Braemar has now released its interim results for 2015.

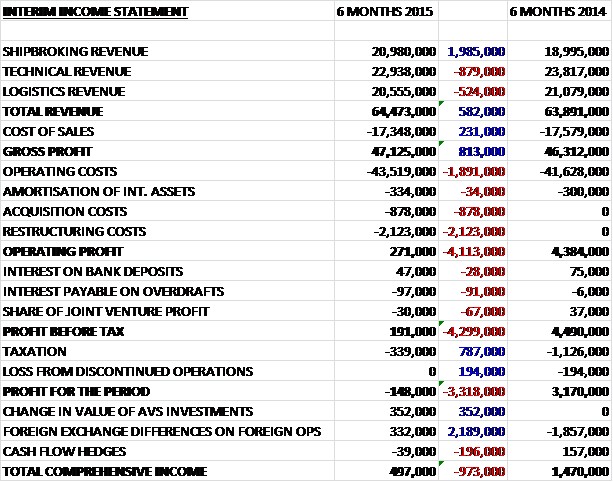

Although shipbroking revenue was up nearly £2M, this was partially offset by falls in technical, now including the old Environmental business, and logistics revenue. Cost of sales were slightly lower than in the first half of last year, so this helped the gross profits up by £813K. This increase was reversed by a £1.9M increase in operating costs, however, and the one-off £2.1M of restructuring costs and £878K of acquisition costs pushed operating profit down to £271K, some £4.1M worse than in the first half of last year. Some increases in finance costs were more than offset by a £787K reduction in taxation and the lack of a loss from discontinued operations that occurred last year so the loss from the year ended up at £148K, a £3.2M reversal on the same period of 2014.

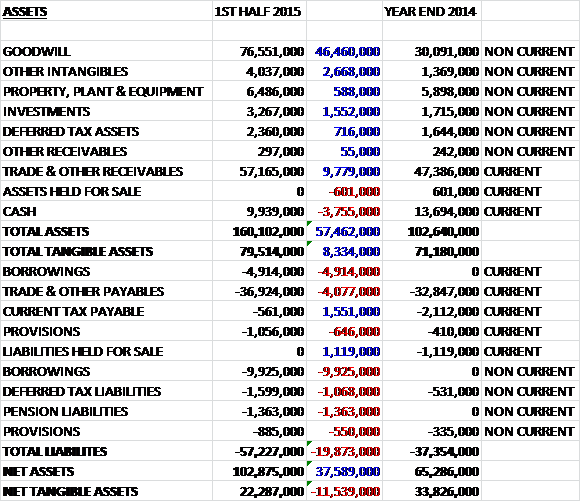

When compared to the end point of last year total assets soared by £57.5M. This was predominantly driven by a £46.5M increase in goodwill related to the acquisition with smaller causes being the near £10M increase in receivables, the £2.7M growth in other intangibles and the £1.6M increase in the value of investments. Liabilities also increased when compared to the end point of 2014. Borrowings shot up by £14.8M, payables were up £4.1M, pension liabilities grew by £1.4M and deferred tax liabilities increased by just over a million pounds. Although net assets increased, due to the huge increase in goodwill, net tangible assets actually fell by £11.5M to a rather measly £22.3M.

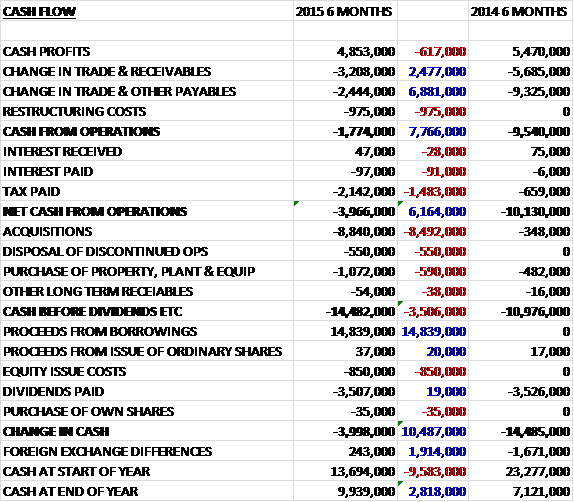

Before movements in working capital and restructuring costs, cash profits were some £617K lower than in the same period of last year at £4.9M. Although lower than last year, changes in receivables and payables still drive this into negative territory and the near £1M of restructuring costs meant that there was a £1.8M cash outflow from operations. Clearly the £2.1M spent on tax exacerbated this further and there was a net cash outflow of £4M from operations –not a good result but still £6.1M better than last year! The group spent about £1M on capital expenditure and somehow managed to spend a net £550K on a disposal. The big destination for the cash, however, was the £8.8M spent on the acquisition. There was a further £850K spent on equity issue costs and the group still decided to pay £3.5M in dividends. Even after the £14.8M of new borrowings there was still a £4M outflow of cash for the half year, although the second half is always stronger cash-wise due to bonuses and dividends being paid in the first half of the year.

After £2.6M of exceptional items, Shipbroking posted an operating loss of £1.5M compared to a profit of £850K last time. Before amortisation and exceptional items, however, divisional operating profit increased by £300K to £1.4M (£100K of which can be attributable to ACM). The total forward order book increased by 12% over the last year to $56M, but revenues were affected by the weaker dollar to the tune of £1.4M. Despite fluctuating market conditions, one year time charter rates and vessel prices have improved since the first half of last year which suggests a cautiously optimistic outlook for the division.

