors and optical inspection CMOS cameras. Life science was steady reflecting end user demand remaining at similar levels to the prior year. In space, revenue growth came through delivery on programmes, although these programmes remain technically challenging and they are continuing to commit the resources needed to improve delivery to customers.

The overall profit growth reflects the contribution from the revenue growth with Professional Imaging delivering mid-teen margins and space margins being affected by the additional resources required to support customer programmes. R&D activities have been increased to drive future growth, focusing on areas of strong customer demand, in particular industrial automation and space. In space, work in progress on programmes has increased supporting the anticipated step up in revenue in the second half of the year. The order book at the end of the period was £100M compared to £82M at the same point of last year. The orders due for delivery within the next year were £65M.

The operating profit in the RF Power segment was £8.2M, a decline of £777K when compared to the first half of last year. In radiotherapy the group continue to anticipate that spares revenue will grow in line with the past expansion of the installed base over the last five to ten years. Revenue growth is expected from continued new build demand, which accounts for about a third of growth, and which currently has low single figure growth rates, with two thirds from growing installed base which has had higher growth rates in prior years. Defence budgets across the NATO countries are constrained and the group do not expect to see this change in the short term. The majority of growth in the division is anticipated to come from radiotherapy where they continue to prioritise their investment. The other applications continue to be driven by the general industrial cycle.

There was a decline in revenues from the division with a strong growth in radiotherapy reflecting increased demand from the key OEM customers, whilst absorbing some destocking, along with growth in the commercial and industrial markets. This was offset by weakness in defence with slower than anticipated programme wins and a pause in industrial processing systems. Margins were maintained at 22% despite the lower revenues. This reflects cost control and the alignment of the cost base in defence to the expected activity level. R&D activities continue to be focused primarily on radiotherapy applications. Inventory levels have increased to support customer delivery and as part of a specific programme to reduce over concentration in the supply base and provide continuity of supply as new suppliers are qualified.

The order book at the period-end was £60M compared to £85M at the same point of last year. The decrease reflects the cycle of the multi-year radiotherapy contracts with delivery against their contracts for their key OEM customers. They have also had a reduction in the defence order book reflecting slower than expected programme wins. The orders due for delivery over the next year were £44M, reflecting a lower than a full year cover for radiotherapy. The board expect to renew one radiotherapy multi-year order in the final quarter of the current year along with securing further specific defence orders for delivery in the second half of the year.

The operating profit in the semiconductors business was £4.2M, a fall of £141K when compared to the first half of 2015. The group sees continued ongoing market growth for high reliability products in civil aviation applications such as flight control computers and engine management systems, driven by civil aviation applications which have seen high single figure growth rates. In the last two years they have seen increasing interest in the high reliability microprocessors for space applications that require increased levels of on-board processing. The group have introduced new own design high speed data converters and new multi-chip modules which enable their customers innovation. They have also secured design-ins for their products on future programmes for civil aerospace and space applications.

Revenues declined year on year. Flow down on programmes has increased activity for US legacy product lines, along with good growth coming from their own design high speed data converters for space applications which was offset by lower demand for microprocessors. In other applications there was the anticipated decline in the legacy ASIC business as these products approached the end of their life cycle. The relatively small fall in profits compared to the revenue was due to an improved mix, with growth in the higher margin lines, good cost control and improved operating performance. Inventory levels have been increased both to take advantage of opportunities for strategic inventory purchases and to support the revenue step up anticipated in the second half of the year. The order book at the end of the period was £27M compared to £23M at the same point of last year. This order intake reflects the anticipated flow down on programmes and the order delivery within the next year remained flat at £20M.

The group acquired Anafocus last year but during the period the group paid £1.8M which represents full payment of the first two payments of contingent consideration. Two further payments remain outstanding, one of which is due for payment in the second half of the year and the second payment is due for payment in the first half of next year. Management expects that the remaining target will be met and a liability of £1.8M is recorded in respect of this. During the period the group has repositioned its regional teams in the US and Asia so that they are aligned with the divisions and has reorganised RF’s defence business into three distinct units. Costs, principally staff related, of £917K have been recognised in the period. Project Sunrise, the reorganisation of the footprint at the Chelmsford facility continued and costs of £106K were incurred in the period and second half restructuring is expected to cost about £1M.

At the end of the period the group had capital commitments of £2.3M, principally relating to the acquisition of new plant and machinery. After the end of the balance sheet date the group sold the thermal imaging business. The business had assets of £1.8M and the estimated net proceeds on the transaction are £3M. The total order book at the period-end was £187M compared to £190M at the same point of last year which reflects a strong order intake in imaging offset by the cycle on contracts for radiotherapy. The order book for delivery over the next year is £130M compared to £138M last time.

The focus for the second half is building, in professional imaging, semiconductors and RF defence, on the satisfactory order book and delivering the technically challenging customer programmes in space. The board remain cautious about the broader economic environment and assuming no deterioration in market conditions, the guidance for 2016 as a whole remains unchanged.

After a 6.7% increase in the interim dividend the shares now yield 2.2% which increases to 2.3% on next year’s consensus forecast. The PE ratio for the full year 2016 is expected to be 16.9. At the period-end the group has a net debt position of £19.8M compared to a net debt position of £4.7M at the end of last year and there is still £62.6M of the revolving credit facility that remains undrawn.

Overall then this has been a bit of a slow period for the group. Profits have increased year on year but this just seems to be due to the positive fair value movement of the exchange rate hedge and underlying profits are presumably lower although I am a bit unsure as to whether this fair value movement mitigates unfavourable exchange rate movements elsewhere on the income statement such as in revenue? Net assets did increase modestly during the period but operating cash flow was down and there was no free cash, mostly as a result of a large investment in inventory.

The imaging division seems to be doing well with increased demand from professional imaging and a bulging order book. Semiconductors seem to be rather flat as a reduced microprocessor demand and a falling legacy business is being mostly offset by improvements in other parts of the division. The RF Power division seems to be struggling a bit, however, mainly as a result of lower NATO defence budgets. The order book in the RF Power business looks rather poor too, but this seems to be a reflection of the radiotherapy order cycles. With a PE ratio of 16.9 and a dividend yield of 2.3% along with an increased net debt, these shares do not really seem that good value to me. Nonetheless I am willing to hold on to them for now.

On the 25th January the group announced the acquisition of Signal Processing Devices Sweden, a leader in the design and development of high performance analogue to digital processing technology for up to £12M. Their products are used by customers including leading OEMs across a number of sectors such as industrial test & measurement, healthcare, communications, and science. It also brings proven patented technology in software and board level sub-systems and services which complement the group’s broadband date converter business. Last year the business made sales of $4M but no profit figure is mentioned so I assume it is loss making with the acquisition expected to be earnings enhancing in 2017. The initial cash purchase price is £9.5M with a further earn out of up to £2.7M in cash which is being funded from existing resources. I have to say that this looks a little pricey to me.

On the same date the company released a Q3 trading update. The business performed in line with expectations apart from Space Imaging where they have not seen the anticipated acceleration in programmes delivery, which remain technically challenging. Nevertheless, assuming stable forex and market conditions, management expects a satisfactory outcome for the full year trading performance and the financial position of the company remains strong.

Overall then, I am not sure about these updates. The acquisition seems a bit expensive and trading in Q3 seems to have been a little disappointing. I remain out of these shares for now.

On the 3rd March the group announced the appointment of Carla Cico as a non-executive director. She is also a member of the board of Allegion, a global provider of security products and Alcatel-Lucent, a telecoms provider. In her previous roles she has been CEO of both Rivoli SPA and Ambrosetti Group – China.