Cranswick has now released its interim results for the year ending 2015.

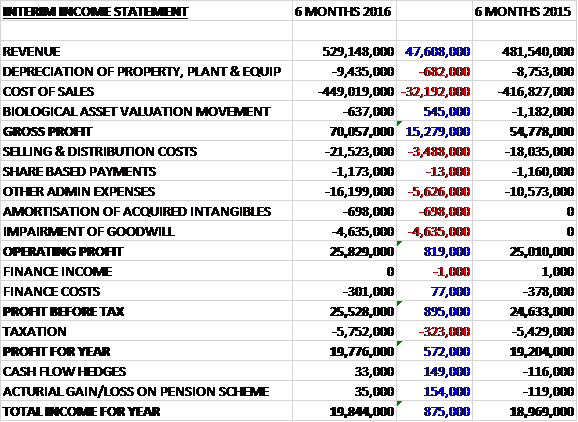

Revenue increased by £47.6M when compared to the first half of last year. Cost of sales also grew which meant the gross profit was some £15.3M above that of last time. Selling and distribution costs increased by £3.5M and admin expenses grew by £5.6M but there was a £700K amortisation of acquired intangibles and a £4.6M impairment of goodwill but despite this the operating profit grew by £819K. Finance costs were slightly lower but tax was higher so that the profit for the half year came in at £19.8M, an increase of £572K year on year.

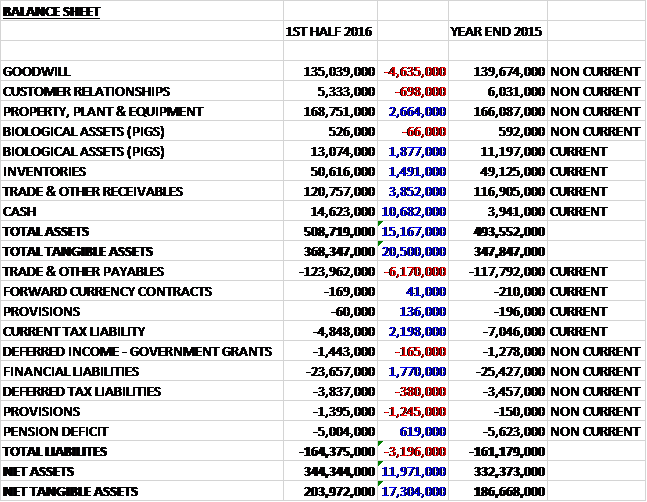

When compared to the end point of last year, total assets increased by £15.2M driven by a £10.7M growth in cash, a £3.9M increase in receivables, a £2.7M increase in property, plant and equipment, a £1.8M growth in the value of biological assets and a £1.5M increase in inventories, partially offset by a £4.6M decline in goodwill. Total liabilities also increased over the past six months as a £6.2M growth in payables and a £1.1M increase in provisions was partially offset by a £2.2M fall in current tax liabilities and a £1.8M decrease in financial liabilities.

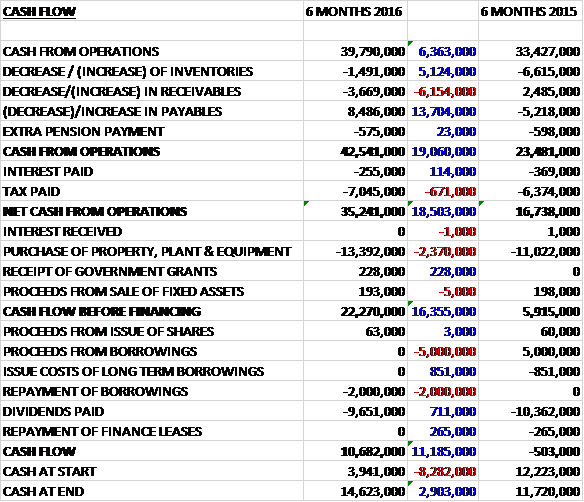

Before movements in working capital, cash profits increased by £6.4M to £39.8M. This was further boosted by a growth in payables and after a slightly lower interest payment and a higher tax spend the net cash from operations was £35.2M, a growth of £18.5M year on year. The group spent £13.4M on capital expenditure relating to the redevelopment of Kinston Foods cooked meats facility, the Benson Park projects and various other initiatives across the group to increase capacity and drive further efficiencies, and after that, the free cash flow was an impressive looking £22.3M. Of this, £2M was used to pay back loans and £9.7M was spent on dividend so that the cash flow for the six month period was £10.7M to give a cash level of £14.6M at the end of the half.

