Cambria Autos has now released its final results for the year ended 2016.

Revenue increased when compared to last year with a £59M growth in new car revenue, a £28.3M increase in used car revenue and a £4.9M growth in after sales revenue. Cost of sales also increased to give a gross profit £7.5M higher than in 2015. Staff costs increased by £3.1M and other admin expenses were up £1.6M but the group made £2M on the sale of businesses so the operating profit grew by £4M. Interest costs reduced slightly but tax charges grew by £883K to give a profit for the year of £9.3M, a growth of £3.2M year on year.

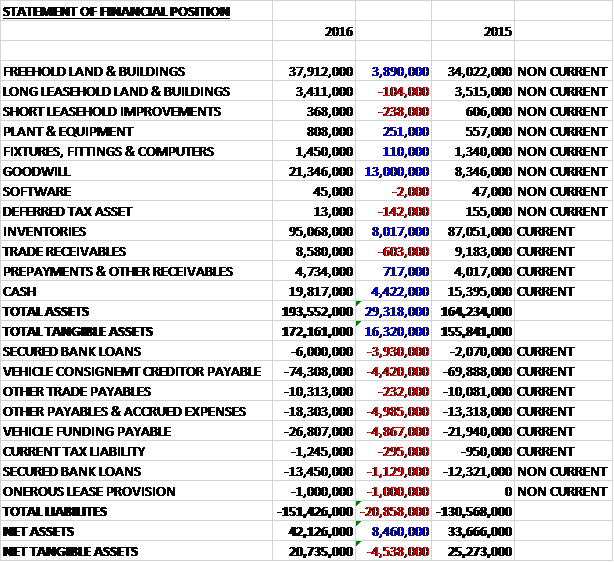

When compared to the end point of last year total assets increased by £29.3M driven by a £13M growth in goodwill, an £8M increase in inventories, a £4.4M growth in cash levels and a £3.9M increase in the value of freehold land and buildings. Total liabilities also increased due to a £5M growth in accrued expenses and other payables, a £4.9M increase in vehicle funding payable, a £4.4M growth in the vehicle consignment creditor payable, a £5.1M increase in secured bank loans and a £1M onerous lease provision relating to the JLR dealership acquired in Woodford. The end result is a net tangible asset level of £20.7M, a decline of £4.5M year on year.

Before movements in working capital, cash profits increased by £3.9M to £14.1M. There was a cash inflow from working capital due to an increase in payables and after tax payments increased by £922K and transaction costs grew by £730K, the net cash from operations came in at £16.7M, a growth of £1.7M year on year. The group spent £5.6M on property, plant and equipment along with a net £10.9M on new branches to give a free cash flow of just £464K which didn’t cover the £800K dividends. After new loans were taken out, the cash flow for the year was £4.4M and the cash level at the year-end was £19.8M.

During the year the like for like businesses contributed a £9.1M pre-tax profit, an increase of 28% year on year.

The gross profit in the New Car business was £19.3M, a growth of £3.8M year on year. On a like for like basis, new volumes rose by 2.9% and gross profit by £1.5M with an improvement in the gross profit per unit sold. This performance was delivered against an overall year on year increase of 3.9% in new UK car registrations, so slightly below the market although the private registrations element of the new car market increased by just 1.7% year on year. Including acquisitions, the sale of new vehicles to private individuals was 7.6% higher; fleet car and commercial vehicle sales increased by 6.9% and 32.5% respectively which has had a dilutive effect on overall new car gross margin.

The gross profit in the Used Car business was £23.7M, an increase of £2.9M when compared to last year. Like for like volumes were up 3.4% and like for like gross profit grew by £2.5M. The group has adopted a trading strategy which involves applying consistent controls to the level of used car stock being held, the pricing and presentation of the inventory and the penetration of finance and insurance products to the sale of used cars. The adoption of this trading style has resulted in the average gross profit on each unit increasing by 8.1% to £1,508 per unit.

The gross profit in the Aftersales business was £26.6M, an increase of £800K when compared to 2015 although like for like profit was flat despite a 1.9% increase in revenues. The aftersales margin was slightly diluted as the parts component of the revenue increased in mix terms. The margin in the parts element is smaller than that generated by service and bodyshop labour sales. The 0-3 year car parc continues to be replenished, as new car sales increases year on year and this gives the group confidence of further progress in guest relationship and retention and the aftersales business remaining strong.

During the year the group was partially through the building project related to its JLR dealership in Barnet and there is a further £4.1M of contract sum payments to be made under the terms of the agreement with the main contractor. The site should be complete in Q1 2017.

In January the group acquired a Land Rover dealership in Welwyn Garden City from Jardine for a consideration of £10.8M, generating £10M of goodwill. The business currently operates from leasehold premises under a short lease agreed with the vendor of the business. The existing Jaguar and Aston Martin businesses in Welwyn are located two miles from the Land Rover dealership. The group has agreed terms to acquire a freehold plot of land in the town to build a new facility for JLR and Aston Martin. The expected capital cost is £16M and the building will be completed in Q2 2018. The development will be funded through the existing revolving capital facilities and new term debt secured against the freehold of the property.

In July they completed the acquisition of the Jaguar and Land Rover dealership in Woodford from Pendragon for a cash consideration of £2.1M, generating goodwill of £3M. On assessment of the lease liability associated with the showroom premises in Woodford, the board made a £1M onerous lease liability which increased the goodwill (again showing what a ridiculous asset goodwill is). Since their acquisition, these businesses have contributed £631K to pre-tax profit.

