Circle Oil has now released its final results for the year ending 2014.

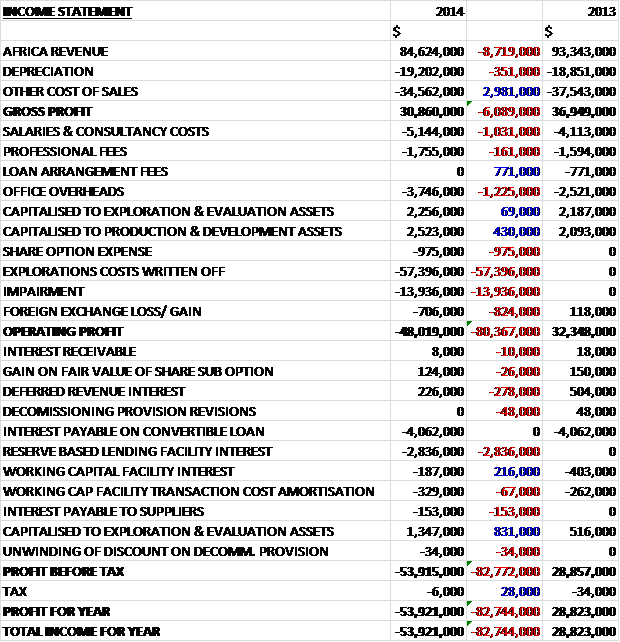

When compared to 2013, revenues fell by some $8.7M, mainly due to the lower price of oil but there was also a small decline in volumes in Egypt, and with cost of sales also declining gross profit was $6.1M lower at $30.9M. We then see staff and consultancy costs increase by $1M and office overheads up by $1.2M. The real damage was done by the one-off charges, however, with $57.4M of exploration costs written off due to the withdrawal from Oman and the expiration of the license at the Grombalia block in Tunisia; and impairments of $13.9M relating to the assets in Egypt due to the lower oil price environment, which meant that operating profit was $80.4M worse than last year. As far as finance costs are concerned, we see a $2.8M interest charge from the reserve based lending facility somewhat offset by an $831K increase in the amount of interest capitalised to exploration and evaluation assets. A negligible tax bill then meant that the loss for the year was $53.9M, a reversal of $82.7M year on year.

When compared to the end point of last year, total assets increased by $6.3M driven by a $51.7M increase in African exploration assets, an $8.4M growth in cash and a $2.5M increase in production and development assets, partially offset by a $35.7M decline in Middle East exploration assets, an $11.9M fall in trade receivables as the balance receivable from EGPC reduced considerably, and a $10M decline in restricted cash. Liabilities also increased during the year as a $30.9M increase in bank borrowings, a net $2.3M growth in the convertible loan and a $26.3M increase in trade payables was partially offset by a $1M fall in deferred revenue to give a net tangible asset level of $95.4M, a collapse of $68.1M year on year.

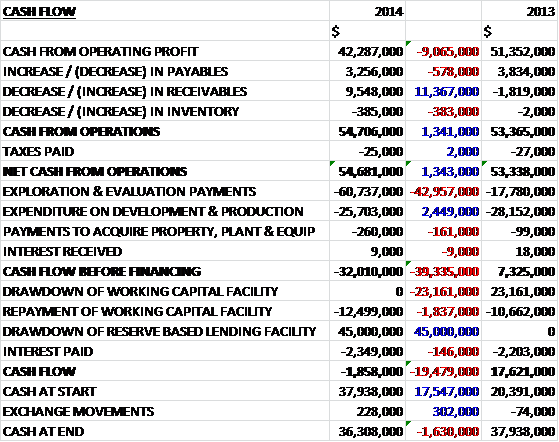

Before movements in working capital, cash profits fell by $9.1m to $42.3M. Favourable movements in both payables and receivables, however, mostly relating to the cash receipts from EGPC which were overdue (the receivable from this client is now expected to remain at a similar level going forward), meant that the net cash from operations came in some $1.3M higher at $54.7M. This partially covered the expenditure on the producing assets but was no-where near enough to cover the expenditure on the exploration assets so that before financing there was a cash outflow of $32M with the drawdown of a new reserve based lending facility meaning that for the year as a whole the cash outflow was $1.9M to give a cash pile of $36.3M at the year end.