Overall the business performed strongly during the period and recorded revenue slightly ahead of the board’s original expectations. The improvement in group operating margin reflected the positive contribution from Benson Park, an improved performance from the Pastry business and a tight focus on cost control and operational efficiencies. The UK pig price fell 2% during the period and was on average 18% lower than in the same period last year. Despite this reduction, the UK price remains about 30% higher than in Europe. Improvements in productivity together with lower feed costs helped offset the impact of lower pig prices. Total export volumes grew by 18% during the period. Volume growth in Far Eastern markets of 31% offset lower volumes into the US and flat volumes into European markets. Further opportunities are being explored and the range of products being exported is continually being developed and broadened.

Fresh pork sales grew by 15% in the period driven by the recovery of business with one of the group’s principal retail customers as the market as a whole fell 10% due to the fall in UK pig prices. The recent AHDB pulled pork advertising campaign highlights the way in which focused marketing can deliver positive results with a 19% year on year increase in shoulder joint sales during the campaign. The next phase of the redevelopment of the Norfolk facility is now underway. This £6M investment to replace the existing abattoir will increase capacity, improve efficiencies and will facilitate the site’s push for USDA accreditation.

Sausage sales were 5% higher supported by strong volume growth. The premium sector of the market is the main driver of growth as consumers are prepared to pay a modest premium for better quality and taste. Sales of premium beef burgers were 24% higher year on year. Further substantial capital investment to upgrade mixing and filling equipment is planned at the Lazenby’s facility in Hull to support anticipated growth in the sausage category.

Bacon sales were 21% ahead as continued development of the business’ hand-cured, air-dried bacon was supported by strong premium gammon sales. This growth was aided by gaining sole supply status for premium bacon and gammon with one of the group’s lead retail customers shortly before the previous half year-end. With further new product launches planned for both existing and new customers in the run up to the peak Christmas trading period, the business is well placed moving into the second half of the year. The redevelopment and conversion of the former Kingston Foods site in Milton Keynes into a gammon facility was recently completed. This facility will apparently enable the business to target a new sector of the bacon and gammon market.

Cooked meat sales fell 6% reflecting overall market deflation and lower volumes to one retail customer. Further substantial capital investment at the Sutton Fields facility will upgrade staff amenities and refurbish both high and low risk production areas to enable expansion into new categories with existing customers and develop further capability to supply food to go ranges to manufacturing and food service customers. A significant three year capital investment programme at the Valley Park facility will refurbish the site and upgrade chilling and storage facilities to support future growth.

Sales of poultry from Benson Park made a positive contribution to overall group performance in the first half. New business wins during the period, both with existing and new customers, leave the business well placed moving into the second half of the year. The capital investment programme which was underway when the business was acquired in October last year, is now complete. The enlarged factory footprint and new in-line spiral cooking and cooling equipment was commissioned ahead of the peak Christmas trading period. This £9M investment programme has substantially increased capacity and will improve operational efficiencies as well as enabling the business to offer a broader product range.

Pastry sales were 45% ahead of the first half of last year, continuing the positive development since this category was introduced. Operational performance at the site continued the marked improvement seen in the second half of the last financial year and the category made a positive contribution to the overall group result. New product lines have recently been launched which, coupled with a strong Christmas and seasonal promotional programme, leaves the pastry business well placed to deliver growth during the remainder of the financial year.