In May the group opened the Aston Martin dealership in Solihull operating from a temporary facility. In order to secure the franchise for the territory, they acquired a freehold property and invested in a refurb of the facility while the permanent location in procured and built. The temporary facility has incurred a total spend of £1.6M and they are in advanced negotiations to secure some freehold land to build a new facility over the next two years. It is anticipated that the total investment in the permanent facility will be about £4.5M and on relocation of the business, the group intends to sell the temporary freehold property.

Following the Land Rover acquisition in Swindon last year, the group intends to redevelop its Swindon Motor Park location to provide a new JLR facility in line with the new brand requirements. It is expected that development will be completed in Q4 2017 and the planning and design processes are progressing well. Once the new development is complete, they will relocate the Land Rover business from the existing dealership property in Wootton Bassett. The expected investment in the site is £6M which will be funded from the facilities arranged in November 2015.

Overall then the group is investing £30.6M into these franchises of the next two years which is quite a considerable investment.

During the course of the year the group sold the Exeter and Croydon Jaguar businesses to the Land Rover franchise holder in each of those territories, realising a non-recurring income of just under £2M. These were positive earnings contributors to the group’s underlying performance in recent years so a bit of a shame but I doubt there is much they could have done to prevent the sale.

After the end of the year in late October the Welwyn Garden City Jaguar dealership workshop suffered fire damage. They are in the process of dealing with the aftermath of the fire which will impact the trading of the site for about four months while it is rebuilt and refurbished. They are working closely with their insurers to mitigate the financial impact on the group and don’t currently expect that these will be material.

Apparently it remains too early to assess the full implications of the Brexit vote but the economy is entering a period of uncertainty and sterling has depreciated considerably against the Euro which could impact the strategy adopted by the manufacturers of targeting the UK. The latest SMMT forecasts for new car registrations in 2017 show a 5% reduction on the 2016 closing forecast and from April to October 2016 there was a 2.7% year on year reduction in the private segment of the new car market. After the period-end in the important plate change month of September, trading was in line with expectations but October trading showed some softening in new car margins.

The group has a net cash position of £400K compared to £1M at the end of last year, although I suspect this is flattered somewhat by the timing of the year-end. At the current share price the shares are trading on a PE ratio of 8 which falls to 7.3 on next year’s consensus forecast. After a 20% increase in the total dividend, the shares are yielding 1.5% which increases to 1.6% on next year’s forecast.

On the 19th December it was announced that non-executive director Michael Burt sold 500,000 shares at a value of £285K. Apparently this decision to sell relates to a one-off change in his residential tax status and he has no plans to sell any more shares for the time being.

On the 4th January the group released a trading update. They have maintained the momentum from the results delivered last year and their trading performance in Q1 has been ahead of Q1 2016 on a total and like for like basis. After a strong September, there was some pressure on new car margins in October and on volumes in November. New vehicle unit sales for Q1 were down 9.4% on a like for like basis (0.7% total) but gross profit per unit improved in the group’s like for like businesses.

Used vehicle sales performed well with unit sales 2.5% ahead on a like for like basis and gross profit per unit continuing to increase. This performance has enhanced the profit from the used car segment of the business. The aftersales operations increased revenue by 13% (like for like 2.9%) with profitability up 6% but down 1.5% on a like for like basis, impacted by the fire at the Welwyn Garden City JLR workshop.

The board continues to believe that there may be some pressure on new car volumes and margins in 2017 as a result of the uncertainty in the economy and the forex volatility witnessed recently. The group’s trading performance in Q1 means that they are trading in line with market expectations for the full year, however.

Overall then this has been a decent year for the group. Profits increased as did the operating cash flow, although virtually all of this cash is ploughed back into the business (not necessarily a bad thing). The net tangible asset base did fall though due to the cash being spent on goodwill. Over the year new car profits grew, as did used cars which were helped by increased margins. The after sales business was flat however, due to lower services and body shop work.

The group is investing a lot into its existing franchises over the next two years – predicted to be about £30.6M over that time frame. This investment seems to be in response to requirements from JLR and is a substantial amount for a company of this size and adds some risk. The sterling depreciation is not helpful to the group as it makes the UK less attractive to foreign car makers and it is clear that the Brexit vote has caused some turbulence in the car market. So far this year, sales seem to be as expected with used car sales continuing to do well and new car sales dropping off a bit and aftersales being affected by the fire in Welwyn.

Going forward, the group are expecting 2017 to see pressure on volumes of new car sales and now doesn’t really seem to be the time for investing in businesses like this. With a forward PE of 7.3, however, quite a lot of this risk is already priced in so I’m caught in two minds over this one…

On the 7th March the group released a trading update covering the first five months of the year. They have maintained their momentum from the strong results delivered in the last year and the trading performance so far this year has been substantially ahead of the corresponding period last year. Used vehicle sales continued to perform well, with unit sales 0.6% ahead of the same period in the prior year while gross profit per unit continued to increase which has enhanced the profit from the used car segment.

The aftersales operations increased revenue by nearly 12% (like for like 2.6%) with profitability up by 3.8 Year on year (although like for like profits were down 2%), impacted by a fire in October at Welwyn Garden City Jaguar and Aston Martin which continues to affect the business. There will be a business interruption insurance claim which has not been reflected in this update.

Whilst new vehicle unit sales were down 2.9% (like for like down 11.1%) the gross profit per unit improved and the gross profit in this market also improved. Heading into the important March trading period, the new car order book is building well and is in line with expectations.

The board continues to believe that there may be some pressure on new car volumes and margins in 2017 with the current macroeconomic uncertainty in the economy. The group’s trading performance in the first five months of the year indicates that they are trading in line with market expectations, however, which already reflect these uncertainties.

Overall this seems OK, there is a big fall in new car like for like sales but aftersales continue to do OK – tricky one this, I will probably hold off.