Brooks MacDonald has now released their final results for the year ended 2016.

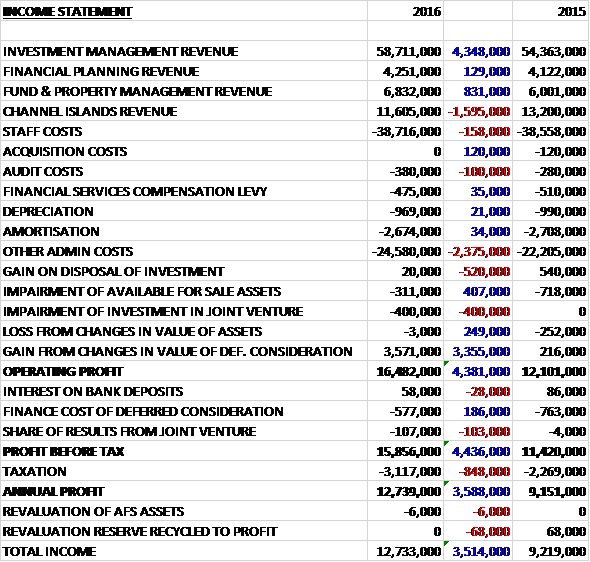

Revenues increased when compared to last year as a £1.6M decline in Channel island revenue was more than offset by a £4.3M growth in investment management revenue, an £831K increase in fund and property management revenue and a £129K growth in financial planning revenue. Staff costs increased by £158K and other admin costs were up £2.4M. There was also a £400K impairment in a joint venture relating to the investment in North Row Capital which was offset by a £407K reduction in the impairment of available for sale assets relating to the Student Accommodation Fund. We also see a £520K decline in gains on investment disposals as the disposal of Sancus Holdings was tied up, offset by a £249K reduction in losses from changes in asset values and a £3.4M increase in the gain from changes in the value of deferred consideration which meant that the operating profit grew by £4.4M when compared to 2015. The finance cost of deferred consideration also reduced, down by £186K, but tax charges grew by £848K, mainly due to under provision in previous years, which meant that the profit for the year was £12.7M, an increase of £3.6M year on year.

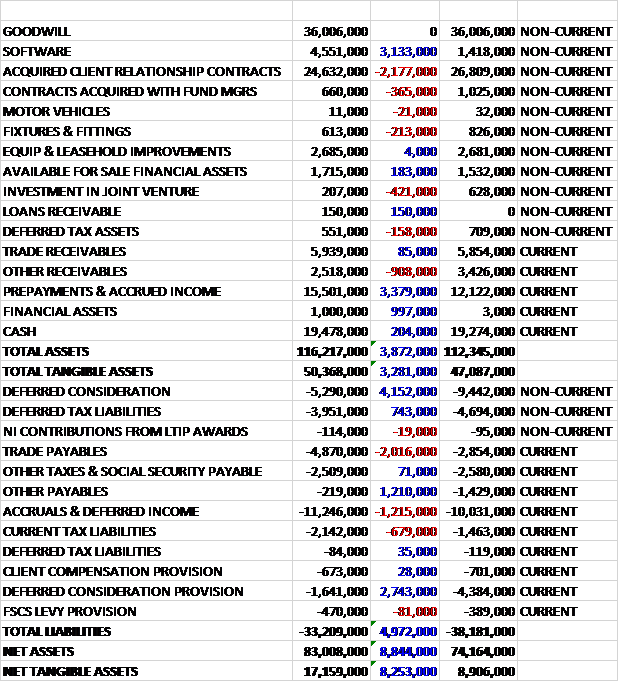

When compared to the end point of last year, total assets increased by £3.9M driven by a £3.4M growth in prepayments and accrued income, a £3.1M increase in the value of software and a £997K growth in financial assets, partially offset by a £2.2M decline in acquired client relationship contracts and a £908K reduction in other receivables. Total liabilities declined during the year as a £2M growth in trade receivables and a £1.2M increase in accruals and deferred income were more than offset by a £6.9M decline in deferred consideration and a £1.2M fall in other payables. The end result was a net tangible asset level of £17.2M, a growth of £8.3M year on year.

