Cohort has now released their final results for the year ended 2017.

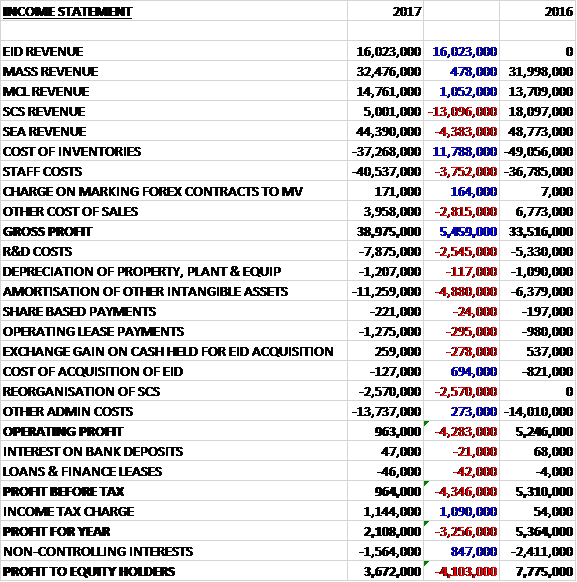

Revenues were broadly flat, increasing slightly as a £13.1M decline in SCS revenue and a £4.4M fall in SEA revenue was offset by a £1.1M increase in MCL revenue, a £478K growth in MASS revenue and a maiden £16M revenue contribution from EID. Cost of inventories declined by £11.8M but staff costs were up £3.8M and other cost of sales grew by £2.8M to give a gross profit £5.5M higher. R&D costs increased by £2.5M, amortisation was up £4.9M, there were a small increase in operating lease payments and £2.6M was spent on the reorganisation of SCS, including a £1M charge for the onerous lease at the former operating site in Theale. Acquisition costs fell by £694K, however, which meant that the operating profit declined by £4.3M. Tax charges fell by £1.1M which meant that the profit for the year was £3.7M, a decline of £4.1M year on year.

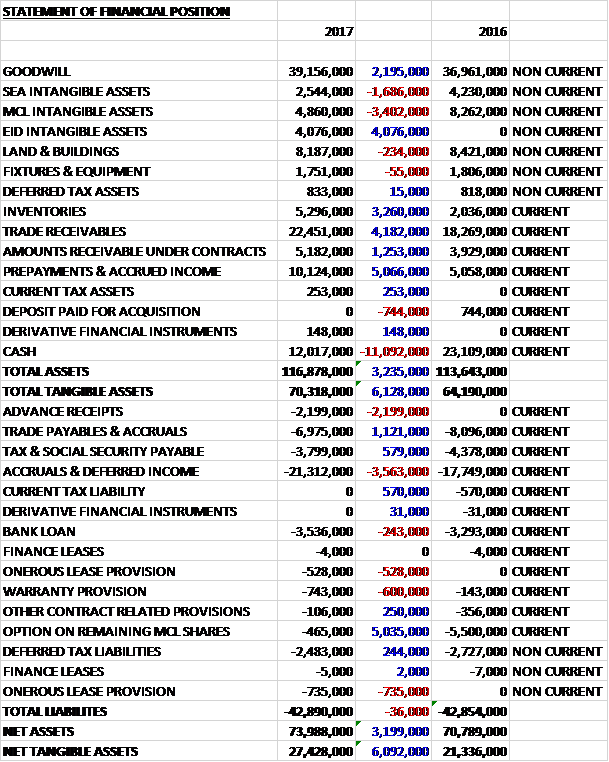

When compared to the end point of last year, total assets increased by £3.2M driven by a £5.1M growth in prepayments and accrued income, a £4.2M increase in trade receivables, a £4.1M increase in EID intangible assets, a £3.3M increase in inventories and a £2.2M growth in goodwill, partially offset by an £11.1M decrease in cash and a £3.4M fall in MCL intangible assets. Total liabilities were broadly flat as a £5M reduction in the option remaining on MCL shares was offset by a £3.6M growth in accruals and deferred income and a £2.2M advance receipt. The end result was a net tangible asset level of £27.4M, a growth of £6.1M year on year.

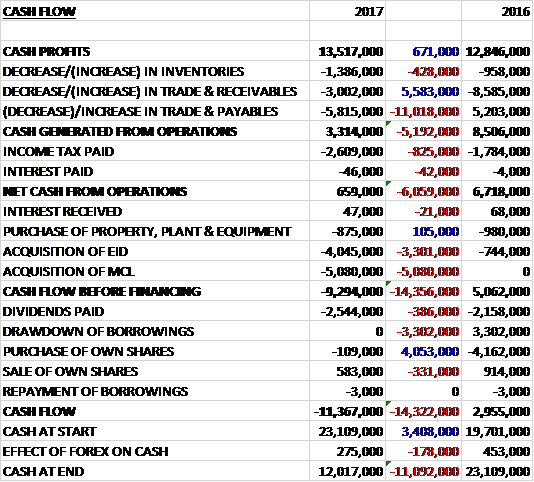

Before movements in working capital, cash profits increased by £671K to £13.5M. There was a big cash outflow from working capital, however, and after tax payments increased by £825K the net cash from operations was £659K, a decline of £6.1M year on year. The group spent £875K on capex, £4.1M on the EID acquisition and £5.1M on the acquisition of MCL shares so before financing there was a cash outflow of £9.3M. The group spent £2.5M on dividends and after some movements in shares the cash outflow for the year was £11.4M and the cash level at the year-end declined to £12M.

