Compass has now released its interim results for the year ending 2015.

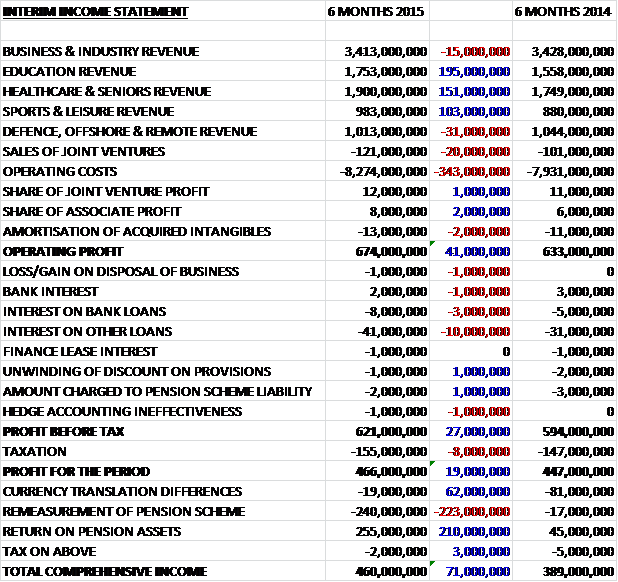

Overall revenues increased when compared to the first half of last year as small declines in offshore & remote, business & industry and joint venture sales were more than offset by good increases in education, healthcare and sports & leisure sales. Operating costs also increased to give an operating profit some £41M ahead. We then see an increase in loan interest and tax so than profit for the period stood at £466M, an increase of £19M when compared to the first six months of 2014.

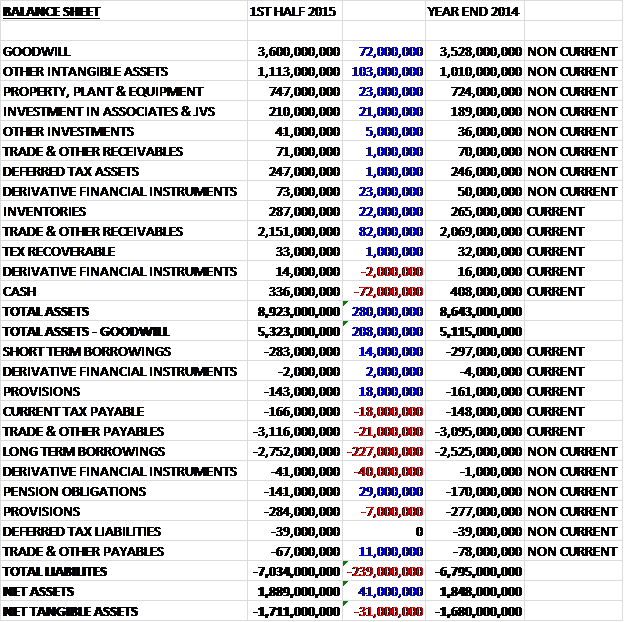

When compared to the end point of last year, total assets increased by £280M, driven by a £103M growth in intangible assets, an £82M increase in receivables and a £72M increase in goodwill, partially offset by a £72M decline in cash levels. We also see liabilities increase due to a £113M growth in borrowing levels to give a net tangible asset level some £31M lower at a negative £1.711BN which doesn’t look too good.

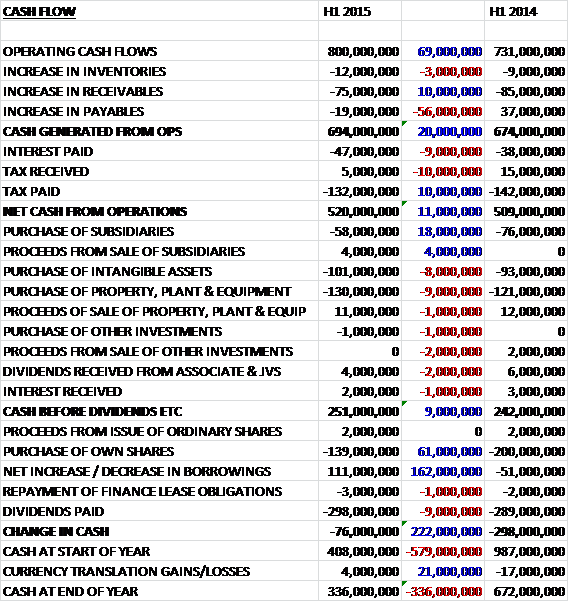

Before movements in working capital, cash profits increased by £69M before detrimental movements in all working capital elements due to the seasonality of the business and investment in emerging markets where working capital is less efficient, meant that cash generated from operations stood at £694M, a £20M improvement. After tax and interest this then became a net cash from operations of £520M. This was more than enough to pay for the £130M spent on tangible assets, the £101M spent on intangibles and the £58M spent on acquisitions to leave a cash flow before financing of £251M. This did not cover the dividend payment of £298M though, let alone the £139M spent on the share buy backs so the group borrowed a further £111M to give a cash outflow for the first six months of the year of £76M to leave a cash pile of £336M.