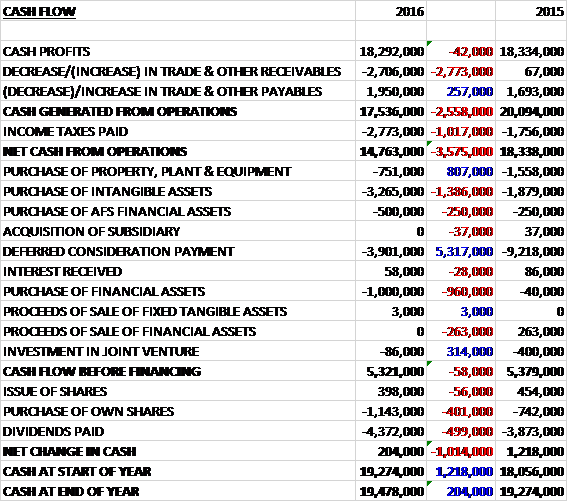

Before movements in working capital, cash profits remained broadly flat at £18.3M. There was a cash outflow from working capital, however, and tax payments increased by £1M to give a net cash from operations of £14.8M, a decline of £3.6M year on year. The group spent £3.3M on intangible assets, £751K on property, plant and equipment, £500K on available for sale financial assets, £1M on other financial assets and £3.9M on deferred consideration to give a free cash flow of £5.3M. Of this, £4.4M was spent on dividends and £1.1M on their own shares to give a cash flow for the year of £204K and a cash level of £19.5M at the year-end.

The profit in the Investment Management business was £17.8M, a growth of £2.1M year on year. The discretionary funds under management rose to over £8.3BN, an increase of £880M. This represents an increase of 12% of which 11.7% was new business and 0.3% investment growth. Growth was largely generated internally, predominantly via their work with professional introducers. The group continue to work with an increasing number of professional intermediaries.

The bespoke discretionary portfolio service now manages over £6.4BN and pension funds along with ISA portfolios remain a substantial growth opportunity here. The managed portfolio service saw assets exceed £617M and the board view this as a strong area of growth. The financial planning business continued the trend of the prior year. Consulting work rose while employee benefits had a difficult year. Work generated into the investment management business remains robust and they will be looking to launch a pension default fund for employee benefit clients early in the next year.

The loss in the Financial Planning was £60K, an improvement of £8K when compared to last year. Numbers of clients increased over the course of the year and the division remains a major introducer of new investment management funds to the group. During the year there was a further investment in systems and staff which meant that despite the small increase in revenues, there was not much of a movement in profits.

The loss in the Funds and Property Management business was £624K, an increase of £60K when compared to 2015. It has been a year of growth for the business across the range of funds it manages. Total Funds under management increased by 20% to £796M with the growth achieved both organically and through new investment into the funds with particularly strong flows into the multi asset funds.

The Ground Rents Income fund performed well during the year with an increase in the net asset value. It was the intention to launch two further property related funds in the second half of the year but due to the Brexit result, these were postponed and will be reviewed again next year. As mentioned below, the group incurred a £400K impairment charge on the investment in North Row Capital along with a £100K share of losses in the business.

The estates business had an improved year although the value of assets under management marginally declined to £1.1BN. Following a review of the business and some changes to the board, additional revenue streams were identified which saw an increase in turnover of 9% over the previous year despite the fall in the value of assets under management. As a result the estates business broke even for the year compared to a £400K loss last year.

The profit in the International business was £453K, a decline of £862K year on year. The business saw an increase in FUM during the year of 16% to £1.35BN with new business from a number of sources and new jurisdictions including South Africa and the conversion of previously non-managed advisory and execution clients.

The planned conversion of advisory accounts to discretionary accounts saw a significant reduction in the transactional income of the business with total revenues falling by 12%. Whilst the associated costs of the advisory clients have been reduced, these have not matched the timing of the loss of revenue together with the increased legal fees in the year, particularly dealing with some legacy issues prior to the acquisition hence the fall in profit.

The growth in the FUM and the expanded sources of international introductions together with the further rationalisation of the core client proposition in line with that offered in the UK means that the board believes the business will see an increase in profit in the next year.

Regulatory changes continue with a major focus on MiFID II. This has been postponed until January 2018 but the group are ensuring the business is well prepared for the substantial changes around transaction and client reporting.

The Brexit vote had an effect on results. In the first half the group decided to postpone the launch of two funds. In the second half, investment returns were challenging and in Q4 investor sentiment was weaker. Markets have improved since the referendum vote but sentiment remains volatile.

The group have continued with their IT system development with three external providers. The time scale for completion has now moved out to mid-2017, but this still remains on budget. In addition they have completed their brand refresh which modernises the look and feel of the marketing and has firmly positioned the business as an investment management business as this remains the key driver for growth. As such, they will be moving their funds and UK asset management business into one brand, Investment Management in early 2017.