EID contributed a maiden £4.2M operating profit to the group, although the group is only entitled to 57% (£2.4M) of this. This represented a contribution for the ten months since acquisition which exceeded expectations in Euro terms and was further enhanced by the weak sterling. The business saw a significant level of higher margin naval support activity, for both domestic and export customers. The tactical division, where it delivers mostly off the shelf products, delivered on a significant contract for the Egyptian Army.

The combination of this support activity and higher volumes of export product deliveries drove an unusually high net martin of over 26%. The business has secured nearly £19M of orders since joining the group which included over £8M from the Portuguese MoD and follow on orders from Egypt of nearly £1.5M. The closing order book of £27.6M gives a good underpinning for the coming year and some very good prospects, especially in naval systems, are expected to add to this so the board expect revenue to grow in the coming year. The mix of work is expected to change, however, with lower levels of support activity which means the net margin is expected to return to historic levels.

The operating profit at MASS was £5.9M, broadly flat year on year with a decline of just £48K despite this year including £500K of profits from SCS’s former training support division which transferred to MASS in November. Like for like revenues declined as a low margin, non-core service they had provided for many years was halted. This was combined with an increase in overheads, partly as a result of one-off costs and partly due to business development and project support in the Cyber division.

During the year the business secured a number of significant contracts in the growth areas of secure information systems and cyber. This included the Metropolitan Police Services Digital Forensic managed service for nine years (£8.6M) and a ten year secure information management service for the RAF’s Sentry Platform (£12.5M), the latter being an extension of existing work. The order intake included over £8M of other renewals and extensions of existing work and more is expected in the coming year.

The MPS win opens up a significant new market for both similar and new offerings to other UK police forces as well as overseas customers. The operating cash flow this year was slightly weaker than last with a build-up of working capital at the end of the year linked to higher activity. The business is currently investing in facility upgrades to enable it to offer a more comprehensive cyber service which completed towards the end of the year. The division enters the current year with a strong order book and pipeline of opportunities, including exports, though the latter are always unpredictable in terms of timing.

The operating profit at MCL was £2.1M, a growth of £649K when compared to last year with revenues up 8% mostly due to increased support services for the UK MOD, primarily in the land environment. The business secured a number of orders in the year including a further £15M of hearing protection systems and other equipment development, production and support for specialist military users.

The closing order book of £15.M, up from £7M last time, along with further recent wins of around £6M shows improved visibility and gives the board confidence that the division will continue to grow in the coming year, although they expect margin percentages to be lower due to the level of bought-in content. The small operating cash flow was expected, reflecting their peak of activity at the end of the year.

The operating loss at SCS was £455K, a detrimental movement of £1.7M year on year. There was a steep decline in demand from the UK MOD for the business’ services so it was restructured with the profitable parts being moved to MASS and SEA with the rest being closed.

The operating profit at SEA was £5.3M, a decline of £148K when compared to 2016 reflecting a growth in the transport business offset by a significant contraction in their research activities. The year has seen a reduced predictability of the revenue stream, especially in the software solutions and product division where the timeframe from order win to delivery is usually a few weeks to months. They expect to see this continue in the medium term whilst they await the new major stages of the UK submarine fleet’s external communications system, the Vanguard Class upgrade and the new Dreadnought class. In the meantime the business is seeking to expand their export business, especially in maritime markets.

The maritime business remained steady with the expected decline in the UK submarine communications activity offset by increased delivery of torpedo launcher systems for export customers. The sub communications work has moved from design and testing to delivery. They continue to have good levels of redesign and upgrade work whilst the engineering team await the next major activity on the Vanguard class in the near future.

The level of torpedo launcher activity, as expected, increased as they completed design and moved to the first production systems for two export customers. The level of this activity will be sustained for the coming year and the business is tracking opportunities to win further export orders with the potential to provide growth in 2019 and beyond. In the maritime division, the business suffered project losses on a one-off development project for a specialist sonar array, a contract inherited with the J&S business acquired in 2014. This programme is expected to conclude in 2018 and no further losses are expected.

The Software, Simulation and Product division, increased revenue by around £2M in the year. This growth was mostly from increased orders for enforcement systems in the UK and overseas, as well as an important follow on order for Digital Traffic Enforcement Systems at TFL.

