Dechra has now released their full year results for 2013.

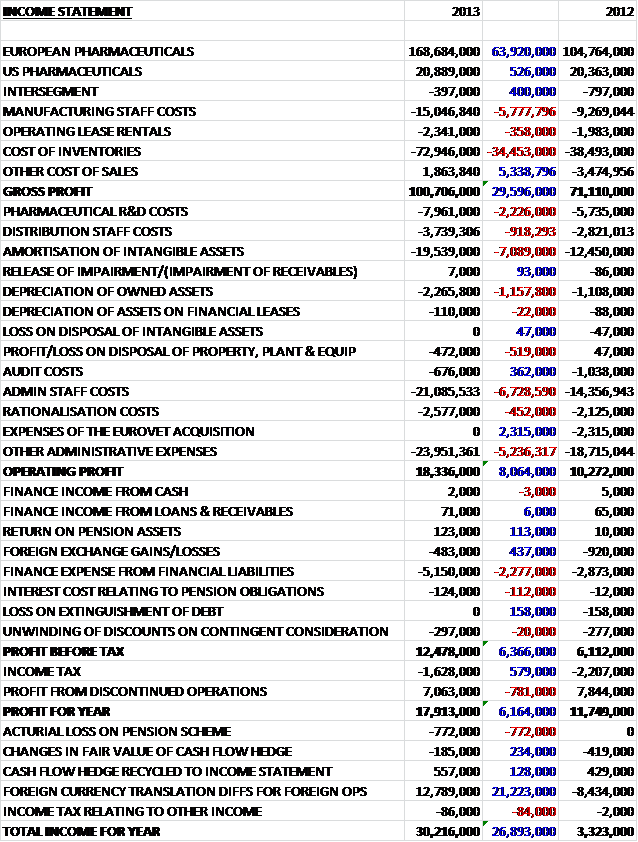

Following the decision to sell the services division, there are only two reporting segments with the vast of majority of revenues earned by the European sector, up by £64M as a result of the Eurovet acquisition. US revenues were fairly flat during the year. Cost of inventories were up by £34.5M, again at least partly due to the Eurovet acquisition. Admin costs seem to have increased by a fairly substantial amount and we can also see that there was £19.5M of intangible amortisations, up by £7.1M on last year. The £2.6M of rationalisation costs relates to the costs incurred to rationalise the four duplicated sales offices the group had after the Eurovet acquisition. This leaves the operating profit £8.1M higher at £18.3M. The only significant finance cost is the expense from financial liabilities, presumably interest from the huge loans, up by £2.3M to £5.2M. The profit from the discontinued services sector was £7.1M which left the profit for the year at £17.9M, £6.2M higher than in 2012 with the difference coincidently not that far off the £7.1M that will be lost with the sale of the services business.

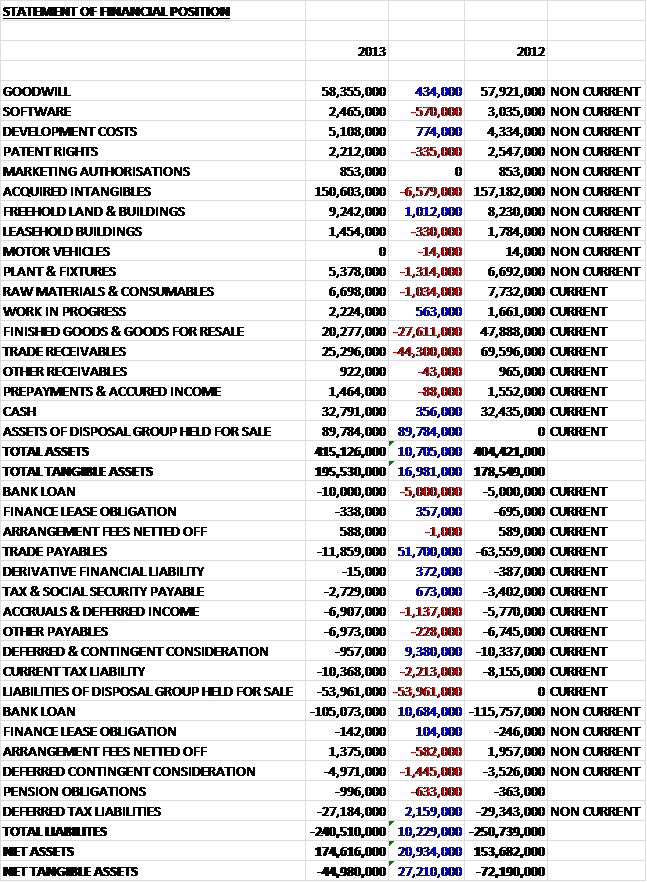

Overall Total Assets were up £10.7M on last year and we can see the effects of taking the services business out and placing it in assets held for sale. Acquired intangibles fell by £6.6M but remained very high. They are the development costs and product rights acquired with Dermapet, Gentrix and Eurovet. The big fallers, however, were finished goods inventory, down £27.6M and trade receivables, down £44.3M. The value of assets held for sale was £89.8M so without this effect, I suspect both inventories and trade receivables would be up. Taking off the intangibles gives tangible assets of £195.5M, up a healthy £17M on last year.

