Easy Jet is a short haul European low cost airline. As well as the main brand, they also own 49% of EasyJet Switzerland. The company pays some £12.6M in order to use the Easy Jet brand. It has now released its final results for the year ending 2014.

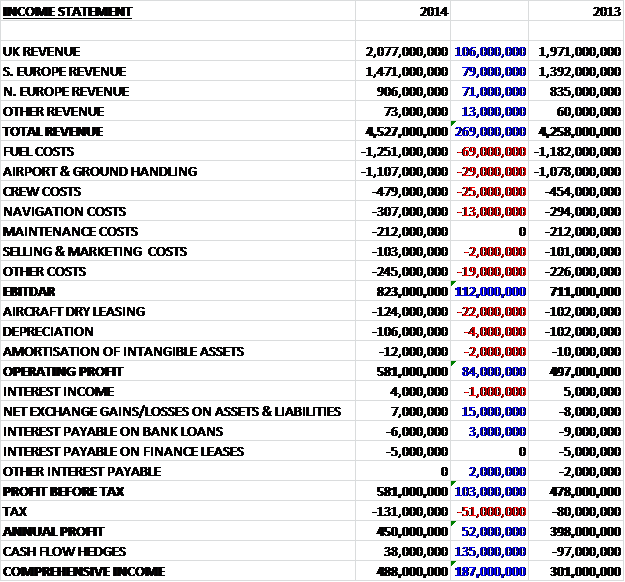

Revenues increased across all markets with a £106M increase in the UK, a £79M growth in Southern Europe and a £71M increase in Northern Europe. Various costs also increased, with fuel costs up £69M due to higher load factors on the planes, airport and ground handling increasing by £29M due to annualised costs in Italy, crew costs up £25M due to a 2% increase in payroll costs and an increase in average sector length, and marketing costs up £13M. Maintenance costs managed to remain flat during the year as the group benefited from a renegotiated engine maintenance contract (most of the gains are non-recurring though) but there was a £19M increase in other costs, driven by the cost of wet leasing two aircraft over the summer, employee bonuses and digital development costs to give an EBITDAR of £823M, an increase of £112M year on year. Due to an increase in aircraft dry leasing due to 17 new aircraft leases that were taken out in 2013, and tax, partially offset by a £15M favourable swing in exchange gains, the profit for the year ended at £450M, an increase of £52M.

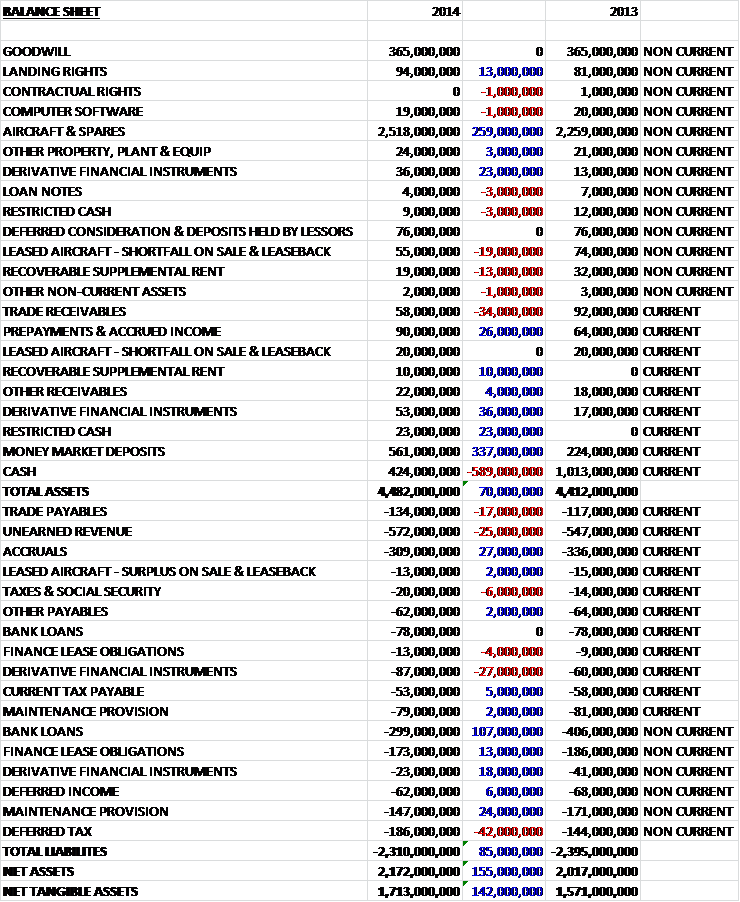

When compared to the end point of last year, total assets increased by £4.482BN driven by a £259M increase in aircraft and spares, a £337M growth in money market deposits and a £59M increase in derivative financial instruments, partially offset by a £589M fall in cash levels, and a £34M decline in trade receivables. Liabilities fell during the year as a £42M increase in deferred tax and a £25M growth in unearned revenue, which represents the seats sold but not yet flown, was more than offset by a £107M fall in bank loans, a £27M decline in accruals and a £26M fall in the maintenance provisions. The end result was a decent £142M increase in net tangible assets to £1.713BN which seems like a strong balance sheet to me. There were some £466M of operating leases outstanding, mostly relating to aircraft.