For some years the business has been a provider of research to the UK MOD in the areas of sonar, maritime and land. The former to areas continue to provide revenue streams as well as providing expertise for their development of low profile sonar array systems, now being sold as the Krait array, to a number of customers around the world.

In the land domain, they have led a team of suppliers over a period of eight years on two major research programmes into Dismounted Soldier Systems. The last of those research programmes completed last year. A follow on programme was expected but various internal and budget issues on the side of the customer have delayed it. The timing of the programme remains uncertain and initial work is now likely to be delayed into 2019. The impact of this delay resulted in most of the revenue fall seen in the business.

The subsea division also had a tough year with revenue dropping by a third to £2M as the low oil price continued to hold back spending from oil producers in the North Sea. Despite this, the vision largely maintained its profitability by a combination of some cost reduction, including redeploying staff to support the maritime division and improved gross margin. The latter arose from an increase in the proportion of refurbishment and repair activity.

The business absorbed the former SCS divisions of Capability Development and Air Systems which added £300K of profit to the result of SEA. The closing order book of £44M (£55.6M) includes nearly £24M of revenue to be delivered in the coming year and along with good order prospects, gives the board reasonable confidence that it will return to growth in the coming year.

In January 2017 the group acquired the 50% of MCL it did not already own for £5.1M as per the original sale and purchase agreement in 2014. They are also expected pay £465K earn out in respect of the closing order book at the end of April. In addition, the non-controlling interest is entitled to the cash in MCL which is estimated at just under £2M, which will be paid before the end of July. As of the year-end, the group held 57% of EID and has agreement with the government to acquire a further 23% to take their holding to 80% at a cost of €4.4M. Despite these commitments, the group still expects to grow their net funds in the coming year.

Going forward, recent contract wins have given a positive start to the year and the board considers that the order book (£136.5M compared to £116M, with the increase entirely attributable to EID) and near term prospects provide a good base for future progress.

At the current share price the shares trade on a PE ratio of 45.5, including restructuring but this falls to 14.4 on next year’s consensus forecast. After an 18% increase in the total dividend, the shares are yielding 1.7% which increases to 2% on next year’s forecast. The dividend has been growing faster than earnings in recent years so going forward the board expects the rate of growth to reduce over the coming years to align more closely with earnings growth – I hope they stick to this! At the year-end the group had a net cash position of £8.5M compared to £19.8M at the end of last year.

On the 1st August the group announced that EID had been awarded a contract by the Portuguese Navy for the supply of integrated communication systems to the Tejo Class Coastal Patrol Vessels, worth a total of €4.6M. The contract encompasses the supply of radio equipment, ICCS, integration engineering and logistic services. It also includes additional supplies for the second batch of the Viana do Castelo Oceanic Patrol Vessels currently being built in Portugal.

Further to this, SEA has been awarded a contract by Hyundai Heavy Industries, which around £5M, for the supply of torpedo launcher systems for the SE Asian market. These will be fitted to new ships that HHI are currently building. The system is based on the product in service with the UK Royal Navy and is currently being supplied to the navies of Malaysia and Thailand. The system is unique in that it can be configures to fire any NATO standard light weight torpedo, enabling customers to choose the best weapon independently and to potentially switch during the life of the ship.

Overall then this has been a bit of a mixed year for the group. Profits were down but this was due the increased amortisation following the EID acquisition, along with the recognition of the onerous lease at SCS. Net assets increased and although the operating cash flow declined, this was due to working capital movements and cash profits grew, although no free cash was generated.

The EID acquisition seems to have got off to a flying start, and indeed without it these results would have looked a lot worse. The margins are not going to be as high going forward, but there will be the recognition of more earnings if the further share acquisition goes through. MCL was the other good performer, as they provided more support services to the MOD but again margins are expected to be lower, but all of the earnings will be recorded by the group.

The MASS division was flat, but without the contribution from the old SCS business there would have been a decline in profits as they invest for future growth. The SEA business saw a bit of a disappointing year as research activities declined considerably and the low oil price continued to take its toll. The SCS business performed disastrously and was closed, with the profitable bits moving to SEA and MASS. The shares are not glaringly cheap with a forward PE of 14.4 and yield of 2% but I do feel the company is moving forward, slowly. A tricky one but on balance I remain a holder.

On the 7th September the group released a Q1 update. Import contract awards announced since the final results include EID to supply integrated communications systems to the Portuguese Navy, SEA to provide torpedo launcher systems for the SE Asian market and MCL to supply further hearing protection and communication ancillaries to the UK MOD. Including these wards, the order book stood at £149M at the end of July, underpinning a slightly higher proportion of revenue compared to this time last year. The pipeline of orders and expected renewals give them confidence that the overall performance will be in line with the board’s expectations.

On the 27th November the group announced that it had acquired a further 23% of EID for a cash consideration of €4M which brings the total holding up to 80% with the Portuguese government holding the rest. The group remains on course to meet the board’s expectations for the year.