Liabilities fell by £10.2M during the year with £51.7M of trade payables being shunted into liabilities held for sale. The big changes were the £7.9M less of the deferred consideration left to pay and the £5.7M overall reduction in bank loans. I have to say that reducing loans and deferred consideration to such an extent whilst leaving the cash levels pretty much untouched is very impressive. Overall these movements give rise to a £27.2M increase to net tangible assets. A lot depends on what is received for the disposal but if these valuations are correct, much progress on the balance sheet seems to be made this year. Net Tangible assets are still negative to the tune of £45M but for pharmaceutical companies much of the value is in brands and patents so this is not of any great concern.

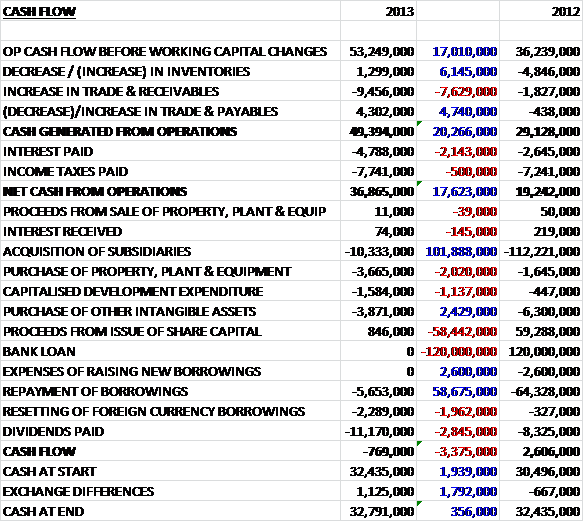

Operating cash flow before working capital changes was £53.2M, a £17M hike on last year. The main change in working capital was a £9.5M increase in receivables which meant that cash generated from operations was £49.4M, £20.3M better than last year. Interest nearly doubled to £4.8M due to the big loan taken out to acquire Eurovet and net cash from operations was £17.6M higher at £36.9M. Out of this cash, £10.3M was spent on acquisitions relating to the deferred consideration on Eurovet . There was £5.2M spent on capital expenditure and a further £3.9M spent on intangible assets. Also during the year, the group paid back £5.7M of borrowings and spent £11.2M on dividend payments. There were no new loans and the resultant cash out flow was £769K and with a healthy cushion of £32.8M of cash at the end of the year, this is really rather impressive. It will be interesting to see if it can be sustained without the cash receipts from the Services business.

As far as profit is concerned, European pharmaceuticals contributed £45.8M whereas US pharmaceutical profit fell slightly to £5.6M. Geographically, the UK still accounts for the largest amount of revenue followed by Germany and then the US.

During the year, the group completed a licencing, supply and distribution agreement for a branded veterinary generic product from a US pharmaceutical company. Dechra will pay $3M up front and then a potential further $2M based on achieved sales of $20M, these are new companion animal products and will not make a material impact. The idea is that they will complement the existing products and add to the growth of the business in the States. The major event last year, as mentioned in the last update was the Eurovet acquisition for a cash total of £116M which included £36.3M of goodwill and £78.7M of other intangibles. Also during the period, a further £10M was paid with respect to contingent consideration relating to the Dermapet acquisition. There is now only $6M contingent consideration left. It was agreed that the Services division would be sold for £87.5M to Patterson Companies Inc, which relates to a profit of £400K. The completion accounts are yet to be finalised, however.

Good work has been made on overdue receivables, presumably at least partly due to the services business being sold. There is now £4.5M overdue as opposed to £10.1M last year, none of which are overdue by more than three months. At the moment, due to the high level of debt the group is quite susceptible to interest rate increases and a 2% rise would reduce group profit by £621K. Even more concerning is the exposure to the Euro exchange rate. A 10% appreciation of Sterling against the Euro would cost the group £3.2M.

Overall, pharmaceutical sales grew by 4.7% with companion animal products up 7.8% driven by increases in sales of Vetoryl, Felimazole and Caridsure whereas food producing animal sales dropped by 3.2% due to pressure on antibiotic prescriptions and competition on Cyclospray. Diets showed growth of 2.6% and third party manufacturing increased by 12.5%.

Dechra Europe is performing well in the three major European markets and EU revenues were up 5% on a like for like basis. The UK was the fastest growing market with Germany and France also showing solid growth as Eurovet’s swine and poultry products were launched in France for the first time and all Eurovet products are now ready to be launched into Scandinavia. The export business is also expanding in markets around the world and the Dechra brand will be expanded through newly established subsidiaries in the EU. Performance in Netherlands and Scandinavia was relatively disappointing, however. Sales of pet diets increased by 2.6% at constant currency levels, which was boosted by the launch of a new intensive support diet for animals in post-surgery rehabilitation. Third party manufacturing continued to perform strongly with an increase in external sales of 12.5% at a constant currency basis and the group continued to receive a high level of new external contract enquiries.