Overall the retention rate increased to 94.5% due to an unusually strong performance in North America and improving trends in Europe and Japan. Like for like revenue growth was 2.7% which reflects some pricing and modest like for like volume increases and underlying profit increased by 6.5% on a constant currency basis. The group has continued to generate efficiencies by embedding its “MAP” framework deeper into the business with a focus on the cost of food and labour costs but the board believes that there are still further efficiencies to come. Overall there was a 0.6% negative impact on revenues from currency translation as a weakening of Sterling against the US Dollar was more than offset by strengthening against other currencies.

Operating profits in North America increased by £47M to £395M with a margin improving from 8.4% to 8.5%. This reflects some good new business wins with unusually high retention rates, with some like for like volume improvement. Further progress was made on reducing costs whilst at the same time investing in the business to support the organic growth. The Business and Industry sector delivered good levels of new contract wins including Johnson & Johnson, the Culinary Institute of America and the Royal Bank of Canada, along with some improvement in like for like volumes.

In the Healthcare sector, organic revenue growth was good, driven by new contracts with the Vancouver Coastal Health Authority and the Scottsdale Lincoln Health Network. Organic revenue growth in the Education sector included strong new business and increased levels of participation which included contract wins with Hillsdale College and Louisiana State University. The sports and leisure business delivered strong organic revenue growth through excellent contract retention and solid attendance levels at sporting events. The smaller defence, offshore and remote business saw some pressure on organic growth following the recent decline in commodity prices.

Operating profits in Europe and Japan fell by £7M to £206M with an operating margin that improved from 7.2% to 7.3%. Although organic revenue increased, the economic picture in the region remains difficult and despite stabilising, like for like volumes remained negative. There were good levels of new business in the UK, Spain and Japan with improving retention rates across the region. Contracts were won with VW and JLL in the UK, Hospital D. Josep Trueta in Spain and the Rakuten Kobo Stadium Miyagi and GE Healthcare in Japan. Retained contracts included the Wimbledon championships, and ExCel in the UK as well as Disneyland Paris, the Sony head office in Japan and Bosch in Germany. Across the UK, Germany, the Netherlands and Southern Europe, there was an improving trend in like for like volumes but the group continued to experience pressure in France and the Nordic regions, which have an exposure to the oil and gas market.

Operating profits in Fast Growing and Emerging markets were £105M, a decline of just £1M when compared to the first half of last year, although the operating margin fell from 7.1% to 7%. There was a 7.7% increase in organic revenues with strong levels of new business in emerging markets helping to offset the decline in the Australian Offshore and remote sector. In Australia, negative organic revenue reflected the ongoing slowdown in the offshore and remote sector, although other sectors within the country saw good levels of new business and extended contracts including Wesley College, the University of New England and Network Nine. In Latin America, new business wins remained strong with an encouraging pipeline across all countries. New food service contracts included Pepsico and Pirelli in Brazil and a remote site contract with copper miner Codelco in Chile. The business focused on cost efficiencies in the region to mitigate against falling volumes.

Organic revenue growth in Turkey was driven by new business wins which was offset by some declines in like for like volumes driven by challenging macroeconomic conditions. New contracts in the country included the provision of food services to Doga Schools, Cimentas and the Turkish Aerospace Industry, as well as the retention of Mercedes and Goodyear. The Middle East performed well with strong new business wins such as Zadco, Tawam Hospital and the UAE University; and in South Africa the group won contracts with Anglo American and Mondelez as well as retaining business with Microsoft and Mediclinic.

Double digit organic growth in India and China was driven by strong new business wins. In India, the group won food service contracts with the Asian Heart Institute and Ceat Tyres and strengthened their relationship with Reliance Group with additional support services. In China, they extended their relationship with Tencent and won a food service contract with Dulwich College in Beijing. Due to the uncertain macroeconomic environment in some emerging markets and weak commodity prices, the group has experienced some negative like for like volumes and clients looking for costs savings, along with increasing inflation rates. In order to offset these headwinds, the headcount has been reduced in Australia, Brazil and the Turkish food business by 10%, although the long term potential in these markets remains.