Overall, the stable gas price in Morocco means that the country is a priority going forward and the group is keen to boost reserves through the ongoing drilling campaign with some potential new customers in the Atlantic Freeport near Kenitra a possibility. Two discoveries in the Sebou concession added over 6.5 bcf to the reserves during the year and these wells will be put into production shortly. The 2015 drilling campaign in both the Sebou and Lalla Momouna blocks is well under way and the rig has moved to Lalla Mimouna after the third well was completed. In Egypt, two further producers and one water injectors were added to arrest the inevitable decline in production from the mature Al Amir SE and Geyad fields.

The low oil prices have impacted the group quite hard especially considering the cost overruns on both the Mahdia block and block 49 in Oman and in order to remain competitive a strategic review of the cost base and funding options is underway. The average price achieved in Egypt was $94.8/bbl against $104.4/bbl last year and in Morocco the group achieced $10.12/Mscf against $10.34/Mscf in 2013 with the fall in that country attributable to the weakening of the Dirham against the US dollar.

At the end of the period, proved and probable (2P) oil and gas reserves showed NW Gemsa in Egypt as having 26.19 gross MMbo of oil, an increase of 1.83 MMbo with 29.17 bcf gross of gas, a fall of 2.09 bcf, both due to revisions. In Sebou in Morocco, gross gas reserves came out at 27.88 bcf, an increase of 4.42 bcf, mainly due to new discoveries, and in Oulad N’Zala in Morocco, the gross gas reserves were 1.33 bcf, an increase of 0.2 bcf due to revisions.

In Morocco, gross gas production averaged 6.46 MMscf per day (1,183 boepd), supplying three companies in the Kenitra industrial zone with the largest two customers regularly taking more gas than the minimum contracted. Preparations for the third drilling campaign were completed with the start of well SAH-W1 in May 2014 with the wells planned to add additional reserves with a view to extending the gas supply contracts. The KSR-12 well was drilled into a seismic anomaly next to the KSR-8 Main Hoot production and tested separate accumulation in a downthrown fault panel at a different pressure. This independent gas reservoir has now added additional reserves to the estimate. Also the CGD-12 well was drilled through another separate accumulation in the SW area of the Sebou concession.

In well SAH-W1, three gas bearing zones were encountered at the expected depths but for technical reasons, the rig was released from this site prior to testing and completion so these accumulations have not been included in the latest reserves calculation. During April 2015, however, testing was completed which enabled the well to be added to the production system and following this, the rig was moved to the Lalla Mimouna block to start drilling an initial three well programme. For the Oulad N’Zala concessions, the 2P value of gross estimated recoverable gas reserves is 37.14 bcf (6.4 MMboe) with 27.5 bcf net to Circle, a 23% increase over the prior year report. The 2P gross remaining reserves are estimated to be 29.21 bcf (5.04 MMboe) with 21.71 bcf net to the group, a 19% increase on last year’s report.

In Egypt, the NW Gemsa concession contains the AASE and Geyad fields where gross production averaged 10,026 bopd and 10.6 MMscf per day. Development drilling continued to May 2014 with two producers and one injector in AASE. The gas export line to the SUCO facilities in Zeit Bay has allowed for produced wet gas to be processed as dry gas with the additional benefit of extracting condensate and LPG at the terminal which has been ongoing since early 2013. Appraisal production well AASE-19, infill production well AASE-21 and the water injector AASE-22 were completed during the year which concluded the initial field development programme with the rig being farmed out to another operator for a year or so.

During the year, field operatorship at NW Gemsa changed from Vegas to North Petroleum and development drilling is planned to resume during H2 2015. Average daily production in the new-year to May was is 8,236 bopd with 3,294 net to Circle and 9.32 MMscf per day of gas with 3.73 net to the group.