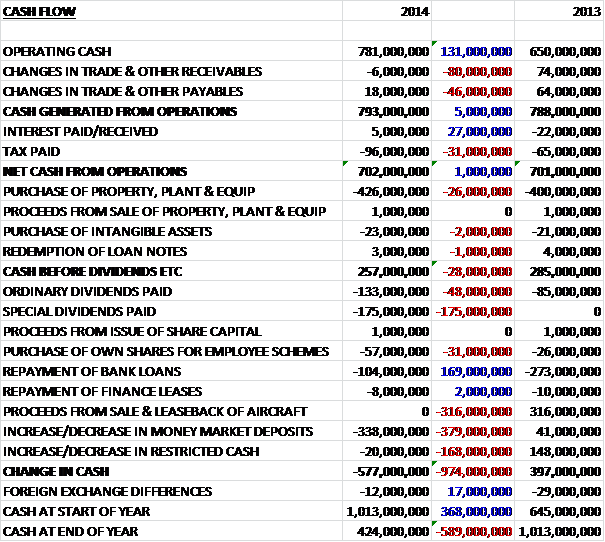

Before movements in working capital, cash profits increased by £131M to £781M. The favourable movements last year in payables and receivables were then partially offset and a reduction in interest paid was counteracted by an increase in tax so that net cash from operations increased by just £1M to £702M. This covered the capital expenditure of nine new aircraft, parts used in engine restoration and pre-delivery costs on 35 aircraft ordered during the year along with £20M for the acquisition of Gatwick landing rights from FlyBe, fairly comfortably to give a free cash flow of £257M. The group used this to pay off some loans and bank leases with the rest going on ordinary dividends before they dipped into their reserves to pay a £175M special dividend and put some £338M into money market deposits to leave a cash outflow of £577M and a cash level at the year-end of £424M.

The improvement in profit is due to a number of factors such as the continued revenue per seat growth and higher capacity; a 1.3 percentage point improvement in the load factor; and the better than expected cost performance driven by the “Easy Jet lean programme”, one-off benefits of the CFM engine selection and the continued scale advantages of increasing the proportion of A320 aircraft in the fleet which have been introduced over the last few years with minimal reduction in yields and cost savings per seat of around 7% to 8% when compared to the smaller A319 aircraft through economies of scale.

The revenue per seat grew by 1.2% to £63.31 (1.9% on a constant currency basis) which was driven by a number of factors including the continued improvement in the mix of routes due to the ability to respond quickly to changes in demand, improved conversion and yield from more sophisticated pricing for customers through further developments in the bespoke revenue management systems, performance of allocated seating and the yield management of bag charges, the increase in load factor, and initiatives to target the business passenger. Revenue per seat fell at Gatwick due to the purchase of FlyBe slots and the management see a good opportunity to improve revenue performance at the airport as these slots are integrated.

As touched upon above, the group has made a concerted effort to target business customers during the year and the managed business, where the group has a contractual relationship with certain corporates, grew by 10% year on year. The group’s sales through dedicated business channels such as Global Distribution Systems, API and on-line booking tools grew by 34%. In September 2014, a TV ad campaign was launched focusing on the business passenger offering which enabled the group to carry its highest number of business passengers in a month ever. Furthermore, the group partnered with Sabre to enhance its booking process and renewed its distribution agreement with Travelport. It also renewed its travel deal with the UK Houses of Parliament and won best short haul airline at the 2014 Business Travel awards.

Easy Jet is the largest short-haul carrier in the UK with a market share of around 20%. They saw growth across a number of airports in the country with the majority of the increase coming at Gatwick due to the acquisition of FlyBe slots last year, where capacity increased by 15%. The slots were transferred at the end of March 2014 and have been used to further build the number of routes out of the airport and increase frequencies on existing routes such as Inverness and Amsterdam. Overall, the group increased capacity in the UK by 5.8% and launched 24 new routes during the year.