Sales of continental products increased by 12% reflecting the UK consumer’s growing appetite for these products including charcuterie, cheeses, pasta and olives. Growth was supported by new product launches and new retail contracts together with a continued focus on sourcing new products from across Europe. The extension of the Guinness Circle facility to produce British cured meat products was completed during the period, and will produce a range of premium cured meats under both the Woodall’s brand and retail own labels.

Sandwich sales grew by 5%, supported by new contract wins brought on stream part way through the first half of last year. Top line growth was supported by an improved operational performance as the business continued to strip out underperforming accounts and rationalise the product range. The business has recently received confirmation that a key account will not be extended beyond its current term, however, and consequently the outlook for this business beyond the current financial year-end will be more challenging.

Following a change in the customer base of the sandwiches business, an impairment review was performed which resulted in a goodwill impairment of £4.6M. After this impairment the carrying value of goodwill in the business was £8.9M so any further adverse changes in key assumptions would lead to an additional impairment charge. Market conditions are expected to remain competitive through the second half of the year but the board believe they are well placed to deliver further growth.

After a 9.4% increase in the interim dividend, at the current share price the shares yield 1.9% which increases to 2.1% for the full year consensus forecast. At the period-end, the net debt position stands at £4.8M compared to £17.3M at the end of last year.

Overall then this has been a good period for the group. Profits increased, aided by the Benson Park acquisition; net assets improved and operating cash grew to give a very decent amount of free cash. Exports to the Far East seem to be increasing considerably but they did fall to the US. Most products performed well with fresh pork sales up due to a recovery of a large customer, sales of sausages were up due to increased sales of premium products and ales of bacon, gammon, pastries and continental fare all increased. Cooked meats performed less well with sales down generally as a result of market deflection but the real problem is that a key client has been lost in the sandwiches business which will affect the group next year.

It is difficult to quantify how much this loss will cost them but it was serious enough to take an impairment on the goodwill of the division. I suppose I will have to wait for some new broker forecasts to get a better idea. With an improving net debt position and a 2.1% dividend yield, the shares are not cheap but this is a quality outfit and once I manage to get some clarification on the lost sandwich contract, I might consider buying in here.

On the 28th January the group released a Q3 trading update where they stated that trading was in line with the board’s expectations. Total revenue was 5% ahead of the same period last year driven by strong volume growth of 11% and underpinned by a strong Christmas trading period. Underlying revenue was 4% higher with volumes up 10% as the benefit of falling input prices was passed on to the group’s customers. Export sales grew strongly with volumes shipped to the Far East 28% ahead of the same quarter last year.

Following the seasonal increase in working capital and ongoing capex, net debt increased from £5M to £18M in the quarter but remained well below the £57M reported at the same stage last year. Overall then, a steady update and I will continue to hold.

On the 5th April the group released a trading update for the year ended 2016. There was continued positive trading in Q4 which resulted in total full year sales volumes being 12% higher than the prior year. Full year underlying sales volumes increased by 10% with corresponding revenues ahead by 5% as the group’s customers continued to benefit from lower pork prices. Export sales grew strongly in the final quarter, reflecting the ongoing robust demand for pork products in Far Eastern markets.

The group invested well in excess of £30M across its asset base during the year to support future growth and drive operating efficiencies and this level of investment is expected to continue through the current financial year. Strong cash generation resulted in the group moving into a net cash position at the year-end compared to a net debt position of £18M at the end of Q3 and £17M at the end of last year.

Overall the board expect the trading performance for the year to be in line with their expectations.

On the 11th April the group announced the acquisition of Crown chicken from the Thacker family and management for a cash consideration of £40M paid from existing bank facilities. Crown is an integrated poultry producer based in East Anglia. They breed, rear and process fresh chicken for supply into a broad customer base across grocery retail, food service, wholesale and manufacturing channels. They also have an efficient milling operation which satisfies all of their own feed requirements as well as supplying feed to other pig and poultry producers in the region.

Last year, adjusted EBITDA for the business was £6.6M and the transaction is expected to be modestly earnings enhancing in the current year.