At the start of the year the group had interests in two exploration licenses in Tunisia: the offshore Mahdia permit and the onshore Ras Marmour permit with an application for an exploration permit for Takelsa under negotiation. In addition, an agreement with Exxoil, the operator of the Beni Khalled production concession made Circle a partner in this lease subject to fulfilment of an agreed work programme of seismic and a well. The field is currently producing less than 100 bopd compared to some 550 bopd ten years ago. Activity during the year included the drilling of an exploration well in the Mahdia block and seismic survey planning in Beni Khalled.

The El Mediouni well in the Mahdia permit commenced in June and was suspended in September having encountered light oil shows through a 133 metre section of Ketatna carbonates. Massive mud losses occurred and despite multiple attempts to restore circulation, the hole conditions deteriorated and no open-hole logging was possible. Although this was a disappointing result, the well proved both a petroleum system and a reservoir on the block and with an application to enter the next exploration phase awaiting formal government approval, efforts to farm-out an interest in the block with re-commence in later in the year.

At the start of the year, the group operated onshore exploration block 49 and offshore exploration block 52 in Southern Oman. The infill 2D marine seismic survey acquired during the year was processed and interpreted for the inshore area of Sawqirah Bay in block 52. The group also drilled onshore exploration well Shisr-1 in Q1 2015 in the SW area of block 49 but the decision was taken to plug and abandon the well due to drilling difficulties and no hydrocarbons were detected. As part of the review of the cost base, given the insufficient interest in a farm-in of block 52, Circle decided to relinquish both blocks and exit Oman completely. Once the restoration of the drill site on block 49 is complete and all relevant data has been submitted to the Ministry, the offices in Oman will be closed and the group will no longer bid for new acreage in the country. As a result, the group’s investment in Oman has been written off.

Trying to keep track of Circle’s various funding facilities is quite a challenge. After the year-end the convertible loan was amended with the group paying $10M by July (so far $6M has been paid off) with the remaining $20M being extended until July 2017 and an increase in the interest rate from 6% to 8%. During the year the group also signed a reserved based lending facility of up to $100M with IFC with a maturity date of June 2018. As of the end of December, the total loan amount committed was $75M with the maximum available amount being $66M and the total draw-down was $45M with a further $12.5M being drawn down after the year-end.

Going forward the group is planning further infill drilling in Egypt during the year with three new production wells in 2015 aimed at minimising the decline in production rates, and to continue the drilling programme on the Sebou and Lalla Mimouna permits in Morocco with at least three wells being drilled in the Lalla Mimouna concession during the year with the aim to increase gas sales this summer. In Tunisia, they are waiting for government approval to proceed to the next exploration phase of the Mahdia permit and will re-start farm out efforts. The drilling of Sedouikech well in the Ras Marmour permit is likely to be undertaken but the final decision will be taken in light of the overall review of the group’s capital expenditure commitments. Overall the board hopes to further increase the gas reserves in Morocco and sustain oil production in Egypt during the year.

During the year Chris Green resigned as CEO and Mitch Flegg was appointed as his replacement from June 2015. He was formerly the COO of Serica Energy and is an operationally focussed executive. Also, Susan Prior was appointed finance director from January. She is a chartered accountant who was formerly at PwC. Additionally there were two new non-executive appointments with Antony Maris, a petroleum engineer currently COO of SOCO International and David MacFarlane, the former Finance Director at Dana Petroleum both bringing significant experience to the group.

As the group made a loss, it is pointless looking at the P/E ratio this year but it is expected to be 18.3 on next year’s (varied) consensus broker forecasts which looks rather rich to me. At the year end the group has available cash of $34.5M and net debt stood at $38.7M but it increased to $59.2M by the end of May 2015.