In Switzerland the group grew capacity by 6.8%, carried over 10 million passengers and now has 23 aircraft bases in the country. 11 new destinations were launched from Geneva and Basel during the year which means that they now fly 110 routes from the country. Also during the year, Easy Jet consolidated its number one position at the two airports, increasing market share by 0.4% and 1.2% to 40.5% and 52.4% respectively.

Easy Jet is now the largest low-cost airline in France with a market share of around 14% with 26 aircraft based in the country. During the year some 14.7 million passengers were carried over 180 routes with 24 launched in 2014. The group was able to take advantage of the Air France pilot’s strike during the year by adding additional capacity, attracting more customers and increasing revenue by £5M. The group launched four new routes at Bordeaux, increased frequencies on key business routes, became the largest short-haul carrier in Nice and launched two new French destinations at Strasbourg and Figari.

Easy Jet has 27 aircraft based in Italy, grew capacity by 6.2% during the year and has number one or two positions at Milan Malpensa, Rome Fiumicino and Naples, where the base was only opened in March 2014 with two aircraft. They also have a strong position in Venice, Olbia and Pisa. It is believed that further opportunities exist in the country given the current market dynamics and the position the group have already established in the market.

In Germany, Easy Jet’s capacity grew by 6.7% and 11 aircraft are now based at the country in Berlin and Hamburg, where the base was launched in March with two aircraft. The focus so far has been on Berlin where the company has nine aircraft and a 62% market share at Schonefeld airport and it has taken market share from Lufthansa in the city.

Easy Jet carried about four million passengers in Spain and Portugal during the year and with a market share of around 13% is the second largest carrier in Lisbon with four aircraft based at the airport. In Spring 2015 the group is planning on opening its second Portuguese base at Porto with two aircraft. Spain is also an important destination in the network and the group have an 8% market share in the Spanish short haul market. In Netherlands, the group is the second largest carrier in Amsterdam with a market share of around 9%. In Spring 2015 the group will open a base at Schiphol airport with three aircraft.

Clearly one major driver of customers to the Easy Jet proposition is the value offering. The strong operational and cost performance is built around ensuring aircraft depart and arrive on time. The first half of the year saw some challenges for the group’s operations including the Italian Air Traffic Controllers strike in October, a power outage at Gatwick on Christmas Eve, Air Traffic Control computer systems failure in the UK, the adverse weather conditions in December across Northern Europe and the French Air Traffic Controllers strike in March. The second half of the year also saw some operational issues including recurring industrial action in Italy and France, unusually prolonged continental summer thunderstorm periods and the transitional impact of the group’s large increase in capacity at Gatwick following the acquisition of FlyBe slots. All of these issues resulted in a two percentage point reduction in on-time performance levels for the year as a whole to 85%.

During the year, the lean programme delivered £32M of sustainable savings, of which £18M was delivered in the second half. Savings were focused on ground handling contracts and agreements with non-regulated airports. Further savings were delivered by engineering initiatives and fuel burn projects including the benefit of more aircraft fitted with Sharklets (which improve fuel efficiency) in the fleet. The process also highlighted that there are many more cost saving opportunities for the group to deliver which will form the basis of a plan to deliver £30M to £40M in sustainable savings per annum over the next five years.

After several years of low market capacity growth, the European short-haul market has returned to more normal levels of capacity growth. In the year to September the total number of short-haul seats increased by 3% on the group’s markets with EasyJet experiencing seat growth above the market at 5.1% during 2014 as a whole. It is expected that capacity and demand will be broadly aligned over the next five years.

During the year the group has exercised its remaining 35 options and purchase rights over current generation Airbus A320 aircraft for delivery between 2015 and 2018. The group is contractually committed to the acquisition of 170 Airbus A320 family aircraft with a total list price of $14.6BN with 20 being delivered in 2015, 50 between 2016 and 2018 and the remaining 100 between 2017 and 2022. They now have number one or two market positions at primary airports including Gatwick, Geneva, Paris Orly, Paris CdG, Amsterdam and Milan Malpensa.

During the year the group has seen regulatory progress at Gatwick where they have reached a long-term agreement that provides a good base for savings and growth over the next seven years. In addition, governments have apparently started to reconsider how airports are regulated in France and Switzerland. There have been significant increases in charges at Rome Fiumicino airport, however, where the airport has structured charges in a way that discriminates against point-to-point airlines (I suppose to try and protect Alitalia’s position) and this has been accompanied by continued pressure on regulated charges at a range of other airports across Europe.