The US business currently only markets companion animal and equine products and spending in the US pet market has been recovering from the levels seen during the financial crisis. Revenue from the segment grew by 4.7% in the year, hampered by third party supply issues with the ophthalmic and dermatological ranges to such an extent that the dermatological product, Animax, had a complete out of stock situation. Dechra has now changed suppliers but the validation from the relevant authorities for the new supplier is taking some time. It is considered that the group should be able to make up most of the lost sales when it is up and running though. The underlying performance of the key products in the US has actually been strong with Felimazole growing by 16% and Vetoryl growing by 12%. There are currently several products in the US development pipeline which should encourage further organic growth.

Following the Eurovet acquisition, Dechra had manufacturing sites in Skipton, UK; Bladel in the Netherlands and Uldum in Denmark. The small site in Denmark will be closed by the end of next year with its two key products being transferred to Skipton. The Bladel site predominantly manufactures products for food producing animals in large scale batches. The acquisition has had the effect of allowing Dechra to expand into Germany and into food animals, two markets where they were not really that well developed and expanding into food animal drugs is particularly interesting because this is a much bigger market than companion animals in emerging markets outside the EU and North America

The process to get drugs to market in the veterinary world takes between three to five years so products are in development for a much shorter time that in the human pharmaceutical arena. There are currently 11 drugs in development for dogs, cats, horses, cattle and poultry and revenues from these projects are expected to peak at around £35M. New products for the global markets includes Methoxasol, an antimicrobial for swine and poultry that has been approved for use in the EU; Buprenodale, a multi dose small animal analgesic that has received authorisation for use in the EU and Anesketing, a generic companion animal sedative that has been approved for use in seven EU countries. There were also a number of line extensions, including Soludox, a water soluble antibiotic for swine and poultry that has a new indication for use in Turkeys in the EU; Felimazole 1.25mg, a new dose strength that has been approved for use in the EU and Comfortan, a companion animal analgesic has received approval for an extension for its use in cats. In addition, a number of drugs were registered in new territories, including Libromide used to treat canine epilepsy has been extended for use in France, Austria, Portugal and Switzerland; Felimazole, for feline hyperthyroidism has been approved for use in Australia and Vetoryl, used in the treatment of canine Cushing’s syndrome has been approved for use in South Korea, Brazil and New Zealand. The new dosing for Felimazole is intended to further differentiate the product from a number of generic drugs that have been recently launched in a number of EU countries.

The new product launch of Osphos to treat lameness in horses was delayed due to problems with a third party manufacturer. This product is due to be submitted in UK, Canada and Australia imminently but as the horse is classed as a food producing species in the EU, further work is needed on it before submission into that territory. It is already approved for use in the US. A second major new product, for use in a canine endocrine disorder was originally intended to be manufactured by a third party but following the problems it is now likely to be produced in house. The clinical trials for this product are progressing well.

During the year the long standing Chief Financial Officer, Simon Evans, resigned. It always worries me when this happens as it sometimes points to hidden problems in the business, particularly as he was still relatively young at 49 and had been with the company for 15 years. His replacement is Anne-Francoise Nesmes who joins the group this year and has herself been at Glaxosmithkline for 15 years where in the latter years she worked as Senior VP of Finance in the global vaccines business. During the year, there was also another executive director appointed and Tony Griffin joined from the acquired Eurovet and became managing director of the EU pharmaceutical business.

This was a fairly good year for Dechra, profits were up £6.2M but discontinued operations contributed £7.1M. Revenues in the EU were particularly strong, partly due to the Eurovet acquisition. Net tangible assets were up considerably with borrowings and contingent consideration both down. Cash flow was flat but it should be taken into consideration that this included spending of £5.7M to pay back loans, £10.3M on deferred consideration, £3.9M on the acquisition of intangibles (the licencing agreement) and £11.2M spent on dividends. That flat cash flow now looks rather impressive. Current trading is being described as ahead of last year and in line with management expectations. Net borrowings currently stand at £80.8M, still substantial but some good progress has been made in bringing it down as mentioned previously. At current share price levels the dividend is a solid but unexciting 1.9% and the P/E stands at 18.6 but with the loss of the services profit next year, this is predicted to increase to 20.8 which is probably about right.

On 17th October, Dechra released a trading update covering Q1 2014. It was stated that trading with inline with expectations, approximately 5% ahead of last year but 1% behind on a constant currency basis. The sale of the services segment was completed for £87.5M with £81.1M of that being used to play down debt. European pharmaceuticals increased revenues by 6% but this was entirely due to exchange rate differences and at a constant currency revenues were down 1% as robust trade in Dechra’s own sales and marketing organisations was more than offset by reduced exports, apparently due to the phasing of orders. US revenue was down by 5% (down 7% at constant currency) doe to the Animax supply issues. Were it not for that, US revenues would have been ahead. I must admit I was a little disappointed by this update and I do hope these supply issues in the US get sorted shortly. As long as the reduction in exports really is due to the phasing of orders, though, there is not really that much to worry about here.