There are slightly more capital commitments at the period end than at the same point last year with £203M, mainly relating to intangible assets , compared to £139M. The expectations for the full year remain unchanged but the economic environment in some of the emerging markets is rather uncertain and low commodity prices are impacting the remote and offshore business. The pipeline of new contracts is decent and the board has confidence in delivering another year of progress.

After an 11.4% increase in the interim dividend, at the current share price, the shares yield a decent 2.4%. Net debt stood at £2.655BN at the period end compared to £2.353BN at the start of the year. The share buyback scheme continued during the period and the £500M programme is expected to be completed this year.

Overall this was another solid update. Profits crept up year on year and operational cash flow improved to give a decent amount of free cash, although this was not enough to cover the dividends and share buyback scheme. Net assets fell, however, as borrowings increased to give a very negative net tangible asset level which is somewhat concerning. Operationally the North American business is the star performer, propping up the other more underperforming parts that includes a European market that is still suffering (although slowly improving), and a mixed emerging market outlook with strength in China and India offsetting difficult macroeconomic conditions in Turkey and Brazil and declining commodity prices that have impacted the remote sector in Australia. Going forward, there are apparently further efficiencies to come and a yield of 2.4% is probably just enough to remain interesting. I will continue to hold but I can’t really see much scope for share price appreciation in the short term.

Since April there has been some weakness in the share price although the long term trend still seems to be up.

On the 15th June it was announced that Chairman Paul Walsh purchased 5,000 shares at a value of £55,350 to give him a total holding of 21,411.

On the 29th July the group released an update covering trading in Q3. Overall organic revenues were up 5.5% for the first nine months of the year with growth in Q3 slightly softer at 5.1% reflecting strong net new business in North America, an acceleration of growth in Europe and Japan, and a more subdued environment in both Fast Growing and Emerging and Offshore and Remote. Overall margins have improved by around 5 basis points in the quarter and around 10 basis points for the year to date.

The performance in North America was good with revenue growth of 7% for the quarter and 7.8% for the year to date. Strong growth across most sectors was partly offset by weaker volumes in the oil and gas business. The margin increased by around 5 basis points during the quarter. In Europe and Japan, organic growth was 1.8% during the quarter and 1.2% for the year to date, driven by improving performances in several countries, particularly the UK and Spain. The group continued to deliver efficiencies in the region which improved margins by 10 basis points in Q3. In Fast Growing and Emerging markets, organic revenue grew by 7.4% in the first nine months of the year and by 6.8% in Q3. Revenue growth in emerging markets was around 12% in Q3 with strong rates of new business somewhat offset by weaker volumes in Brazil and Turkey. The operating margin declined by 10 basis points with the ongoing efficiency programme partly offsetting the impact of volume and margin pressures in the oil and gas, and mining client base (particularly in Australia) and soft volume some emerging markets.

If the current spot rates continue for the remainder of the year, foreign exchange translation is expected to negatively impact underlying operating profit by £6M. The share buyback programme is now almost complete with just £25M to be spent going forward.

The group are now proactively reducing the cost base in the offshore and remote business globally, and in some emerging markets. This restructuring plan will cost around £20M to £25M per year in 2015 and 2016. It is therefore expected that 2015 operating margin will be flat year on year and in 2016 the savings, together with margin improvement in the rest of the group, is expected to offset the impact of lower volumes and pricing pressures in the fast growing and emerging region.

Overall the update sounds positive but the restructuring looks like it is going to cancel out much of the improvement in margins already gained. The market did not take too kindly to this update but considering the share price weakness leading up to this, it doesn’t seem all that bad to me. I am quite heavily invested here so I might look to offload some given the headwinds in emerging markets but I am happy to continue to keep my core holding.

On the 13th August it was announced that COO North America Gary Green sold 150,422 shares at a value of more than £1.6M. I feel given this and the latest update along with the poor chart now is probably the time to sell my shares here. I have held them since the financial crisis and have realised a good profit but it is a little sad more me nonetheless and it now leaves me with no investments in the FTSE 100 at all.

On the 1st September it was announced that non-executive director Mr. Silva purchased 8,200 shares at a value of £84K. This is his first share purchase.

On the 24th September the group announced a few board changes. Andrew Martin, COO for Europe and Japan will step down in December and Dominic Blakemore, currently group finance director, will become COO for Europe including Turkey. On the same day, Johnny Thomson who is currently regional MD of the Latin American business will become group finance director and will join the board as an executive director. It is unclear who will be responsible for Japan. Johnny, who is a chartered accountant, joined the group in 2009 as finance director for the Brazilian business. He was then appointed CEO of the Brazilian business before becoming the regional MD in 2014. He joined from Hilton Hotels where he was VP finance for the UK and Ireland division.