The Student Accommodation Fund is promoted by the group. The shareholders of the fund approved a resolution in May to sell the underlying property portfolio to a third party. The shares will subsequently be compulsorily redeemed out of the remaining net assets of the fund following the sale, although the process had not been completed as of the year-end. The group has therefore estimated the fair value of the group’s investment at £471K based on the most recent information made available to investors. This has given rise to an impairment loss of £311K during the year.

During the year the group acquired 500,000 redeemable preference shares in an unlisted company at a cost of £500K. The shares are redeemable any time after five years from the date of issue and bear an entitlement to a fixed preferential dividend of 8% per annum of the nominal value of the shares.

An impairment loss of £400K was recognised during the year to reduce the carrying amount of the group’s investment in North Row Capital to its estimated recoverable amount. Based on the most recent forecasts, the future cash flows from the partnership will accumulate slower than originally anticipated and as a result it will take longer for them to realise a cash return on the investment in the joint venture.

Payments totalling £3.9M were made relating to deferred consideration which included the final payment of £524K to the vendor of JPAM, the final payment of £2.1M to vendors of DPZ and a further payment of £1.2M to the vendors of Levitas. There was an adjustment to reduce the fair value of deferred consideration in respect of Levitas by £3.3M. The amount payable is based on the incremental growth in FUM of the TM Levitas funds. As forecast growth was not achieved during the year, it was subsequently revised and the estimated future deferred consideration payments reduced accordingly. Adjustments were also made to reduce the fair value of deferred consideration attributable to DPZ by £225K and JPAM by £3K.

After the year-end the group disposed of its entire holding of GLIF shares for proceeds of £735K, representing a realised loss on disposal of £15K. The sale of the underlying property portfolio of the Student Accommodation Fund completed in July. The final net asset value of the fund had not been determined at the date of signing these financial statements but is expected to be available by the end of September with the final payment of the redemption monies expected in October 2016.

Going forward the group have made a good start to the new financial year with further organic growth in discretionary FUM.

At the current share price the shares are trading on a PE ratio of 27.5 which falls to 18.4 on next year’s consensus forecast. After a 15% increase in the total dividend, the shares are yielding 1.7% which increases to 2.2% on next year’s forecast. The group has no borrowings so had net cash of £19.5M at the year-end compared to £19.3M at the same point of last year.

On the 20th October the group released a funds under management statement for Q1. As of the period-end discretionary funds under management totalled £8.922BN, an increase of 7.5% in the quarter compared to the WMA balance index which increased 5.2%. This growth was a combination of new business (£170M) and the performance of the funds (£451M).

Notwithstanding potential market volatility, the board look forward with confidence as they continue to leverage the growing strength of the brand, investment offering and professional intermediary relationships.

On the same date the group announced that Caroline Connellan will be joining the group as CEO. She was most recently head of UK Premier and Wealth at HSBC. Chris Macdonald will remain with the group in his current role of CEO becoming Deputy Chairman with effect from April. It is the intention of the board that Chris will become Chairman in the future.

On the 26th January the group released a half year trading update. Over the last six months discretionary funds under management have risen by 12.4% to £9.33BN. This is compared to a rise in the WMA balanced index of 7.8% with increases seen across asset management, funds and international.

Net organic growth over the period was 4% against a backdrop of uncertainty following the Brexit vote and later surrounding the implications of a Trump presidency. These outcomes dented client sentiment and whilst portfolios have performed well, the board expect market volatility to remain. The group have continued to progress as planned with their IT system development whilst pursuing the core strategy of growing the business organically and trading in the first half is in line with management expectations.

Overall then this has been a decent performance for the group. Profits increased but this was due to changes in deferred consideration so without this, profits were flat. Net assets increased but the operating cash flow reduced. This was due to working capital movements, however, and without this cash profits were broadly flat with a decent amount of free cash being generated.

The Investment Management business has been the driver for growth with funds under management increasing due to new business. Financial planning saw no movement in its slightly loss making position as increased investment matched the revenue growth. The funds business saw losses widen, mainly as a result of the North Row impairment and loss for the year but the international business saw the biggest deterioration in performance due to the move of clients from advisory to discretionary products and increased legal fees due to a legacy issue.

The Brexit vote makes the market more volatile that it would otherwise been and so far this year there has been decent organic growth. With a forward PE of 18.4 and yield of 2.2% these shares are not cheap so it seems we are paying for quality. Tricky one this, overall I think the price is probably justified despite the market uncertainty.