Technical operating profits this year were £2.3M, a decline from the £3.4M during the first half of 2014. The decline was due to weaker oil and gas exploration activity in the Far East and difficult comparatives due to the strong performance this time last year. The marine warranty surveying and engineering consultancy was affected by the slowdown of activity in Asia and the business environment has become increasingly competitive. The hull and machinery damage surveying business performed steadily throughout the period and the number of new instructions were comparable to last year despite fewer claims globally. The offices in Europe, America and the Middle East region performed well while the office in the Far East saw a decline in activity.

The loss adjusting business performed well in the Far East office and the recently established Middle East office also received a number of high profile assignments in the period. The new business received a good mix of onshore and offshore assignments and the group has been included in the panel of adjusters for a number of major offshore construction projects. The engineering consulting business continued to operate on the construction of six LNG carriers and this project moved from the design phase to construction during the period. The North American office was appointed to the role of “Owner’s engineers” to the first significant LNG bunkering project aimed at vessels that use the gas as a bunkering fuel. The Environmental business, recently moved into the Technical division experienced routine levels of business with no major projects.

After £300K of exceptional items, logistics operating profits were £728K compared to £1.3M in 2014. The main reason for this was given as the sale of the Tours business. The ship agency business experienced weak market conditions in Europe in the first half of the year but the volume of trading was steady. A new office was opened in Houston and serves to compliment the other services the group offers from the city. The freight forwarding business underwent some management changes, reducing costs. It finished the first half strongly, and started the second half well.

Clearly the major event that occurred during the period relates to the acquisition of ACM Shipping for a total consideration of £51M (£10.1M in cash and £40.8M in new shares). The net assets of ACM only came to £4.6M so a huge goodwill of £46.4M was recorded as a result of the transaction. The acquired business contributed £1.8M in revenues and £144K in profits during the one month that it has been part of the group. There have been a number of one-off costs relating to the acquisition, including some redundancy payments as the cost base is decreased. Indeed, the group now expect to make about £4M in annual savings which was more than expected.

Going forward, the reduced cost base and full contribution from ACM is expected to lead to a stronger second half of the year and the board’s expectations for the year as a whole remain unchanged and are supported by the early indications of trading in the second half. There is now slightly more financial risk here. The group has taken on debt for the first time in a long time and ACM also came with some pension liabilities.

At the current share price the shares are yielding and impressive 6%, but the pay-out remains the same as last year. Whether this level of shareholder return is sustainable is of course open to debate. This half of the year has been somewhat difficult for the group, one-off costs meant that it made a loss but underlying profit was also down, predominantly due to problems in the Asian oil and gas market for the technical consultancy business. Net tangible assets also took a dive and the group now has a net debt position whilst cash flow was pretty dire. The acquisition is clearly the most important event, and quite a bit seems to have been paid on it. Having said all that, the second half is likely to be an improvement and will be interesting to see how much ACM contributes to the bottom line. The dividend yield is exceptional and I am happy to wait to see how the acquisition beds in.

On the 13th January it was announced that the Chelverton UK Equity Income Fund had purchased 50,000 shares (worth just over £200K) to bring their holdings above 3% to 3.12% of the total voting rights. It appears that other Cheverton funds also hold shares and the group as a whole is interested in 3.71% the total share capital. As an income based fund they are clearly attracted by the generous dividend yield on offer here. It is run by David Horner and David Taylor and whilst year to date the fund is down 1.66%, over the last 3 year it has grown by 74%. All in all, a decent vote of confidence.

On the 15th January, the group released a statement covering trading in the majority of Q3. As anticipated, shipbroking performance improved significantly compared to the first half of the year, reflecting the inclusion of ACM and the cost reduction actions taken as the business has been integrated. The merging of the two broking teams continued in line with their plans and the board are encouraged by the progress made. The weak oil price seems to have had a positive effect on Braemar as freight rates have increased and demand for oil tankers have increased. The logistics and technical divisions performed in line with expectations with continued improvement in the freight forwarding business and a strong performance from Braemar Engineering. The full year outlook remains unchanged so overall a decent update.

On the 28th January the group announced that it had sold its freehold headquarters in Marylebone to Greenhouse Sports Ltd for £9.5M, a gain of £5.5M over the book value of the property. After the acquisition of ACM, this office no longer has enough space to hold the enlarged staff contingent so they will be moving to One Strand, Trafalgar Square on the 2nd February. This seems like a good price for the building.

On the 2nd February it was announced that Jurgen Breuer, a non-executive director has purchased 5,000 shares valued at £23.3K which nearly doubles his holding to 11,000 shares. There seems to be quite a log of good news flow so I have added to my position here.

On the 2nd March it was announced that Majedie Asset Management, on behalf of their UK Equity Fund and UK Smaller Companies Fund, have purchased 106,952 shares at an approximate value of £500K to give them more than 5% of the total company. This seems like a substantial purchase so it is good to see some confidence from the institutional world!

On the 30th March it was announced that Majedie had topped up a bit more and purchased 24,890 shares at an approximate value of £107K. This now gives them 5.07% of the total share holding.

On the 9th April the group announced some changes to the board structure. After being in the position for 12 years, Graham Hearne is retiring as Chairman to be succeeded by non-executive director David Moorhouse who has been at Braemar since 2005. Denis Petropoulos is stepping down from the board but remaining on as president of Braemar Asia, Johnny Plumb is retiring from the board to focus on his independent consultancy interests and Tim Jaques is retiring having served as non-executive director of ACM since 2010. In addition, Finance Director Martin Beer is also stepping down in order to spend more time travelling with his family. He will be succeeded by Louise Evans who was formerly Finance Director at Williams Grand Prix. In other news, the integration of Braemar and ACM is now largely complete which I suppose is why there is such upheaval at the board level at the moment.