Overall then this was clearly a disappointing year for the group. Underlying profits fell, there were impairments in Egypt and Oman, net assets declined considerably due to large increases in borrowings and trade payables. Operating cash flow did increase but this was only due to the continued recoverable of overdue receivables from EGPC which will not be repeated going forward and the cash income is not enough to sustain this level of exploration which is why it is a good idea to leave Oman – arguably this was a step to far at the same time as the Tunisian programme anyway. The technical problems on the Tunisian drill is disappointing but the country does hold some promise with Morocco also likely to add to income going forward. Sadly the same cannot be said for Egypt which is an ageing field susceptible to oil price fluctuations. Overall, given the above and the vastly increasing levels of debt I don’t think Circle Oil is a sensible investment at this time.

On the 26th June the group released an update for the LAM-1 well testing. Following the completion of the well on the 26th May, the well was tested using a slick-line unit. The primary target was hit at 1,261 to 1,272 metres and gas flowed at a stabilised rate of 1.9 MMscf/d on a 16/64” choke and the secondary target was hit at 1,181 to 1,183 metres and flowed at a stabilised rate of 1.1 MMscf/d. The rig has now been mobilised to drill the ANS-2 well, the second one of the campaign located on the norther flank of the Anasba ridge with a TD of 1,062 metres.

It is good to finally get some good news from the company, I think that Morocco always was the most likely to provide good results.

On the 14th July the group announced that it had completed the ANS-2 exploration well in Morocco. Although the well encountered gas shows whilst drilling at the targeted depth, the interpretation of the wireline logs indicates that the reservoir quality encountered at the well has not met the pre-drill estimates. It has therefore been suspended pending further analysis of all the data before a decision is made regarding whether or not to complete the well. The rig is now being mobilised to drill the NFA-1 exploration well, the third in the drilling campaign on Lalla Mimouna. This well is targeting two potentially gas-bearing zones in the Miocene sands which exhibit strong seismic amplitude anomalies, attributed to gas filled porous sands.

On the 3rd August the group released an update covering the NFA-1 exploration well on the Lalla Mimouna permit, onshore Morocco. The TD of the well, at 1,077 metres, was reached on the 26th July. The well encountered gas shows whilst drilling at the targeted depth but the reservoir quality did not meet the company’s pre-drill estimates so the well have been plugged and abandoned. The rig will not be mobilised to drill the Ksiri South exploration well in the Sebou permit which is targeting two objectives in the Miocene Gaddari sands. One of the objectives is to prove up the potential of targets with a significant trapping component which, if successful, will open up a new play type for the Sebou permit. Unfortunately this is another disappointing result for the group.

On the 19th August the group announces that the Tunisian authorities have approved the application to renew the exploration permit on the Mahdia block with an extension running until January 2018. The extension carries with it a commitment for one exploration well, one appraisal well and a requirement to acquire 300km2 of 3D seismic. Given the group’s 100% working interest in the block, they intend to select suitable partners to help evaluate and develop the prospects on the permit. There have apparently already been initial expressions of interest from a number of oil and gas companies with the financial strength and experience to make suitable joint venture partners. The confirmation of this extension of the permit will give interested parties greater certainty in making a formal approach and should assist in concluding an agreement.

On the 26th August the group released an update for the KSS-A well which was targeting two objectives in the Miocene Gaddari sands. The well encountered unexpected lithology above the primary objectives and as a result the well has been plugged and abandoned. The technical data from the well in being assessed in line with available seismic with a view to assessing further drilling in the area at a later date.

The rig is now being mobilised to drill the Ksiri West (KSR-A) exploration well in the Rharb basin. The principal target is in the hanging wall of the Ksiri West fault sequence. There are channelised sand bodies within the Main Hoot sequence which display a significant seismic amplitude anomaly found to be caused by gas-filled porous sands in several nearby wells. The event should be a depth of about 1,789 metres and a shallower, smaller, secondary target is recognised in the Miocene Guebbas sands at 1,303 metres. The well has a TD of 1,860 metres.

Oh dear, things are getting a bit desperate here in my view…