The group is susceptible to changes in the price of fuel and currency movements so they hedge between 65% and 85% of the next year’s fuel requirements and between 45% and 65% of the following year’s anticipated foreign currency requirements. A £10 per tonne movement in the cost of fuel impacts the fuel bill by $3.5M, a one cent movement in £/$ impacts profits before tax by £1.3M and a one cent movement in £/€ impacts profit before tax by £1.1M.

There were a number of board changes with Dr. Andreas Bierwirth and Francois Rubichon joining the board. Andreas is currently CEO T Mobile Austria and has previously served on the board of Austrian Airlines whereas Francois used to be deputy CEO and COO at Aeroports de Paris so their experience should prove useful going forward. Just after the year end David Bennett and Professor Rigas Doganis will retire from the board having both served for nine years. It has to be said that in my view the executive directors are very well paid, perhaps excessively so. Including the LTIP scheme, the CEO earned £7.7M last year which is an incredibly generous, perhaps greedy, amount.

It is interesting to note that some 45% of the total shareholding voted against the remuneration policy. Clearly one factor for this is the huge salaries being earned by the executive team but there is a little more to the story than this. That 45% corresponds to just two major shareholders, none of them institutional, and a look at the shareholder register suggests that the shareholders voting against the policy are Sir Stelios Haji-Ioannou and his family, who are the founders of the group.

Clearly there are a number of potentially significant risks that affect Easy Jet, being in the airline business. There is always the low risk of a major accident or terrorist threat which may damage the reputation of the airline. More likely and less serous is the impact of mass disruption including prolonged adverse weather, volcanic dust clouds, strike action and pandemics which would affect the ability for people to fly. Additionally, although the fact the group operates one type of plane has its advantages with regards to costs, it does potentially leave the group susceptible to the failure of their one supplier, Airbus, or the A320 aircraft, although this does seem unlikely at the moment. Additionally, although the position is fairly well hedged, sudden significant increases in the fuel price or a weakening in the exchange rate against the US dollar would have a significant effect on fuel costs and a change in the general macroeconomic environment could reduce the number of people travelling, although as a low-cost provider this would probably affect Easy Jet less than the legacy carriers.

Going forward, the group expects to grow capacity by around 3.5% in the first half of 2015 and by around 5% for the full year. Forward bookings for the first half are slightly ahead of the prior year with the investment in the new slots at Gatwick growing capacity at that airport by 10%. As a result of the continued investments, revenue per seat is expected to be broadly flat in the first half of the year and costs per seat are likely to increase by 2.5% in the first half and 2% for the year as a whole, driven by increased crew costs ahead of new base openings, charges at regulated airports in Italy and Germany, increased navigation charges and increased maintenance costs due to the ageing of the fleet. It is estimated that the fuel bill for the half year is likely to fall by between £12M and £22M and on a full year basis, the fall is expected to be between £22M and £70M. In addition, exchange rate movements are likely to have a £5M favourable impact in the first half and £20M for the full year.

The board will continue to keep the balance sheet under review and intends to make further returns of capital to shareholders as further funds accumulate – I like the sound of that. As for the regular dividend, the board has decided to increase the pay-out ratio from one third of profit after tax to 40% of profit after tax. This year this represents a dividend of 45.4p, an increase of 36% over last year’s ordinary dividend with next year forecasted to yield 3.2%. Including operating leases at seven times, net debt stood at £446M at the year-end compared to £156M this time last year (actual net cash was £422M). This represents a gearing of 17% compared to the target of between 15% and 30%. It seems as though the group is looking to reduce these leases going forward, which is a good strategy in my view as they are targeting 20% leased aircraft compared to the current level of 32% leased aircraft. At the current share price, the shares trade on a P/E ratio of 14 which reduces to a good value 11.4 on next year’s consensus forecast.

Overall then, this seems to have been a good year for Easy jet. Profits are up, as are net assets and underlying operational cash flow, although the actual net cash from operations was broadly flat due to favourable working capital movements last year. In any event, the group throws enough plenty of free cash and the balance sheet looks good. During the year, capacity increased as did revenue per seat with allocated seating and the targeting of business travellers aiding progress. The newly acquired slots in Gatwick have not been fully integrated and next year should benefit from the full year of their contribution. New bases are to be opened up in Porto and Amsterdam which should further increase capacity next year aided by a general improvement in the European aviation market.

The on-time performance suffered from a plethora of one-off items, with strike action being a particular issue throughout the year but this is just one of the many risks that affect companies in this industry. Next year, the profit per seat is not likely to be that far ahead of this year as flat revenues coincide with increases in crew costs, regulation charges at certain airports and maintenance costs, offset by a reduction in fuel costs. The forward P/E of 11.4 looks decent value though and the 3.2% dividend yield is nice to have so I think in conclusion these shares offer decent value at the moment.