Dewhurst has now released their interim results for the year ending 2018.

Revenue declined by £1.4M and operating costs fell by £797K which meant that the operating profit was £604K lower. There was a £439K profit on a business sale and finance costs declined by £52K but tax charges grew by £121K to give a profit for the period of £1.8M, a decline of £290K year on year.

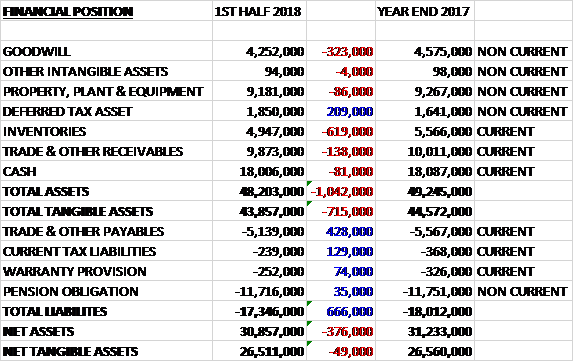

When compared to the end point of last year, total assets declined by £1M, driven by a £619K fall in inventories, a £323K decrease in goodwill and a £138K decline in receivables, partially offset by a £209K growth in deferred tax assets. Total liabilities also declined during the period due to a £428K decrease in payables and a £129K fall in current tax liabilities. The end result was a net tangible asset level of £26.5M, broadly flat over the past six months.

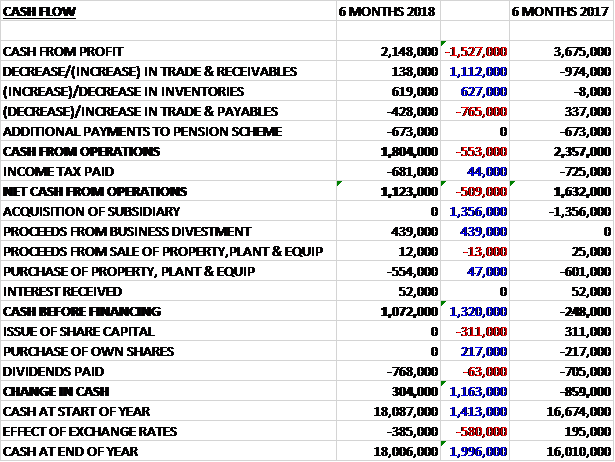

Before movements in working capital, cash profits declined by £1.5M to £2.1M. There was a cash outflow from working capital and the pension scheme payments but the working capital movements were more favourable than last year and after tax payments reduced by £44K the net cash from operations was £1.1M, a decline of £509K year on year. The group brought in £439K from a business divestment and spent a net £542K on capex to give a free cash flow of £1.1M. Of this, £768K was spent on dividends to give a cash flow of £304K and a cash level of £18M at the period-end.

Although sales and profit fell during the period, on a constant currency basis and adjusting for the divested business, underlying sales were slightly up. Demand for keypads was weak, which was the most significant contributor to sluggish sales and the strengthening sterling reduced profits by £200K. Canada continued its strong growth, the UK business was varied but overall up, and Australia was also mixed.

In most of the group’s markets, the business climate seems to be reasonably positive at present. The exception remains the UK where there is still some uncertainty about the short term and the economic situation is highly dependent on political decisions. Although keypad sales have picked up a little in the last couple of months, the board do expect a declining trend in the long term. Current exchange rate levels continue to be a drag on the group. The second half of the year may see a period of consolation but on balance the board are encouraged by the future growth prospects for the group.

At the current share price the shares are trading on a PE ratio of 21.4 which falls to 19.4 on the full year consensus forecast. After the interim dividend was maintained the same the shares are yielding 1.1% which is forecast to remain the same for the full year.

On the 4th June the group announced the acquisition of A&A Electrical Distributors for an initial consideration of £10.5M plus a deferred consideration based on profits generated over the next two years, with the expected consideration expected to be around £1.5M. It is expected that the acquisition will be immediately earnings enhancing.

The business is based in London and is a lift and electrical distribution company which works with lift companies operating in the UK and have been a long standing customer of Dewhurst. Last year the business made a profit of £3.3M but the acquired net assets are only around £800K, giving a goodwill generation of about £11.2M.

Overall then this has been a difficult period for the group. Profits fell, net tangible assets were broadly flat and the operating cash flow declined, although some free cash was generated.

The keypad demand has been weak and this is something it seems that the board expect to continue. These shares are not cheap with a forward PE of 19.4 and yield of 1.1% so this does not look very tempting at the moment.